Since the launch of Nifty BeES in 2001, the Indian financial markets have witnessed the rise of index funds and ETFs. Over the past two decades, 406 index funds/ETFs have been introduced, with 36 of them tracking the Nifty 50 index alone. These products provide a reliable way to replicate broad market benchmarks at a fraction of the cost typically charged by traditional mutual funds.

Investing in alternative equity-linked products, such as direct equity or actively-managed mutual funds, introduces additional risks related to the manager or company, which should ideally be compensated with superior returns. In simple terms, if an investment doesn't deliver excess annual returns (or alpha) of at least 1.5%-3% over the benchmark, it doesn't make sense to look beyond index funds or ETFs.

Also read | New Income Tax Bill: No changes in capital gains tax structure, but language simplified

While investors historically relied on traditional mutual funds for alpha generation, recent data indicates that actively managed funds have often struggled to consistently outperform their benchmarks.

As observed, alpha for large-cap funds has largely diminished over the past 20 years, now delivering less than 1%. Even mid-cap mutual funds, which generated significant alpha until about 10 years ago, have seen their outperformance shrink (with just 0.74% alpha over the past decade). This trend aligns with market efficiency, which has been driven by increased analyst coverage and a surge in retail participation. In fact, in five out of the past 10 years, mid-cap funds have delivered alpha of less than 1.5%. While some funds in these categories have clearly outperformed their benchmarks, selecting the right fund comes with significant negative alpha risk. For instance, in five out of the last 10 years, more than 50% of large-cap funds underperformed their benchmark.

Additionally, the rankings of mutual funds within categories are highly unpredictable, exposing investors to frequent churn and capital gains tax liabilities. For example, the top-ranked large-cap fund in 2022 was ranked 27th out of 31 in 2023. Similarly, in the mid-cap space, the top-ranked fund in 2022 dropped to 22nd in 2023 and was ranked last (30th) in 2024. In categories like mid-cap, the return divergence among funds can be extreme, leading to substantial opportunity costs in the case of poor manager selection. For example, the best-performing mid-cap fund in 2024 returned 59%, while the worst returned only 11%. This volatility often leads investors to frequently churn their portfolios, which erodes potential compounding due to the associated tax implications.

Also read | Gold prices at record high: Look for price dips for accumulation, stagger investments

Disillusioned by the subpar excess returns from mutual fund investments and the challenges of manager selection, many investors are turning to factor investing as an alternative way to add alpha to their portfolios. At a basic level, the potential for excess returns through factor investing makes sense, as the stock selection process already involves evaluating various factors such as volatility, dividend yield, alpha, momentum, quality, and value. As a result, the final portfolio tends to be biased toward securities that score highly on one or more of these factors, based on the belief that these factors will lead to superior returns.

Factor investing standardizes this performance-driven decision-making by providing exposure to a concentrated portfolio of stocks that are rich in specific factors, or a combination of factors, with a proven track record of delivering excess returns. As shown in Table 2, factors such as quality, volatility, and value—while maintaining a risk profile similar to the Nifty 100—have consistently outperformed the benchmark by 1.5% to 3%.

Additionally, factor investing eliminates manager selection risk, as all factor index funds tracking a particular factor tend to provide the same returns (ignoring the expense ratio). This makes factor investing much more reliable than traditional mutual fund strategies, where there is often considerable divergence in performance within the same category.

That said, factor investing also carries inherent timing risk. As illustrated in Table 2, the excess returns from the quality factor have notably diminished in the 2020s. When a factor generates strong outperformance over an extended period, it becomes increasingly recognized by the market, leading to a natural decline in those excess returns. After a phase of subdued alpha, market interest typically wanes, creating valuation discrepancies that set the stage for a potential resurgence in outperformance. This cyclical behavior is a universal phenomenon across markets, with nearly every factor going through similar phases. To manage this timing risk, investors are advised to diversify their portfolios across different factors with comparable risk profiles.

Also read | New Zealand revises 'golden visa' rules. Do wealthy Indians stand to gain?

Fortunately, the Indian investment landscape remains largely dominated by active stock-picking and sector rotation strategies. This ensures that, despite occasional low-alpha cycles, factor alpha will likely continue to thrive over the next 10-15 years.

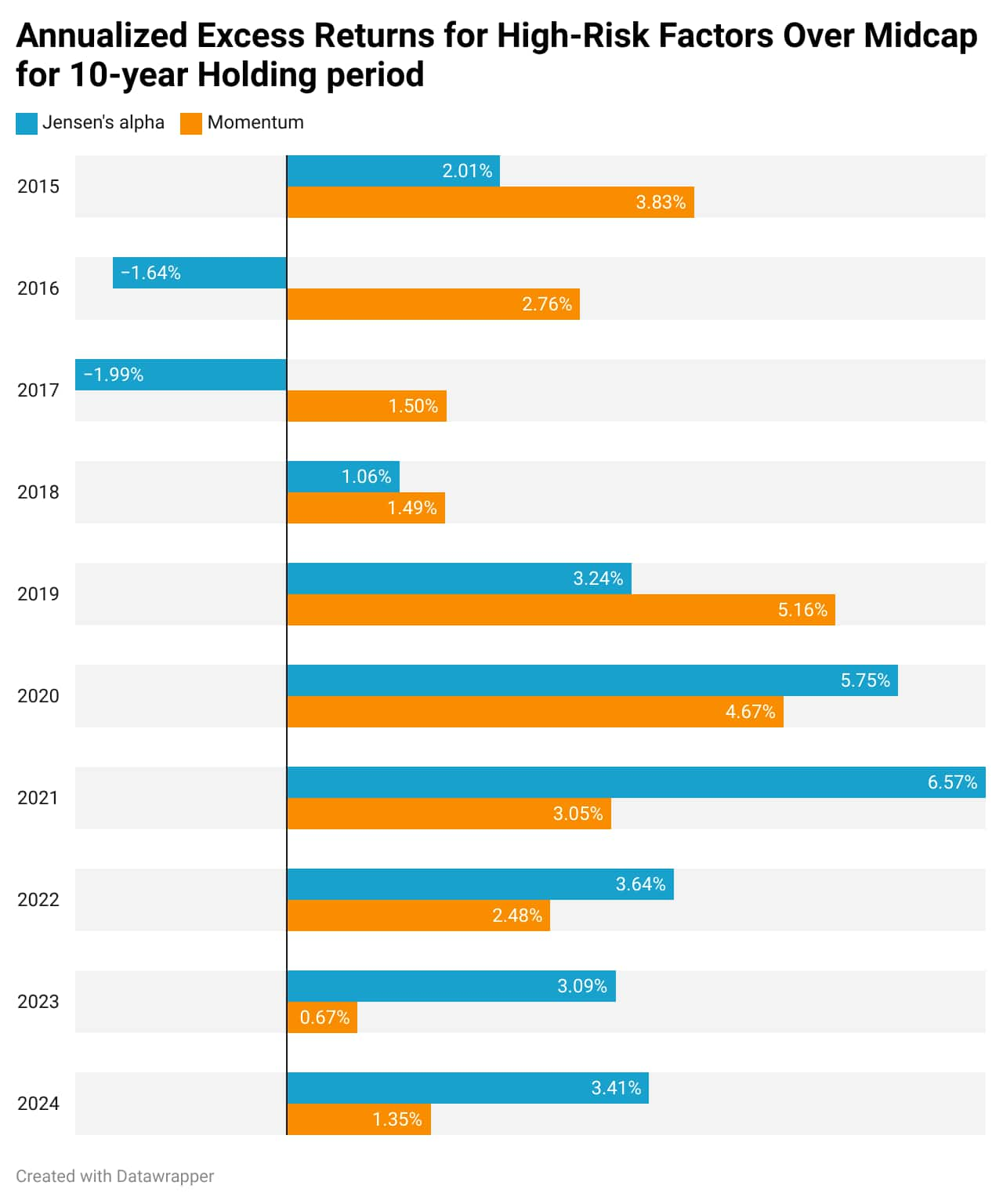

In addition to individual factor cycles, broad market cycles also influence factor returns. Low-risk factors tend to deliver excess returns during bearish market phases, while high-risk factors often experience a spike in excess returns during bullish phases. For high-risk investors aiming to capture returns similar to the mid-cap or small-cap space, factors like Jensen’s Alpha and Momentum offer a potentially more reliable means of adding excess returns to their portfolios.

Both Jensen’s Alpha and Momentum have delivered impressive annualized excess returns of over 1.5% in 7 out of 10 sample periods. One key takeaway is the significant divergence in the excess return statistics between these two factors. For investors seeking excess returns over the mid-cap benchmark, combining Jensen’s Alpha and

Momentum could offer a more reliable path to outperformance than traditional mutual funds.

The alpha potential of factors has gained widespread attention in recent years, with over 100 ETFs and index funds launched in the market over the past five years. This expansion makes it easier for investors to build a diversified, factor-centric portfolio with greater control—something traditional mutual fund portfolios often lack. Even for sophisticated investors, factor investing represents a powerful wealth-building tool, allowing them to strategically rotate risk across factor cycles in a cost-effective and efficient manner, further amplifying the already significant outperformance these factors offer.

Also read | This too shall pass: How to navigate market movements in turbulent times

The author is co-founder and CIO of EleverDisclaimer: The views expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.