The Securities and Exchange Board of India (Sebi) released a consultation paper on February 2 with the aim of smoothening the process of transmission or passing on of financial assets to surviving family members after an investor’s death.

In this paper, the regulator has proposed to revise the prevalent nomination facilities for demat accounts (shares, bonds, real estate investment trusts, etc) and mutual funds held in statement of account form (not in a demat account).

Some of the proposals reiterate what is already in practice, while others, once finalised, can be useful additions to the existing nomination processes. Comments are invited from industry players and the public until March 8.

Key proposalsSebi has proposed to do away with the requirement of mandatory nomination - choosing a nominee/s or explicitly opting out of nomination - for jointly held demat accounts and MF investments.

This has come about after Sebi repeatedly extended the deadline for completing nominations – most recently to June 30, 2024. Many joint holders have faced problems in completing their nominations, especially via the online route (as highlighted in an earlier article).

For singly held accounts/investments, nominations will continue to remain mandatory.

What is worrisome is that data from the Sebi paper shows that a large percentage of singly held demat accounts and singly held mutual fund folios either don’t have a nominee or have opted out of nomination (see graphic).

“In the absence of a nominee, the transmission process becomes very tedious for the surviving family members. One should never leave an investment without a nominee,” said Renu Maheshwari, a Sebi-registered investment advisor and founder of Finscholarz Wealth Manager.

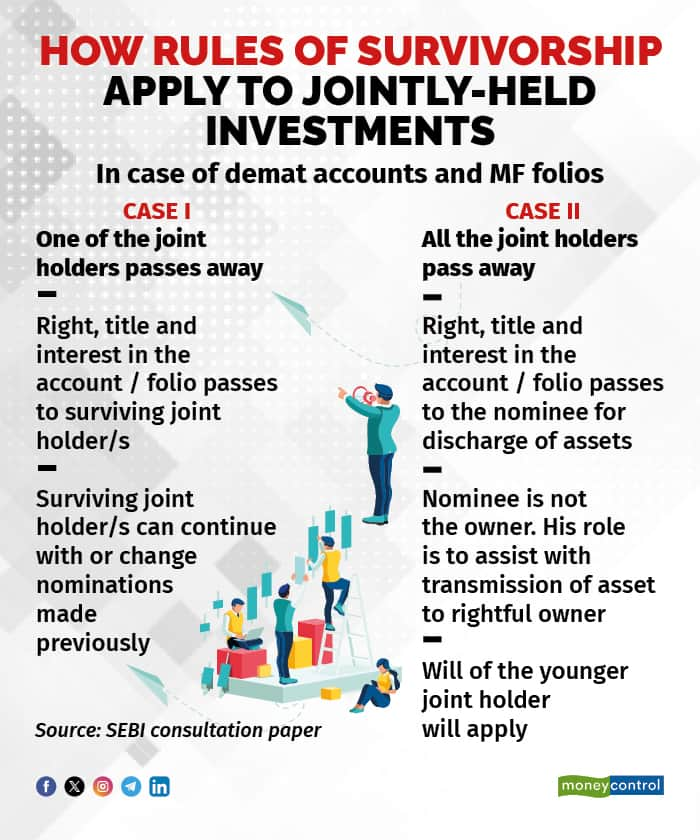

The paper lays out the way forward in the case of death of one or all of the joint holders (see graphic for details).

According to Rajat Dutta, founder of Inheritance Needs Services, a firm that provides inheritance related services, the consultation paper has laid to rest speculation over nominees being declared asset owners.

“Sebi has respected the prevalent two modes of succession, i.e. through will or trust deed and in its absence, the applicability of relevant successions laws. This reinforces that nominees are critical, but only represent heirs or beneficiaries (in case of a will or trust deed). The regulator’s position has been in line with the Supreme Court judgement in the Sakti Yezdani & Anr. v/s Jayanand Jayant Salgaonkar & Others, dated December 2023,” said Dutta.

In short, the nominee does not automatically become the owner after an investor’s demise.

Dutta said this protects vulnerable investors (the elderly with no offspring or with children living overseas) from servants or caregivers who could use the nomination route to swindle their wealth.

Maheshwari found the proposal on giving an investor the option to specify that the nominee/s be allowed to conduct transactions on their behalf in the event they become temporarily or permanently incapacitated very useful. Right now, investors don’t have such an option.

The paper suggests a possible double-digit number of nominees (as an upper limit). Currently, one can specify up to three nominees for a demat account and a mutual fund folio. According to Dutta, the purpose seems unexplainable because more than one nominee would require percentage sharing, etc., which makes transmission complex.

To Amol Joshi, a mutual fund distributor and founder of Plan Rupee Investment Services, the proposal on successive nominee/s is a welcome step. Essentially, in addition to specifying a nominee, an investor will have the option of specifying successive nominees who take over if the chosen nominee passes away while the investor is still around.

Proof of the pudding lies in the eatingJoshi said what’s important is that the process for operationalising the concept of successive nominees should be made digital and investor-friendly for it to really serve its purpose. That seems unlikely at the moment.

He talked about how existing users of Mutual Funds Utility, an MF-industry backed transactions platform, are still unable to update their nominations online. They can do this only through submission of physical forms.

Similarly, when it comes to jointly held folios, MFCentral, an MF transaction platform backed by registrar and transfer agents CAMS and KFintech, does not provide investors the option of updating nominations online.

This is when both these facilities are available to investors on the standalone portals of CAMS and KFintech. But the industry has not been able to provide them on unified platforms such as MFU and MFCentral.

Dutta appreciated Sebi’s pro-activeness in instituting pro-investor regulations, but ground-level practical hurdles faced by investors while dealing with asset management companies and registrar and transfer agents do not seem to be getting addressed.

He cited the example of a demat account in the sole name of an investor with no registered nomination to make his point. On the demise of this account holder, the depository participant (DP) needs a probate of will or, in the absence of a will, a letter of administration (LOA) granted by a competent court to transfer the demat account in the name of the beneficiaries. Probate is the process by which the court certifies the will to be valid. “But when a notarised copy of the will/LOA is submitted to the DP, they insist on a no-objection from all heirs/beneficiaries/claimants. This is a duplication of the court process,” said Dutta.

While the Sebi consultation paper has useful suggestions on easing the transmission of assets to the next of kin, the success of these proposals will depend on how they are implemented.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.