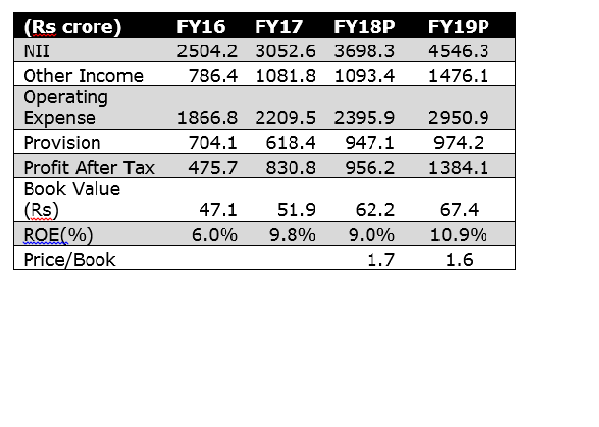

Madhuchanda DeyMoneycontrol Research

On the face of it, Federal Bank’s December quarter numbers are broadly in line with what the street was expecting. But they mask the deterioration in slippages and the additional provision to be taken in the coming quarters towards the assets sold to asset reconstruction companies (as per the changed guideline of the RBI). We have tweaked estimates to factor in the additional provision. The knee jerk reaction in the stock post results and the near-term weakness is an opportunity to accumulate as the bank seems to be doing a decent job on most other parameters.

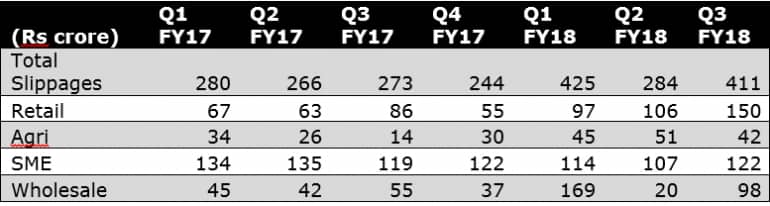

Rise in slippage

Gross slippages for the quarter rose to Rs 411 crore, spread across both corporate and retail loans. Corporate slippages were driven by three accounts, the management said, adding that it expected a run rate of Rs 50-70 crore of quarterly slippage going forward as well.

Retail slippage, however, was attributed to one-off factor of Rs 71 crore of education loans. Since the bank’s almost entire exposure in education loan is in the state of Kerala, a subvention scheme for small-ticket education loans (less than Rs 4 lakhs) announced by the state government resulted in a moral hazard problem and the bank had to recognise a part of the outstanding education loan in the troubled asset pool.

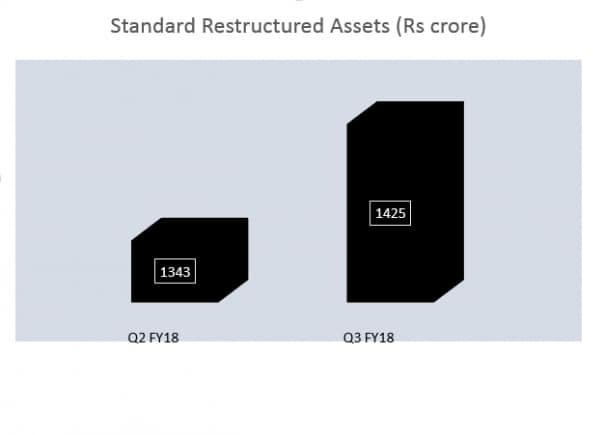

Slippage may remain elevated in the near term

The bank’s restructured book of standard assets is Rs 1425 crore and it expects the quarterly run rate of slippage to be of the order of Rs 350-400 crore in the near term.

Additional provision for Security Receipts

The book value of the outstanding Security Receipts (against assets sold to Asset Reconstruction Company) was Rs 870 crore and the bank carries provision of Rs 95 crore against it. As per the revised guidelines of RBI, banks will have to create provision against SR assuming the loans continued in the books of the bank. So as the recovery prospects of some of these assets worsens, the bank anticipates higher provision. This could impact near-term earnings.

However, on the operational front, the bank still appears to be doing a decent job.

Quarter at a glance

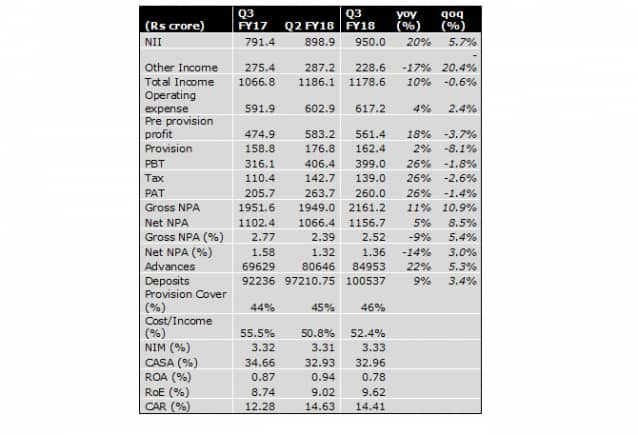

Federal Bank’s headline profit growth of 26% was driven by 20% rise in net interest income (difference between interest income and expenses) and stability in interest margin. Treasury gains were eroded by the sell-off in the bond market, but the early teen growth in core fees restricted the fall in non-interest income to 17%.

The bank was able to recover some part of its bad loans and this helped keep gross non-performing assets under check even though slippages rose. The bank’s provisions did not increase by much and that helped report a respectable profit growth.

Impressive performance on the business front

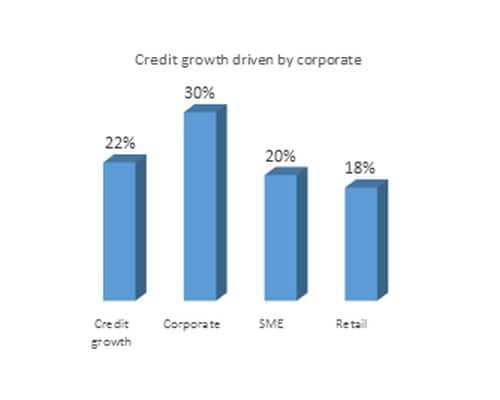

Business growth momentum remains strong with the advances book growing by 22% driven mainly by corporate. However, the bank still has a diversified asset book (40% wholesale, 38% retail and 28% SME) of a sound quality with 72% of the outstanding credit rated “A” and above. The bank is treading with caution and has decided to go slow on SME lending in its core market of Kerala after reassessment of risks.

The bank’s 80% outstanding book is MCLR (marginal cost of lending rate) linked and thanks to its lower cost of funds, it is able to compete and grow in this market without any negative impact on its interest margin.

However, Federal Bank needs to ramp up its low-cost deposit share to stay competitive. In the quarter gone by, while overall deposits grew by 9%, the low-cost (current & savings account) deposits grew by 4% leading to 170 basis points drop in CASA share to 32.96%. The bank targets to ramp up the same to 35%. The NRI deposits (40% of total deposits), however continued to be supportive, growing at a handsome pace.

High cost to income ratio is another area of focus as the bank has been relying on Relationship Manager led distribution model instead of branch banking in recent times. The management is reasonably confident of this ratio trending down in the future.

The bank is well capitalised that should help it embark on growth once the asset quality issues/provision get sorted in the coming quarters. The stock correction has rendered the valuation reasonable and we expect the near-term weakness to provide opportunity to buy into a decent dynamic private sector entity like Federal Bank.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.