Sachin Pal

Moneycontrol Research

Highlights:

- Top line growth came in excess of 20 percent

- Volumes were strong across both its business segments

- Gross margin under pressure due to higher input costs

- Lower advertising spends gave cushion to the margins- Valuations favour investors from a long-term perspective

-------------------------------------------------

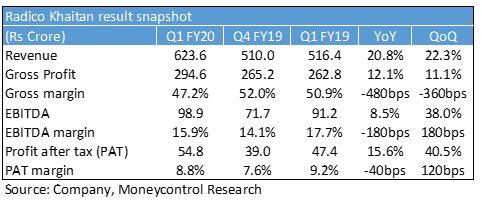

Liquor manufacturer Radico Khaitan delivered an impressive set of earnings in the first quarter of FY20. The top line growth in excess of 20 percent was quite heartening, considering the liquor restrictions during the general elections season. Operating profit, however, was weaker than revenue growth due to sharp increase in input costs.

Quarterly earnings highlights

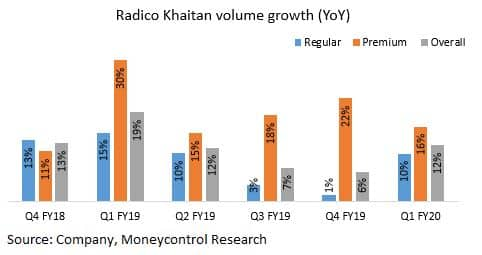

Radico’s top line increase of 21 percent to Rs 624 crore was aided by volume expansion across its premium and non-premium segments. The overall volumes for the quarter came in at 6.25 million cases, representing a growth of 12 percent year-on-year (YoY). Premium segment, which comprises Prestige and above, drove the overall volumes -- with a growth of 16 percent YoY. Popular segment also had a healthy quarter as it clocked double-digit volume growth.

As highlighted earlier, hardening of key raw materials (extra neutral alcohol and glass bottles) weighed on the gross margin, which declined significantly during the quarter. Although gross profit was 12 percent higher, the margin contracted from 50.9 percent in Q1 FY19 to 47.2 percent in Q1 FY20.

Prices of extra neutral alcohol (ENA) continue to be on an uptrend and increased by 3 percent on a sequential basis. ENA prices have touched Rs 55 per litre after having seen a sharp increase of 19 percent in the past 12 months. Similarly, glass bottle prices are 15 percent higher than the previous year. Additionally, Radico faced additional cost pressures due to capacity restrictions at its in-house molasses manufacturing plant.

Cost control measures helped Radico mitigate margins pressures at the operating level. Earnings before interest, tax, depreciation and amortisation (EBITDA) margins declined 180 bps (vs 480 bps decline in gross margin), but operating profit increased 8 percent YoY to Rs 99 crore. Advertising and sales promotion expenses rose just 5 percent YoY and the company spent around Rs 38 crore on the same during the quarter.

The packaging costs appear to have stabilised, but the prices of extra neutral alcohol are on an uptrend due to ethanol blending policy and sharp spike in agri commodity prices. Inputs costs are anticipated to inch up further and could affect gross margins in coming quarters.

However, the management has indicated that the recent price hikes in certain states (Rajasthan, Maharashtra, Tamil Nadu etc.) along with deeper and wider penetration in the premium segment should assuage the concerns on the cost front. Also, the Central Pollution Control Board has allowed the company to restore the operating capacity of its molasses plant from 77 KLD to 200 KLD and this should lend further support to its margins in coming quarters.

Interest expenses have come down as a result of consistent debt reduction. During the quarter, the company repaid Rs 18 crore of loans and its outstanding net debt at the end of Q1 stood at Rs 301 crore. The repayment rate in Q1 was considerably lower in comparison to earlier quarters as the working capital ballooned due to inventory build-up in Andhra Pradesh, Telangana and the Canteen Stores Department.

The new government in Andhra Pradesh (AP) has decided to gain operational control over the liquor retail store operations in the region. AP contributes around 10 percent to Radico’s top line and therefore, we anticipate a rejig in its supply chain in the region on the back of this latest development.

Outlook and Recommendation

Demand prospects seem very exciting from a medium to long term perspective, but near-term challenges such as slowdown in consumption, excise duty revisions, liquor ban in Andhra Pradesh loom as the sector continues to be under the regulatory ambit of the government.

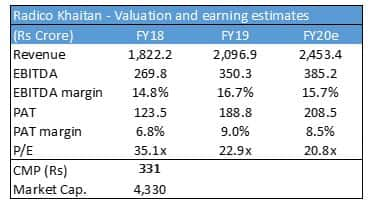

Radico Khaitan’s portfolio expansion and premiumisation strategy have helped the company double its earnings over the past couple of years. Considering the opportunity size and scope of penetration, the company has the potential to expand at a healthy pace over the next few years. However, we anticipate the pace of earnings to moderate (15 percent +) because of high base and inflationary cost pressures.

The company offers an interesting investment opportunity at current levels as the stock is trading at a FY20 price-earnings multiple of 21x, which is at a significant discount of the sector leader – United Spirits. Deleveraging as well as portfolio premiumisation remain the key triggers for growth and improvement on both aspects could trigger a multiple re-rating in the long run and, thereby, narrow its valuation gap with the market leader.

Also read: This stock could be the next Havells

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.