Krishna Karwa

Moneycontrol Research

Highlights:-

- Contribution of branded products to revenue is increasing

- Capex intensity is likely to moderate from H2 FY20

- Utilisation rates and product mix will determine margins

- Overdependence on US markets remains a key risk

- The stock trades at reasonable valuations

--------------------------------------------------

Himatsingka Seide (HSL), one of India’s largest home textile majors and exporters, draws our attention on account of improving business fundamentals. Conclusion of capex cycle by H1 FY20, higher contribution from branded products, an uptick in utilisation rates and undemanding valuations make us bullish on the stock.

Q3 review

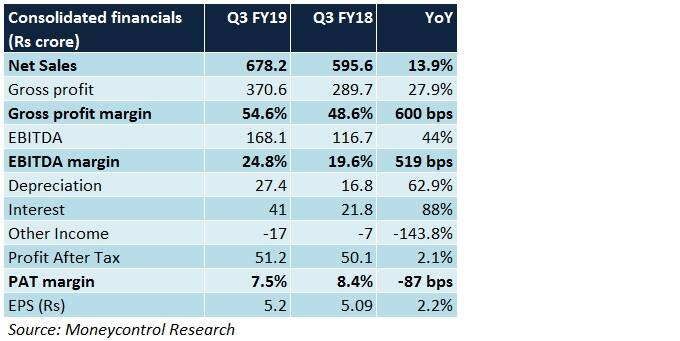

Positives- Sales grew on the back of higher contribution from branded products (84 percent of Q3 sales)

- Gross and operating margins expanded noticeably because of a good product mix and full benefits of captive consumption (ie. yarn being utilised to manufacture bed sheets)

Negatives

- Forex losses resulted in other income declining sharply year-on-year (YoY)

- Depreciation and interest costs rose significantly YoY due to investments in the terry towel plant

- Tax rate increased marginally YoY

- The above factors led to a marginal reduction in PAT (profit after tax) margins

Why consider investing?

Capex intensity is waning

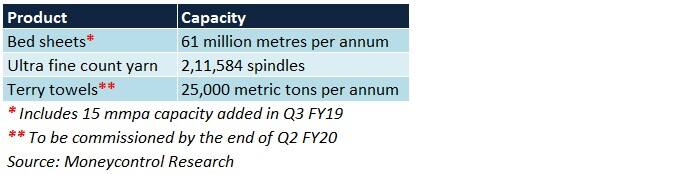

By September 2019, HSL’s terry towel facility is likely to be set up. Post this, barring regular maintenance capital expenditure, there is no big expansion plan.

Depreciation and financing charges, that rose noticeably in the past 4 quarters due to investments in the terry towel project, are likely to reduce from H2 FY20 onwards. This is because impetus will be laid on debt repayment. Consequently, bottom-line margins, working capital cycle and cash flows should improve.

Utilisation rates are likely to go up

In Q3 FY17, HSL expanded its bed sheet manufacturing capacity from 23 mmpa (million metres per annum) to 46 mmpa. Utilisation levels in respect of both (ie. original and new capacity) are stable at the moment. As the company’s order book (particularly for branded products) grows, there will be a corresponding uptick in manufacturing activities. This, in turn, should help achieve operating leverage.

Debottlenecking of bed sheet manufacturing capacity has been concluded in Q3 FY19, thereby resulting in an increase in capacity to the tune of 15 mmpa. This new capacity will be utilised for manufacturing products that yield lower realisations, implying that sales growth, to this extent, will be volume-driven.

Once the terry towel facility becomes operational, utilisation levels should start moving up too.

Sale of branded products on an uptrend

In 9M FY19, brands constituted about 85.6 percent of the top-line as against 71 percent in FY18. HSL’s own brands are making their presence felt in the financials.

HSL will complete integration of manufacturing processes of the Tommy Hilfiger brand by Q4 FY19-end.

Rights to sell ‘Calvin Klein Home’ products globally have been acquired. Previously, HSL could sell products only in North America.

Since branded products, especially own brands and fashion bedding variants, command better realisations vis-a-vis their unbranded counterparts, HSL’s margins should start moving up gradually.

Risks

To mitigate risks associated with regional concentration, HSL is exploring markets in Europe and Asia. Nevertheless, at the moment, the US market alone comprises nearly 85-90 percent of HSL’s annual top-line. Therefore, Trump’s actions of withdrawing the preferential trade treatment granted to Indian exporters may affect the company’s future revenue visibility.

Indian Rupee’s appreciation vis-à-vis the US dollar would impact product realisations to the extent of unhedged cash flows. Raw material (cotton) costs are not showing any signs of moderation as of now.

Competitive pressure from nations such as Pakistan, Vietnam and Bangladesh continues to persist.

Signs of consumption slowdown in international markets can hit the order book.

Outlook

HSL’s stock price has been on a downward spiral during the course of the last 12 months. This is primarily on account of market volatility and YoY dip in PAT (profit after tax) margins since the last 3 quarters.

After a sharp 47 percent correction from its 52-week high, the stock trades at an undemanding 6.7 times its FY21 projected earnings. This makes it a good value buy.

However, it is pertinent to note that any meaningful re-rating in HSL’s valuation multiples may be seen only from H2 FY20.

For more research articles, visit our Moneycontrol Research page

(Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!