P/E is 24.25x while industry P/E is 37.34x.")

Ruchi Agrawal

Moneycontrol Research

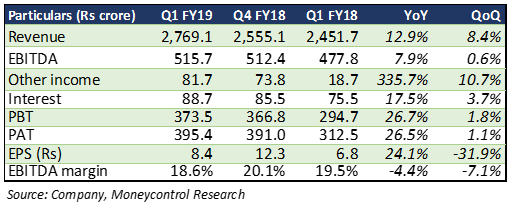

Tata Chemicals (TCH) reported a healthy 13 percent year-on-year (YoY) topline growth, aided by a strong growth in the domestic business, despite a weaker performance in the international business, especially US and Kenya. The consumer products segment saw a strong 33 percent sales growth. While the soda ash business saw improved realisations, volumes remained low due to one-off events. Its energy bill remained a concern and ate into profits. Net profit saw an uptick with extraordinary uptick in other income.

Results at a glance

Volumes in the chemical business impacted

Global demand for soda ash has been strong due to which there has been an uptrend in soda ash prices, which led to improved realisation for the segment. However, a plant shutdown in the US, flood like situation in Africa and an exit from its European soda ash trading business resulted in 10 percent YoY fall in overall soda ash volumes, offsetting this benefit. The management said these one-off events have now settled and Q2 should see an uptick from spillover demand.

Energy expense is a major head under the soda ash business. Energy cost has been going up due to rising oil and coal prices and is eating away a portion of the segment’s profitability.

Strong growth in consumer product and specialty chemical businesses

Consumer products business saw a strong performance for yet another quarter, with a 33 percent uptick in revenue, aided by improvement in both realisation and volumes. Economies of scale with higher volumes also brought in a 302 basis point margin improvement in this segment. Last year’s low base also played a part in making the uptick look stronger. The management is looking to aggressively expand this segment with various new launches lined up and expects revenue to touch Rs 500 crore in the next 5 years (currently around Rs 200 crore).

Specialty chemical business reported a healthy 25 percent sales growth led by strong topline growth in Rallis India and an overall low base last year. The management said new projects announced in Nutraceuticals and highly dispersible silica (HDS) will be major growth drivers in the coming years and plans to invest around Rs 30 crore in this segment.

India business stays strong

Domestic operations have seen a around 23 percent growth due to healthy performance by the domestic basic chemical business. Improving margin with better realisation has helped in consistently expanding margin since the last two quarters. This has more than offset the impact of contracting soda ash volumes.

International business

North America: Planned plant shutdown for maintenance during the quarter gone by resulted in lower soda ash volumes to the tune of 25,000 million tonne. But the rupee depreciation versus the dollar worked in favour of realisations.

Africa: Unfavourable weather and heavy rains impacted plant operations, resulting in lower volume offtake. However, the demand-supply mismatch helped push up per tonne realisations.

Europe: Rupee deprivation versus the euro helped improve realisations while volumes in the traded soda ash business declined 22 percent YoY. TCH has now exited the low margin trading business. This is expected to further compress annual volumes. However, we expect margin to improve going forward.

Rallis India’s performance

Rallis India reported a healthy Q1 FY19 with a significant (24.8 percent) growth in revenue, led by strong volume growth in the domestic pesticide business. While some of this can be attributed to a low base due to Goods & Service Tax-related disruptions last year, overall growth rate is still strong for an agri business. Growth in the seed business remained largely soft at 11.3 percent YoY.

Outlook

TCH has now completed all major restructuring. Its exit from the fertiliser business has freed up working capital and made the standalone balance sheet debt free. Going forward, the management intends to deploy available cash for expansion of the specialty chemical and consumer products portfolios, which have better margin and capability to drive growth. This would be something to watch out for.

The stock has surged around 9 percent in the last one month and is 8 percent below its 52-week high. It is trading at FY19e enterprise value-to-earnings before interest, tax, depreciation and amortisation of 7.8 times. Stabilisation after one-off incidents across geographies would be something to watch out for. A successful deployment of capital in high margin businesses can improve earnings and trigger a re-rating in the stock.Follow @Ruchiagrawal

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.