Nitin Agrawal

Moneycontrol Research

Motherson Sumi Systems (MSSL), one of India’s largest auto components firm, reported a decent set of Q1 FY19 earnings. The company continues to have umpteen growth triggers going forward. Strong demand in domestic and export markets, robust order book, expansion at various locations globally, shift towards electric vehicles (EV) and new emission norms (Bharat Stage VI) should boost topline as well as operating margin. At the current price, MSSL is reasonably valued and could be a strong portfolio fit for the long term investor.

Quarter in a nutshell

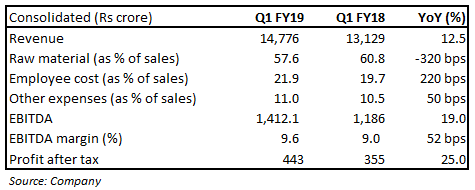

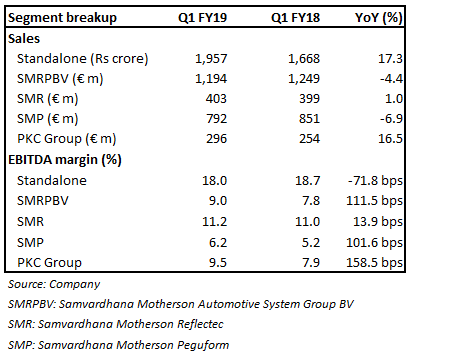

The company recorded a 12.5 percent year-on-year (YoY) growth in consolidated operating revenue, led by strong performances of the standalone entity as well as PKC Group. Standalone business revenue, adjusted for the impact of IndAS, grew 21 percent on the back of strong growth accruing from domestic (21 percent) and export (25.7 percent) markets.

Finnish subsidiary PKC Group, which is a wiring harness specialist, posted 16.5 percent growth in revenue. This was on the back of strong growth emanating from US commercial vehicle (CV) sales and contribution from commissioning of its third joint venture in China.

Samvardhana Motherson Peguform (SMP), a leading global supplier of door, instrument panels and bumpers, reported a 6.9 percent decline in revenue (adjusted revenue grew 12.4 percent YoY). Samvardhana Motherson Reflectec (SMR), a global supplier of exterior mirrors, reported flat numbers due to weak order flows from Hyundai and Kia Motors.

On the profitability front, adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) margin contracted 30 bps on the back of 20 bps contraction in SMP’s EBITDA margin due to high start-up cost. PKC Group surprised with a 140 bps expansion in adjusted EBITDA margin.

MSSL has multiple growth levers ahead:

Robust order book

The company reported the highest ever order book of 17.2 billion euro at Samvardhana Motherson Automotive System Group (SMRPBV) in FY18, which provides strong revenue visibility going forward.

Huge expansion on track

At present, the company has six plants at different stages of completion globally. The management said start-up cost would be lower as SMP’s Kecskemet plant in Hungry has turned operational. They also mentioned that the Tuscaloosa plant in the US has also begun operations. These plants are expected to add 1 billion euro in revenue on a full ramp-up in FY19.

Once the new plants start operations and ramps up fully, operating leverage will kick-in, thereby contributing to margin expansion. The company said it would spend around Rs 2,000 crore capex in FY19.

Strong volume growth

The management said topline growth for the India operations was due to strong growth in domestic passenger vehicles. Growth was also fuelled by an increase in content per vehicle.

With regulatory challenges in Indian automobile industry easing, MSSL was able to register strong growth, indicating strong position of the company in the Indian market. With teething problems related to Goods & Service Tax behind, it is in a vantage position to gain from increased vehicle demand. New upcoming BS VI emission norm would lead to complex wiring harness requirement that would benefit the company as the value is expected to go up.

The management believes that demand growth remains strong across businesses and key markets, especially for commercial vehicles in the US.

PKC – Shining now

Integration of PKC is happening smoothly as is evident from the strong growth during Q1. The firm benefitted from strong demand in North American and European truck markets. The management expects to achieve 35-40 percent of return on capital employed (RoCE) by FY20.

Reydel: Another growth driver

The company had acquired Reydel Automotive Group a few months back and consolidation of its financials would start from Q2 FY19, which would aid performance. Reydel had a revenue and EBITDA of $1.05 billion and $67 million in CY17, respectively.

EVs: An important catalyst

The Centre’s thrust on EVs will be an important catalyst for the next leg of growth for MSSL’s India operations. The management said EVs would need more wiring components, which would increase the content per vehicle by close to 10-20 percent. Other businesses related to polymer and mirror-based products would not be affected because of the shift to EVs.

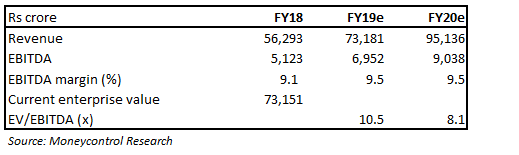

ValuationsMSSL is currently trading at 10.5 and 8.1 times FY19 and FY20 projected EV/EBITDA multiples, which is reasonable. On the back of multiple growth levers and reasonable valuations, we advise investors to be a part of this long-term journey.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.