Krishna KarwaMoneycontrol Research

SP Apparels Ltd (SPAL), a stock we initiated coverage on in the past, reported disappointing set of numbers from a year-on-year perspective because of Brexit-related headwinds, appreciation of the rupee vis-à-vis the pound, and GST-related uncertainties (particularly in case of the difference between duty drawback claimable and input credit available), among other seasonal factors.

In the last fortnight of June 2017, SPAL’s domestic retail (‘Crocodile’ garment sales) did not witness much traction as most of the company’s retailers chose to postpone purchases to Q2FY18 on account of lack of clarity on input credit claims under GST. Moreover, stocks amounting to Rs 4 crore were returned by the dealers to the company during this period.

Most of the amount allocated towards augmenting brand recall (through more ‘Crocodile’ stores across India) has not been disbursed yet, as seen in the exhibit below:-

Moreover, SPAL’s impetus efforts on backward integration is likely to yield results from FY19.

In addition to spending 54 crores on capital expenditure (as mentioned above) by FY18-end, the company will invest an additional sum of Rs 20 crore on purchase of sewing machines during the ongoing fiscal to boost its top-line.

Customer additions

During Q1FY18, SPAL added two US-based customers to its client list, whereas supplies to the French client are expected to commence in the next 2-3 months. The company signed agreements with Landmark Group and BH International for supply of garments as well.

Store expansion strategy

SPAL aims to increase its store presence to 160 large format stores (LFS) over the next two years from the current number of 145. To ensure better market penetration, higher returns on capital, and adequate product visibility, the company’s attention is gradually shifting from company- owned company-operated (COCO) stores to LFS (large format stores, target of 300 outlets in the next 2 years) and franchise-driven stores.

Product profile mix change

In recent times, SPAL has forayed into basic children wear and related products to facilitate better utilization of its manufacturing facilities. Until now, the company’s emphasis was primarily on fashion apparel, which not only requires more capacities but also yields lower output owing to comparatively lower utilization rates. By the end of FY18, the ratio of fashion products to basic ones is anticipated to change from 70:30 (at present) to 60:40. Consequently, a 15-20 percent top-line volume-driven growth seems probable without the need to install new machines.

Cash flow risk

SPAL’s foreign cash flow hedging policies are undertaken in a phased manner, wherein 60/20 percent of the transaction size is covered at the time of order receipt/shipment, respectively. For the remaining 20 percent, the company, being an export-focused business entity, is exposed to risks of rupee appreciation.

Valuation

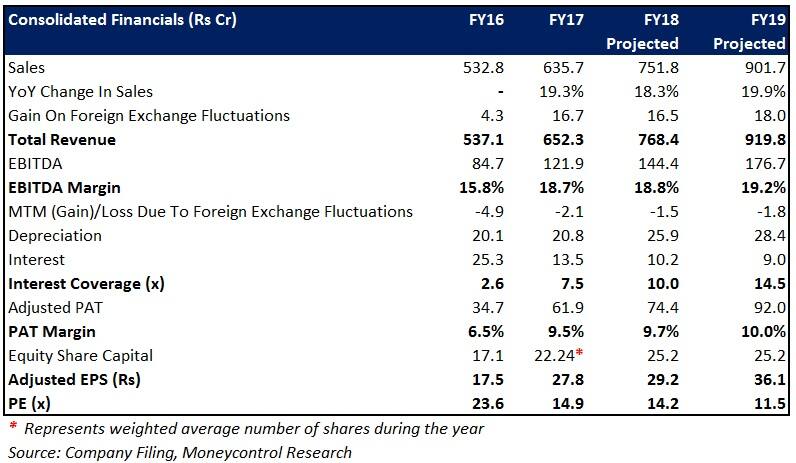

We expect SPAL’s FY18 numbers to remain fairly flat, since most of the company’s IPO funds will be locked in manufacturing upgradation processes till the end of the year. Repayment of debt during the fiscal, however, will strengthen the bottom-line, albeit marginally.

The company anticipates reaching the break-even point with respect to its ‘Crocodile’ garment retailing segment by March 2018. Starting H2FY19, the loss-making department may gradually start aiding the growth in operating margin. Revival of the same will be undertaken through reduction of overheads/advertising costs and reorientation of strategy.

At 11.5x FY19 projected earnings, though the stock appears to be reasonably valued, we suggest investors to adopt a gradual accumulation strategy, given definitive recovery may still take a while.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.