Valuing the insurance business is an especially complex affair. Understanding of the terms and parameters is still evolving, as there are only six listed insurance companies at present in India.

The Life Insurance Corporation of India (LIC) will join this list soon, once its ongoing initial public offering (IPO) concludes and the insurance behemoth is listed on the bourses.

Studying the basic parameters is crucial for investors, especially policyholders, who have set their sights and hearts on this mega public issue. Billed as India's largest IPO, with an issue size of Rs 21,000 crore, it has enthused many policyholders who have been long-term customers of LIC. They hope that they will get a chance to own a stake in the bid daddy of stock markets through the ‘policyholders’ quota’. On day one of the mega issue, the policyholder's reservation portion was oversubscribed 1.99 times.

Many policyholders happen to be first-time equity investors with little or no understanding of equity and IPO investing, let alone being able to value insurance companies. “Most terms used in the insurance space are less-commonly-known compared to those used in other industries. For instance, for banks, parameters such as interest rates and Net Interest Margin (NIM) are well-understood,” says Siji Phillip, Senior Research Analyst, Axis Securities. This is not the case with embedded value (EV) or value of new business (VoNB) margins that are key to valuing insurers.

Insurers’ valuation process varies significantly from that of other industries. “The biggest difference is that the valuation requires projection of future cashflows from the existing book. Unlike other industries, the profit generated from a single sale is realized over a long period of time which can range from 1 year to 100 years depending on the type of product sold to the customer,” says Rahul Jain, an NCR-based consultant actuary.

Also read: How LIC’s IPO has pushed a race for new demat accounts

Here’s a simple-to-understand guide on some of the key parameters for policyholders opening their maiden demat accounts to invest in LIC IPO.

Embedded Value and return on embedded value (RoEV)

This metric is central to the process of valuing an insurance company. Embedded value (EV) is the sum of the present value of the insurer’s future profits and its net worth (total assets minus the liabilities). “Unlocking of the value in insurance companies takes a long time, so investors need to keep an eye on the movement of EV,” adds Jain.

Once a company announces its IPO, the EV, as computed by the actuary-in-charge, will find a mention in the offer documents. But EV by itself won’t be the determining factor. The bidding process throws up a price band. LIC's red herring prospectus reveals that the company's EV is pegged at Rs 5.5 lakh crore. At the upper IPO price band, the insurance colossus is now valued at Rs 6 lakh crore, or 1.1 times its EV.

In case of a listed insurer, EV, along with the company’s market capitalisation and price, will give you the EV multiple, which will hold key. “Broadly, I would say market price of three times the EV can be considered a sort of a benchmark. Anything above that is slightly expensive, while anything below that can be considered reasonably priced. Currently, amongst listed players, one-year forward price to EV multiple of HDFC Life is over three times. SBI Life is more reasonably balanced with market price-to-EV multiple of less than three times,” says Philip. From an investor’s perspective, there is a greater scope of expansion in EV multiple when an insurer is yet to touch the three-times-EV threshold.

“RoEV is another important measure of a company's valuation. Think of this as how much profits a company is able to release each year out of the embedded value it has locked in. Thus it represents the efficiency with which the company is running and also validates the assumptions the company has built into its Embedded Value and mathematical reserves,” says Jain.

Also read: Explained: Here’s how LIC’s valuation process will be conducted

VNB multiple and margin

Value of new business (VNB) is often termed embedded value at the point of policy sale – it represents the present value of future profits from policies issued in a specific period. “It is the amount of additional EV a company generates by writing new business in a financial year/quarter,” explains Jain.

Market price-to-VNB multiple also plays a key role in life insurance valuations. “When we compare the market price-to-VNB multiple, again, HDFC Life’s one year forward expensive at 41 times, while it’s around 32 times for SBI Life and ICICI Prudential Life Insurance,” says Philip. According to her, HDFC Life commands a premium because of “innovative products.”

As an investor, you need to keep an eye on the value of new business (VNB) margins too. It is the profit margin at which new business is being written. “This is the additional VNB generated for every Rs 100 premium of new business written by a life insurer,” says Jain. Higher the margin, the more favourable it is for the company and its shareholders.

Agency strength

Bancassurance channel – that is, selling policies through partner banks – gets a higher billing compared to other channels, though individual agents, too, help diversify the customer profile. “Bancassurance channels largely get metro clients while individual agents account for tier-I and tier-II clients,” adds Philip. Banks provide an opportunity to cross-sell insurance products, making the process simpler for partner insurers. “This channel has played a key role in boosting private insurers’ market share. Also, in the last two years, online channels have picked up pace and private players have benefited. LIC, on the other hand, is continuously losing market share,” says Philip.

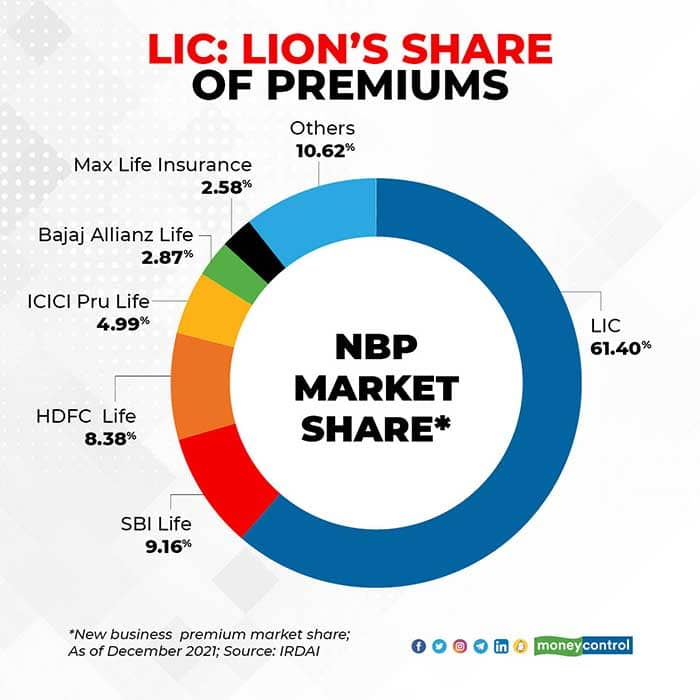

Market share

Though LIC remains the leader by distance with a market share of over a whopping 61 percent in new business premium collections, the downtrend necessitates caution. “The mammoth market needs to sustain and grow for the investors to benefit for investing in LIC IPO. It remains to be seen if it can attract millennials who prefer new-age channels to buy policies,” she adds. Keep an eye on the APE (annualised premium equivalent) growth. APE is the sum of regular, annualised premium from new business earned during a particular period and 10 percent of the new single premiums collected in that period.

Product mix

Product categories impact VNB margins and are hence critical while evaluating a company’s business. “Generally, protection plans (primarily term plans) have higher VNB margins, followed by Ulips. So, when a life insurance company increases its share of protection plans, it is a positive indicator,” says Philip. And, in the backdrop of COVID-19, people are realising the need for protection policies, which has already pushed up demand. This trend is likely to continue with greater vigour once COVID-19 is out of the picture.

Persistency ratio

A higher persistency ratio is a favourable metric – typically, 13th and 61st month persistency ratios are taken into account. It indicates the insurer’s customer retention record. “Higher persistency ratio means that customers are paying their premiums on a regular basis. Insurers are able to reduce their costs as the renewal premiums are coming in without the company having to do additional sales and marketing,” explains Philip.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.