Health insurance policyholders – existing as well as new – have a reason to cheer in the new financial year.

The Insurance Regulatory and Development Authority of India (IRDAI), as part of its product regulations overhaul across insurance segments, has tweaked some crucial norms for health insurance policies.

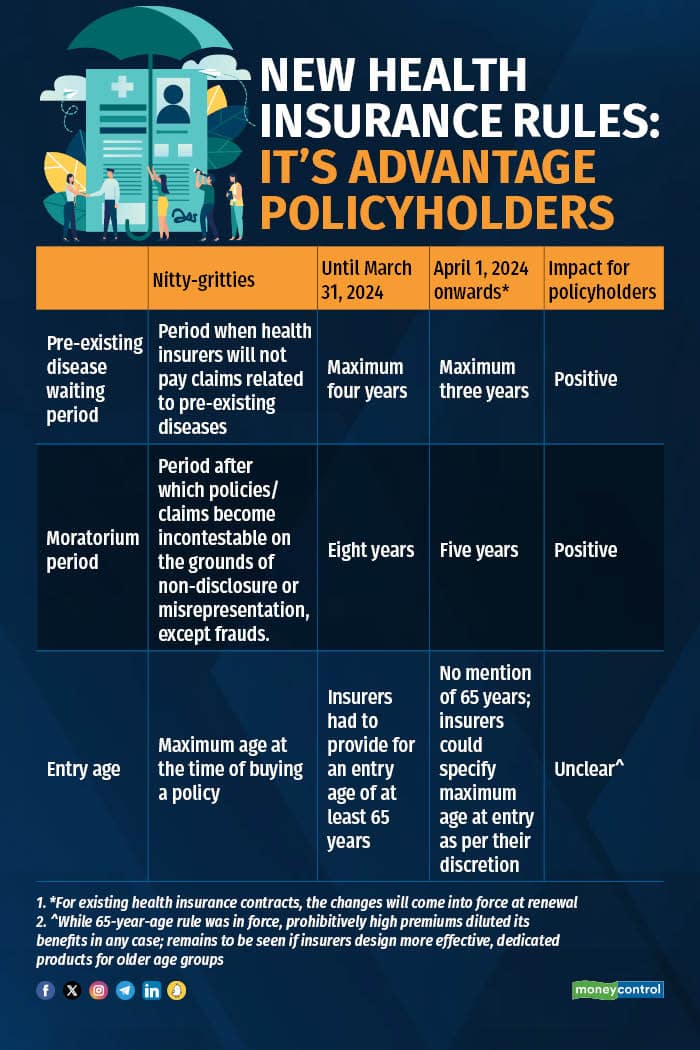

Here are the key changes in provisions that will affect health insurance policyholders.

Anxiety-free claims after five policy yearsFor one, it has reduced the moratorium period for claims under health insurance policies from eight years to five years. “After completion of sixty continuous months of coverage (including portability and migration) in health insurance policy, no policy and claim shall be contestable by the insurer on grounds of non-disclosure, misrepresentation, except on grounds of established fraud. This period of sixty continuous months is called as moratorium period,” the IRDAI regulations say.

Put simply, if you pay your premiums continuously for five years, your insurance company will not be able to reject claims citing failure to disclose your health status. For example, not disclosing pre-existing conditions such as diabetes, hypertension, Asthma and so on can result in claim rejection even if your hospitalisation cannot be traced to these ailments. Insurers can not only repudiate claims but also cancel the policy citing non-disclosures.

Until March 31, 2024, policyholders had to wait for eight long years for this clause to kick in and their claims to become incontestable. “This is a policyholder-friendly move. Eight years was a long period. Five years is a reasonable period of time for any pre-existing condition to show up. The onus of proving that there was a fraud rests with the insurer,” says Shilpa Arora, Chief Operating Officer, Insurance Samadhan, a firm that helps policyholders in getting their grievances resolved.

Health insurance policies come with waiting periods for pre-existing diseases – it is the timeframe after which your declared illnesses or health conditions become payable – of up to four years. Now, this maximum waiting period has been shortened to three years.

Even today, several insurance companies offer products with a waiting period of less than three years. “However, it is left to the policyholder to scout for a policy with a shorter waiting period. IRDAI’s regulations will ensure that all policyholders benefit from shorter pre-existing disease waiting period,” says Dr Bhabatosh Mishra, Director, Underwriting, Products and Claims, Niva Bupa Health Insurance.

So far, pre-existing diseases were defined as conditions or ailments for which policyholder had received treatment or diagnosis from a physician up to 48 months prior to policy purchase. Now, this time-frame has come down to 36 months.

Also read: Declare all pre-existing diseases or your health insurer will reject claims

No mention of 'maximum' entry age of 65 yearsUnder the older set of regulations, insurers had to offer regular health covers to those up to the age of 65 years. However, the new structure does not make a mention of this.

Insurers say the new set of regulations will facilitate the launch of customised and innovative policies that are designed with specific age groups or demographic profiles in mind. For example, products for women, students and senior citizens.

On the other hand, it could also mean that some policyholders will have to settle for dedicated policies. “The maximum age at entry was 65 years for regular health insurance policies. Now, this has been opened up. That is, insurers could decide that their regular policies will be available only for those up to the age of, say, 60 years. Others might have to settle for policies targeted at elderly individuals,” says Hari Radhakrishnan, Regional Director, First Policy Insurance Brokers.

Grey areas that need clarityWhile reduction in waiting and moratorium periods are welcome changes, certain aspects have been left unaddressed. “These regulations have replaced the Health Insurance Regulations (2016), which were quite comprehensive. The regulator needs to provide clarity on whether the standardisation of health insurance definitions and rules, which came into effect in 2019, will continue to be applicable. It remains to be seen if the IRDAI issues fresh standardisation norms,” says Radhakrishnan.

In 2019 these regulations introduced the concept of moratorium in health insurance in India and standardised definition and coverage of modern treatment procedures. “The standardisation norms reduced disputes as all insurers had to follow uniform definitions and clauses. In the interest of policyholders IRDAI needs to make it clear that the standardisation regulations will continue to be in force,” says Radhakrishnan.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.