From October 1 retail loan borrowers will have greater clarity on how much their loan actually costs with the help of key facts statement (KFS) to be issued by banks and non-banking financial companies (NBFCs).

This follows the announcement by the Reserve Bank of India (RBI) governor Shaktikanta Das in the February monetary policy review on directing banks to provide borrowers with an annualised percentage rate (total cost of loan). Put simply, APR will comprise not just the rate of interest but also all other loan-related costs.

Now, on April 15, the central bank has issued an instruction on the key facts statement (KFS). This is being done to enhance transparency and empower borrowers to make an informed financial decision, it said.

The instructions will be applicable in cases of all retail and MSME (micro, small and medium enterprises) term loan products offered by all regulated entities.

Let’s look at the nitty-gritty of the KFS and the recent instructions given by the RBI.

What is KFS?

KFS will ensure transparency and help borrowers take informed decisions after ascertaining the total costs they will incur while taking and repaying the loan. It’s a simple, easy-to-understand summary, covering all key terms of the loan, and the fees and charges related to the loan.

It is critical as the KFS cuts through legal terminology in simple language and provides the borrower with all the crucial facts in a concise form.

“KFS is like a skeleton of the loan and a borrower needs to know all the key joints, bending and movements,” says Rajiv Sharma, Partner, Singhania & Co.

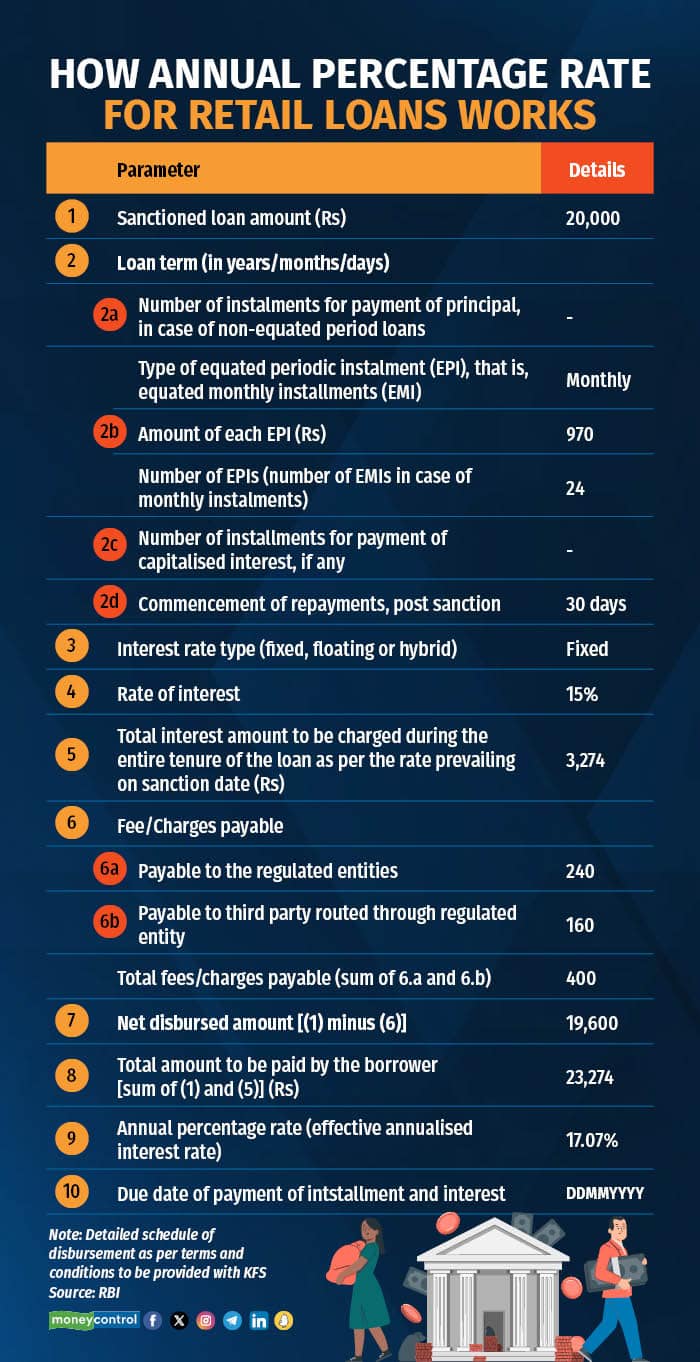

What is annualised percentage rate (APR)?

Annualised percentage rate is the annual cost of credit to the borrower, which includes the interest rate and all other charges associated with the credit facility. Other charges include insurance charges, legal charges, any additional fees, and more.

The KFS will also have to provide a computation sheet of the APR, and the amortisation schedule of the loan over the repayment period.

loans works" width="700" height="1362" />

loans works" width="700" height="1362" />

In all cases wherever the lender is involved in recovering such charges, the receipts and related documents will have to be provided to the borrower for each payment. Any fees or charges which are not mentioned in the KFS cannot be charged by the regulated entity to the borrower at any stage during the term of the loan without the explicit consent of the borrower.

What is the equated periodic instalment (EPI) mentioned in the key facts statement?

It is an equated, or fixed, amount of repayments consisting of both the principal and interest components, to be paid by a borrower towards repayment of a loan at periodic intervals for a fixed number of such intervals; and which results in complete amortisation of the loan. EPIs at monthly intervals are called EMIs (equated monthly instalments). Given that retail loans typically involve repayment in monthly instalments, for individual borrowers, EPI simply means EMI.

How to locate your KFS?

Lenders are mandated to provide all borrowers with a clear, concise KFS at every stage of the loan processing as well as in the case of any change in terms and conditions.

Regulated entities shall provide a KFS to all prospective borrowers to help them take an informed view before executing the loan contract, as per the standardised format given on the RBI website.

“Banks/NBFCs are supposed to share a copy of KFS, along with other key loan documents, to the borrower over email or SMS and so on,” says Parijat Garg, a digital lending consultant.

“In the case of digital lending, a prospective borrower can find KFS under the loan details screen which can be easily read and downloaded,” adds Sharma.

The KFS shall be written in a language understood by the borrowers, the RBI directive says. Banks have to explain the contents of KFS to the borrower and obtain an acknowledgement to prove that she has understood the same.

Also read: RBI Monetary Policy | RBI holds repo rate at 6.5%: No impact on home loan EMIs

Will borrowers be granted a validity period to convey their acceptance after being provided with the KFS by the lender?

Yes, the borrower will have a validity period of at least three working days for loans having a tenor of seven days or more, and a validity period of one working day for loans having a tenor of less than seven days to agree to the terms of the loan agreement as mentioned in the KFS. The regulated entity will be bound by the terms of the loan indicated in the KFS if agreed to by the borrower during the validity period.

What are the benefits for borrowers?

KFS provides a standardised document with a prescribed approach to calculate APR. So, the KFS makes it easier for the borrower to compare offers from different lenders, irrespective of the loan tenure and types of charges involved.

If you do not receive the KFS or spot a discrepancy in the KFS, you can raise it with the lending company. “The first opportunity of grievance redressal is the lender’s internal ombudsman, who must settle such grievance within 30 days of receipt of the complaint,” says Sharma. If the grievance is not redressed to the satisfaction of the borrower, another grievance can be registered with the RBI’s Banking Ombudsman.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.