Brokerage houses remain bullish on the country's largest lender State Bank of India after healthy earnings in the September quarter with a significant fall in slippages.

They expect the stock to rally to Rs 420, implying a 49 percent upside from current levels, in the next one year.

While having a buy call on the stock, Jefferies raised its target price to Rs 385 from Rs 380, as the bank delivered a surprisingly strong quarter, especially on the asset quality front, the biggest worry plaguing the banking sector.

"Insolvency and Bankruptcy Code (IBC) recoveries could be surprising on the upside and keep credit costs under control. Valuations are attractive at 0.9x forward P/B for a 15 percent return on equity (RoE) by FY21," the brokerage said, adding it tweaked earnings estimate by (up) 6.8 percent for FY20 and (up) 0-1 percent for FY21-22.

Kotak Institutional Equities also retained its buy call on the stock and increased the target price to Rs 400 from Rs 390.

"Weak macro raised concern on asset quality but risks are manageable. FY20 should see a far better performance than FY19," it said.

The bank reported a more than three-fold increase in Q2 FY20 profit, despite higher provisions, with an improvement in asset quality. It included one-time gain of Rs 3,484 crore on sale of partial investment in SBI Life Insurance.

Net interest income grew by 17.7 percent year-on-year to Rs 24,600 crore, with loan growth at 9.6 percent.

Asset quality improved sequentially YoY. Gross non-performing assets (NPA), as a percentage of gross advances, fell 34 bps QoQ to 7.19 percent. Net NPAs, as a percentage of net advances, dropped 28 bps QoQ to 2.79 percent.

Fresh slippages fell significantly to Rs 8,805 crore in September as against Rs 16,212 crore in the June quarter. Slippage ratio also declined to 1.57 percent in Q2, down 126 bps QoQ, while credit cost dropped 6bps to 1.97 percent during the quarter.

Here is what other brokerages say about SBI:

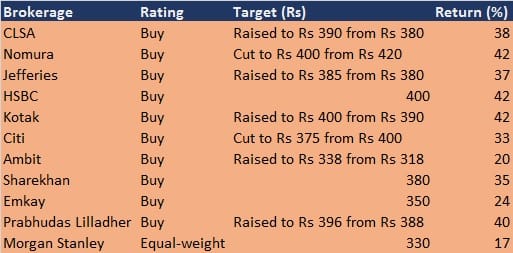

Brokerage: CLSA | Rating: Buy | Target: Raised to Rs 390 from Rs 380

The company remains a preferred pick among PSUs, but the risk in the telecom space is up. Dewan Housing will likely slip in Q3 and is now in its forecast. Potential offset is in the resolution of Essar Steel.

Savings deposit growth of 7 percent YoY is reasonable. CLSA has lowered its earnings estimates to factor in higher credit costs, while upside could arise from the monetisation of gains and resolutions.

Brokerage: HSBC | Rating: Buy | Target: Rs 400

The brokerage maintains a buy call on the stock, with a target price at Rs 400 as slippages moderate after a difficult Q1.

Contained stressed asset pool and high provisioning-cover provided comfort. NIM expansion surprised positively, but HSBC cut FY20/21/22 estimates by 3-4 percent due to higher operating expenses.

Brokerage: Citi | Rating: Buy | Target: Cut to Rs 375 from Rs 400

NPA recoveries and sustainability of NIM are key to stock performance. FY20/21 profit estimates lowered by 18 percent/6 percent, but valuations are attractive at current levels.

Brokerage: Ambit | Rating: Buy | Target: Raised to Rs 338 from Rs 318

The brokerage maintains FY20 estimates but has raised FY21 EPS estimates by 36 percent, factoring in lower provisions and higher NIMs.

Brokerage: Nomura | Rating: Buy | Target: Cut Rs 400 from Rs 420

The September quarter saw a beat on asset quality against muted expectations. It expects PPOP to post a 14 percent CAGR for FY20-21.

Credit costs normalisation should lead to RoE of more than 13 percent by FY21. Asset quality risk is 2.2 percent of loans, which is manageable.

Brokerage: Sharekhan | Rating: Buy | Target: Rs 380

Outlook positive for SBI, with strong capital adequacy (CET-1 at 10.08 percent) and possible value unlocking from its cards business (listing expected in the near term). It maintains a buy rating on the stock, with an unchanged price target of Rs 380.

Brokerage: Emkay | Rating: Buy | Target: Rs 350

Q3 could be eventful, with lumpy NPA recognitions (including DHFL) if not resolved, and also resolutions within NCLT (including long-hoped Essar Steel) and some power stress outside the NCLT. So, the outcomes of these exposures will be closely monitored.

The bank could be a net beneficiary of the migration to new tax regime net of DTA impact, an option which it may exercise in H2 to support profitability. The IPO of SBI Cards (36 percent RoE), which we value at around Rs 33,000 crore, will be launched by January 2020, leading to one-time gains.

We believe SBI's near-term stock performance will track the outcomes of lumpy corporate NPA recognition/resolutions. Maintain buy/overweight in Emkay Alpha Portfolio (EAP), with a target price of Rs 350 given its strong liability profile, higher retailisation, reasonable capital and return ratios among PSBs.

Brokerage: Prabhudas Lilladher | Rating: Buy | Target: Raised to Rs 396 from Rs 388

Key positive was much lower fresh slippages with all segments declining especially retail & corporate. Also outstanding SMA and stress account under new resolution framework saw marginal decline to 1.4 percent of loans versus 1.5 percent in Q1FY20. Operationally bank has been improving with near industry growth & upward NIMs trajectory, opex control and much better PCR and hence, has the ability to absorb hits from existing stress assets, although if additional assets come under stress earnings will see slower recovery. We retain buy with revised target price of Rs 396 (from Rs 388) on higher SBI life share in SOTP.

Brokerage: Morgan Stanley | Rating: Equalweight | Target: Rs 330

SBI numbers were good, but the outlook is tough in weak macro climate. Credit costs are likely to stay higher for longer, but valuation is attractive at 0.7xF20e book & 4x core pre-provision operating profit (PPoP).

Disclaimer: The above report is compiled from information available on public platforms. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.