Vikas Khemani

We are in unprecedented times. Nobody in January would have imagined a complete lockdown of the world for an uncertain period of time along with such massive destruction of wealth. That’s what life is all about.

Risk means more things can happen than will happen. Currently, the world is grappling with these questions:

Q) How long and serious the COVID-19 spread can get; will it get worse before it gets better?

Q) How the lockdown will impact the businesses and economies structurally?

While answers to many of these questions are uncertain and will evolve with each passing day, one thing we believe is that the spread happened at a time when everyone was caught off guard.

Now that it’s a full-blown crisis, Governments and organizations around the globe have come out with full might to curtail the spread and find a cure.

And, it will be a matter of limited time before which it will either get curtailed through a cure or a pause in the spread of new cases or a combination of both.

We would assign a 50-60 percent probability to the world slowly opening up in May/June 2020 and India can even open earlier too. But, never forget the balance probability, so one has to be watching & agile to the evolving situation.

How will business and economies get impacted?

Currently, there are two risks that businesses are facing – productivity loss and liquidity crunch, with the latter one being far more detrimental! We believe companies with good balance sheets and flexible cost structures will be able to navigate through.

The RBI and Government will take counter-cyclical measures to support either specific industries or general businesses to tide over the liquidity squeeze.

But one can never be sure of the effectiveness of these measures, hence businesses with leverage and high fixed costs will be at high risk and will have to tread cautiously.

Our view on the markets - is it a good time to invest?

Very often, we get this question about how much more downside is left? Truthfully, the answer to this is known by none.

Mark Howard once said:

“When everyone believes something is risky, their unwillingness to buy usually reduces its price to the point where it is not risky at all. Consensus negative opinion makes it the least risky thing since all optimism has been driven out of its price.”

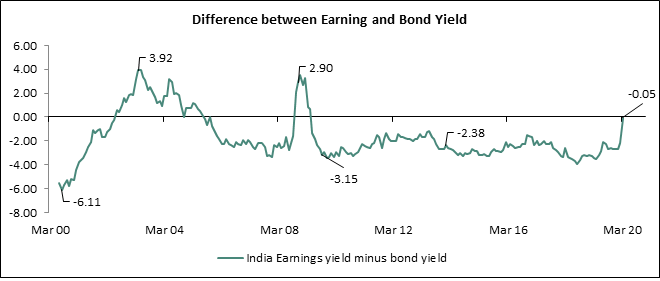

2) Earning yield vs Gsec spread (EY at 6.03% minus GY 6.07% is almost zero) – This ratio (EY-GY) is usually negative. A zero to positive ratio indicates either a significant & sharp drop in interest rates (like in the US/Europe post-2008 crisis) or significant correction in equities prices/valuation.

The positive ratio in a growth economy is hugely valued creative for equities, as equities will offer growth but bonds will not. Historically in such situations, Equities have offered good returns, once the immediate concerns settle down.

*10 Year Bond Yield

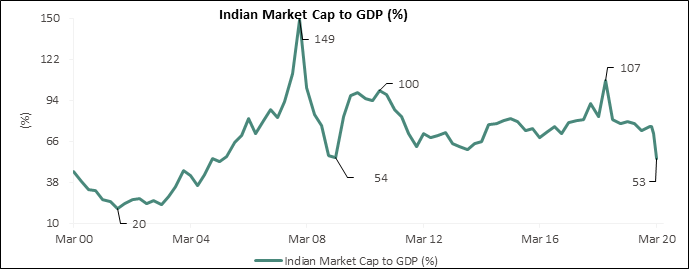

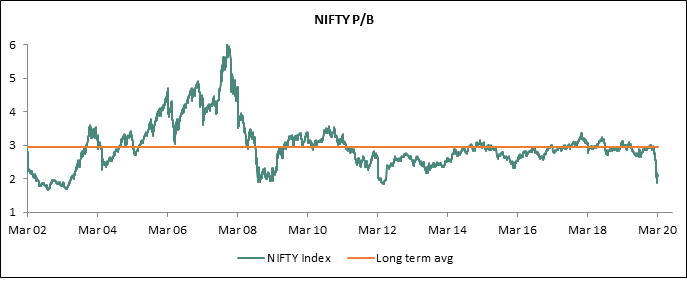

3) P/B Ratio (2.01) – at Nifty level, again is the lowest in the decade. Usually, the range is between 2-3x. Several businesses are available at 0.3 - 0.5x book, just because the earning power of these assets are temporarily impacted. However, this does not mean they will be permanently impaired. They will come back once normalcy returns.

In a nutshell, the risk-reward of investing in equities is surely favourable.

(The author is Founder Carnelian Asset Management)

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.