Neha Dave & Krishna KarwaMoneycontrol Research

The Nifty today reached a fresh all-time high, six months after it last created a record high. The months in between have seen markets stay volatile, starting with a disappointing Budget and followed by continuing bank NPAs, uncertain political outlook, global factors (trade war/rising bond yields), besides a mammoth banking fraud.

To play safe, institutional and retail investors preferred large caps with a promising profitability potential and robust fundamentals. Midcaps and small caps bore the brunt of selling pressures.

With Nifty scaling the 11,000 mark again after a gap of over 5 months, we analysed market trends since January 2018. Our findings suggest the following:-

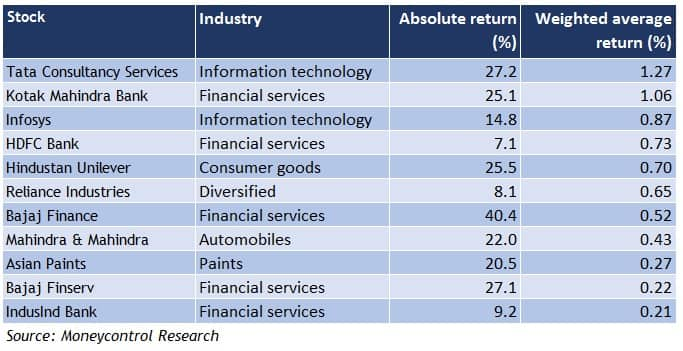

A narrow market with handful gainers

Only 19 stocks in the Nifty outperformed the index with positive returns. From a weighted average return perspective, 5 of the top 11 performers are from the retail-focused financial services industry alone.

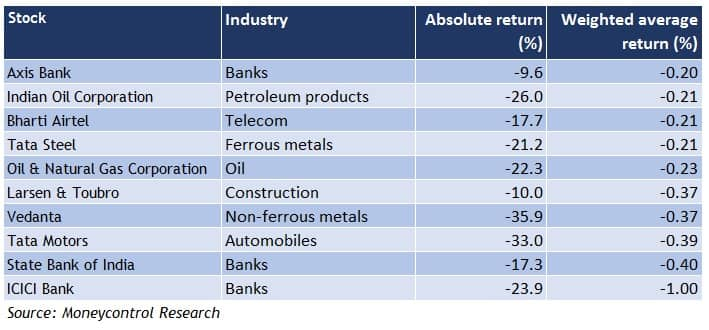

The laggards

31 stocks, comprising more than 50 percent of the Nifty, underperformed the index. In terms of weighted average returns, the bottom 10 list was led by some of India’s leading banks that have high exposures to the corporates.

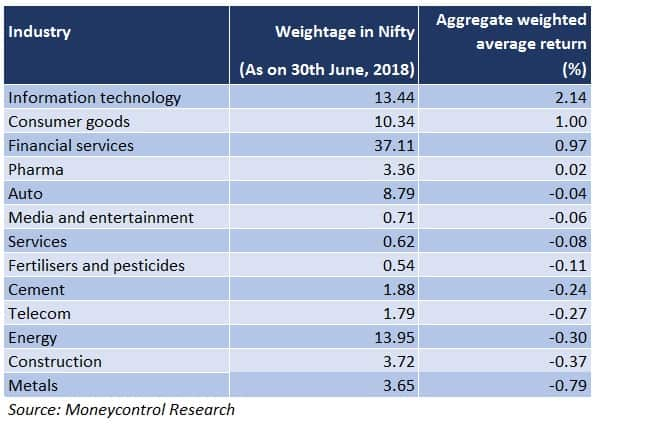

Sectoral performance

Information technology companies, that faced a myriad of headwinds in the past, appear to be on a growth path again, which is reflected in their price performance. Investors reposed faith in some reliable consumer-oriented names (HUL, Asian Paints), notwithstanding their steep valuations.

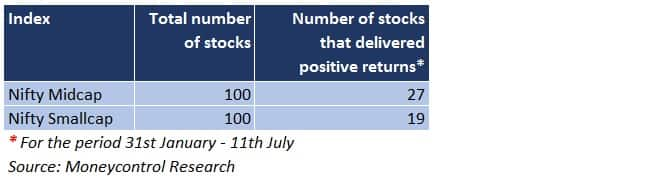

Mid and small caps – a very different picture from Nifty

Market volatility since February 2018 took a big toll on the relatively ‘riskier’ names across all sectors, albeit in varying degrees. Corrections in the mid and small cap space were primarily attributable to the valuation mismatch – the steep premium enjoyed by a section of such stocks was not wholly supported by a similar earnings trajectory.

This fact is further corroborated by the price performance observed in the constituents of the Nifty Midcap and Nifty Smallcap indices, as seen below:-

So, in contrast to the Nifty, only 27 percent of midcap and 19 percent of smallcap stocks delivered positive returns.

Fallout on mutual fund performance

While Nifty has sky-rocketed, the performance of most mutual fund (MF) schemes is painting a different picture. Most large cap MF schemes are underperforming i.e. generating returns less than the benchmark or the index, year to date.

To safeguard investors interest, a couple of stringent regulations by SEBI has made it difficult for MFs to beat the benchmark. Index’s skewed performance driven by a few stocks has further added to the woes of MF schemes.

First, SEBI has mandated all equity schemes to benchmark their performance against a total returns index (TRI). TRI indices are calculated after adding back the dividends in the underlying companies. In effect, this results in a higher hurdle rate for fund managers as the return of TRI indices are typically 1.5-2.5 percent higher than regular indices. So the under-performance of MFs is worse when the TRI is considered.

Second, SEBI defined and tightened fund categories, thus causing all MFs to accordingly re-classify their investments. For instance, a large cap fund will now have to invest at least 80 percent of its corpus in the top 100 largest companies. In effect, this restricts the fund manager’s ability to generate alpha (excess return over the respective benchmark) by choosing many stocks outside the benchmark. In the past, many funds resorted to buying mid cap and small cap stocks in a large-cap fund to generate higher returns. Now, the way out for MFs could be relying more on sector allocation than stock picking to generate higher returns. But, that again is a double-edged sword and can lead to significant underperformance.

What does this mean for investors?

Though not consciously, Nifty index ends up following a so-called momentum style of investing, where stocks that have done well in the recent past are included in the index, while laggards within the Nifty are periodically dropped. As a result, the additions come in at relatively higher valuations, while the discards will have good value. So, the current performance of Nifty will hurt investors following a contrarian strategy of buying low and selling high.

In a volatile and tilted market, investors would be better off investing through index funds or index exchange-traded funds (ETFs), where the fund mimics the index. More importantly, the expense ratio of passive funds (index funds and ETFs) is much lower compared to actively managed funds, which, in turn, can yield better returns.

Globally, passive investing is very popular and attracts a giant share of inflows every year. If index’s performance continues to be lopsided, passive investing will reward investors handsomely in India too.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!