The wedding industry is witnessing a significant shift, with millennials opting to self-fund their special day, not wanting to burden their parents. While this gesture is thoughtful, it's most feasible when the couple has already set aside funds; otherwise, they need to borrow.

To cover escalating costs, couples are increasingly turning to personal loans specifically tailored for wedding financing.

The key drivers for a wedding loan trend are the desire for personalisation, unique experiences, and destination or themed weddings, which are driven by the need for validation and 'likes' on social media such as Instagram.

According to the IndiaLends Wedding Spends Report 2.0, about 26 percent of brides and grooms who plan to self-fund their weddings consider personal loans. Of those considering borrowing, 68 percent plan to borrow between Rs 1 lakh and Rs 5 lakh. The survey, which polled 1,200 millennials, was conducted in October–November 2023.

Factors pushing couples to seek wedding loansThe latest survey ‘Destination 'I Do’ by Skyscanner, a global travel app, sheds light on India's growing love affair with destination weddings. It’s gaining popularity among Gen Z and millennial couples. About 85 percent of respondents to the survey were in the middle of planning or had experienced a destination wedding. The survey took place in July 2024 and involved 2,000 respondents from India.

“Destination weddings come with added pressures, including flying guests to remote locations, hiring wedding planners, booking luxury group stays, and creating elaborate decor – these expenses often necessitate wedding loans,” says Krishan Mishra, CEO, FPSB India, the Indian subsidiary of the US-based Financial Planning Standards Board Ltd.

“The convenience of flexible loan options and rapid approvals makes wedding loans an enticing option for financially independent couples,” says Gaurav Chopra, founder and CEO of IndiaLends, a fintech lender.

Also read | Marriage & money: Why coming together is crucial, moneywise

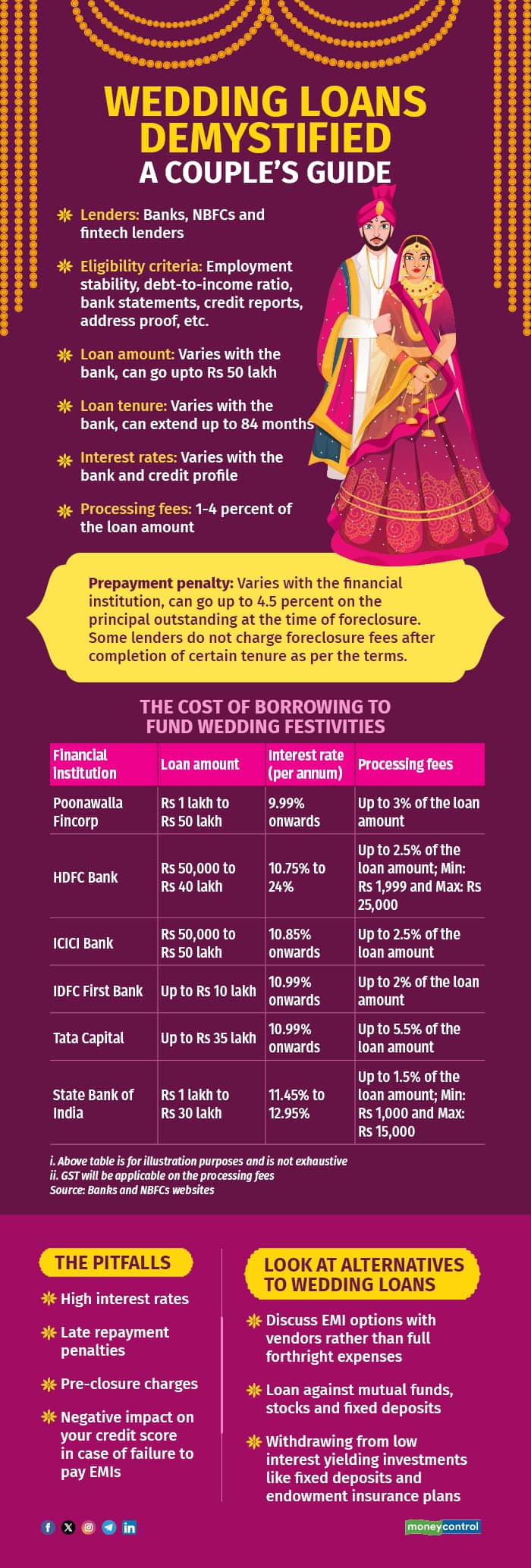

Wedding loans are treated as personal loans by banks, non-banking financial companies (NBFCs) and fintech lenders, with similar eligibility criteria. “To qualify, borrowers typically need a good credit score, preferably above 730, as it demonstrates responsible credit behaviour,” says Chopra. Lenders also require proof of a steady income and recent bank statements. Additionally, a strong repayment history—without missed or delayed payments over the past 1 to 3 years—is crucial.

“Before opting for a loan borrowers should evaluate their own financial situation to ensure they can comfortably manage the loan repayments,” says Chopra.

Also explore: Online personal loan up to Rs 15 lakh via Moneycontrol

Before signing: Crucial loan terms to knowThe borrowers must know the interest rates, processing fees, pre-payment clause and other charges before signing on the loan agreement.

Interest rates for wedding loans generally range from 9.99 to 24 percent per annum, depending on the borrower’s credit profile, loan amount, and tenure. The processing fee is 1 to 4 percent of the loan amount (see graphic).

These loans have a repayment tenure of 12 to 84 months (varies with the bank). “Missed payments or defaults on unsecured loans can lead to significant consequences, including penal charges, a negative impact on your credit score, and potential legal action by the lender,” says Chopra.

For instance, at the State Bank of India, any prepayment of EMI in full or in part and closure of the account before the end of term attracts the prepayment charges of 3 percent on the outstanding amount. Similarly, Tata Capital charges 4.5 percent on the principal outstanding at the time of foreclosure.

The primary drawback of wedding loans is high interest rates, just like any other personal loan. “Failure to repay or delay in payment of instalments can lead to heavy penalties,” says Gaurav Goel, an investment advisor registered with the Securities and Exchange Board of India. This can also lead to trimming of the credit score. “A poor credit score can make it difficult to access loans in the future, as well as lead to higher interest rates,” says Chopra. Foreclosing the loan before maturity comes with substantial charges.

Also read | Marry Now, Pay Later? Why wedding loans are not a match made in heaven

The wedding loan checklistCouples should assess their long-term financial goals, for example, putting something aside for buying a house, contingency, family planning, asset creation, or retirement, prior to focusing on a wedding loan. “They should evaluate their ongoing commitments, for example, repaying student loans, and assess if they have a practical arrangement to pay back the loan,” says Mishra. Making a wedding expenditure plan that adjusts comfortably with the wants and financial well-being of the couple is crucial to stay away from financial burden right after the wedding.

“Another important and practical consideration should be to consider the financial burden of wedding loan EMI payments in case any events like birth of a child, job loss, medical emergencies, demise or separation,” says Goel.

Also read | How to plan your wedding on a budget: 5 handy tips for smart spending

Alternatives to wedding loansMake your wedding more budget-friendly by cutting back on extravagances. “Choose local venues and community centres over distant destinations and pricey hotels/resorts,” Goel advises.

“Families and couples should consider saving ahead of time, utilising individual reserve funds,” adds Mishra. Discuss EMI options with vendors rather than full forthright expenses, he adds.

“There are also options where lenders offer loans against stocks and mutual fund investments. You can consider these options instead of a personal loan for wedding,” says Chopra. The interest rates on secured loans are lower compared to unsecured loans for wedding.

“You can also consider withdrawing from low interest yielding investments like fixed deposits and endowment insurance plans,” adds Goel.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.