It’s that time of the year when you need to get cracking on filing your income tax (IT) returns. As the July 31 deadline draws near, it is time to take stock of some key tax deductions and exemptions that senior citizens (60 or above) can claim at the time of filing their returns. These are in addition to what every taxpayer, whether a senior citizen or not, is allowed.

Unlike the salaried who claim tax deductions against their salary at the time of submitting their proof of investment to their employers in January and February, senior citizens (not in employment) have to claim the deductions against their advance tax liability, if applicable, or self-assessment tax, at the time of filing their returns.

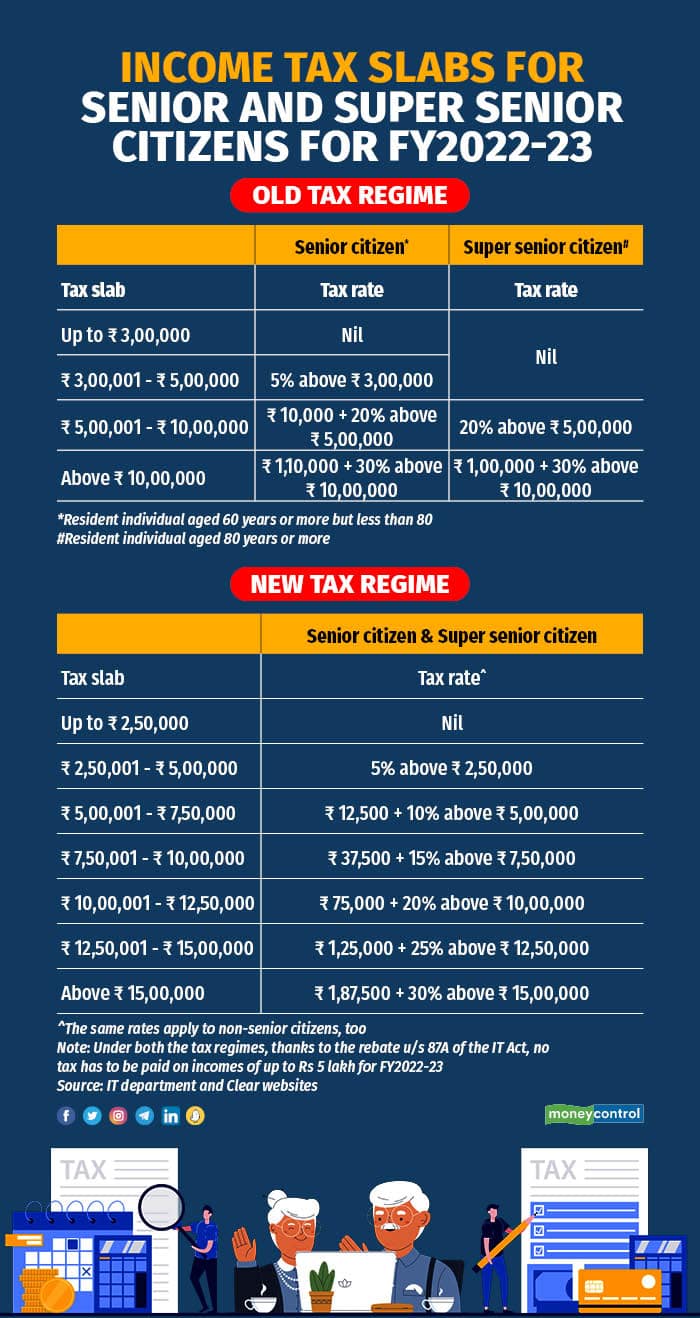

Also, depending on whether you are a resident senior citizen (aged 60 or more but less than 80), or a super-senior citizen (aged 80 or more), and the tax regime (old or new) that you choose, your slab rates will be different (see graphic).

If you opt for the old tax regime, you will be eligible for several exemptions and deductions (see graphic). But if you pick the new concessional tax regime, not all of these will apply. Furthermore, under certain situations, you may also be exempt from the requirement of filing tax returns.

Higher basic exemption, filing returns

Under the old tax regime, senior and super-senior citizens residing in India have been allowed a basic exemption limit of Rs 3 lakh and Rs 5 lakh, respectively, for the financial year 2023 (April 1, 2022 to March 31, 2023). That is, they do not have to pay any income tax on taxable income up to these amounts. For non-senior citizen taxpayers, the exemption limit is Rs 2.5 lakh.

However, under the new tax regime, all resident individual taxpayers, whether 60 and above or not, have a basic exemption limit of Rs 2.5 lakh for FY22-23 (see table for more details). If their income is under the basic exemption limit, they need not file their returns.

“Up till FY2022-23, the old tax regime was the default regime. So, super-senior citizens opting for this were not required to file returns if their total income was up to Rs 5 lakh in a financial year,” says, Mayank Mohanka, Partner, S M Mohanka & Associates.

Talking of FY23-24 and beyond, he says, “From FY23-24, the new tax regime has been made the default regime, so all taxpayers, including those aged 60 or above, are not required to file their returns if their total annual income is up to Rs 3 lakh.”

Apart from this, those 75 years or older, and who meet the conditions specified under section 194P of the IT Act, are exempt from filing returns. Among the conditions that a senior citizen must fulfil is that he must have been an Indian resident in the financial year for which the return is being filed. He must have only pension and interest income, and the interest income must have been earned from the same bank in which the pension is being received.

For this purpose, the bank must be a ‘specified bank’ as notified by the central government. A senior citizen has to submit a declaration (to the effect that he has no other income) to the specified bank, which will then deduct TDS after taking into account deductions under chapter VI-A (deductions under sections 80C to 80U), and the rebate under section 87A.

Asked if many senior citizens qualify under this section, Mohanka says, “The requirement to fulfil all the above specified conditions restricts the benefit of non-filing of returns to a very limited section of senior citizens.”

Exemption from advance tax

Under the old regime, per section 207 of the IT Act, a resident senior citizen (60 or above) does not have to pay any advance tax provided he / she does not have any business or professional income. Parizad Sirwalla, Partner and Head, Global Mobility Services, Tax, KPMG India, points out that this exemption is also available under the new tax regime.

Deduction for interest income

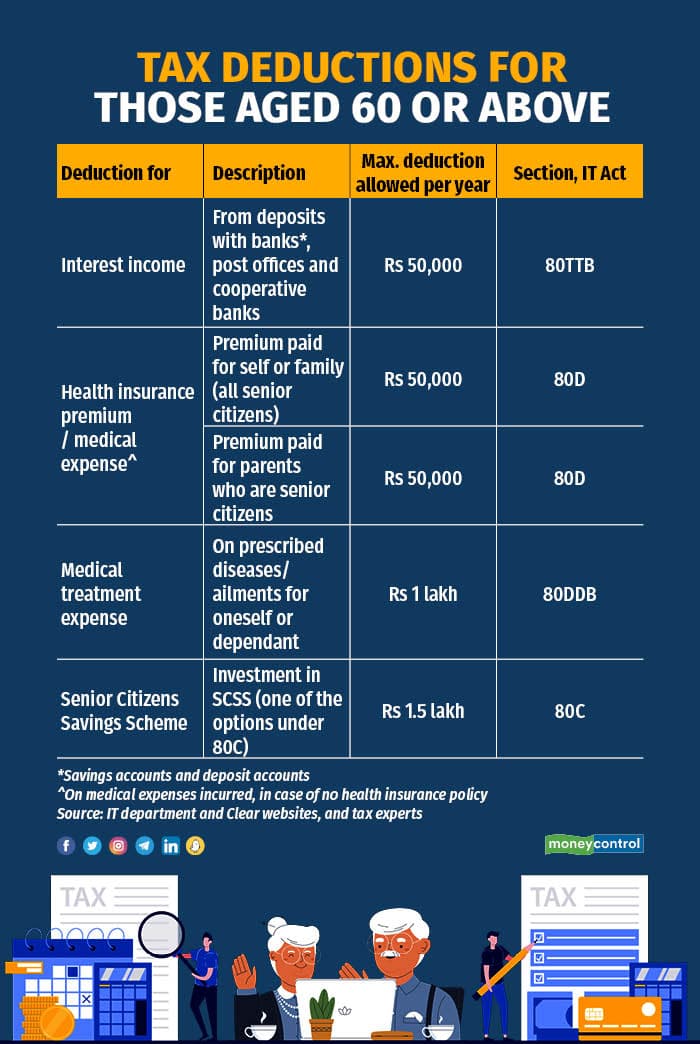

Under section 80TTB of the IT Act, a resident senior citizen (60 or above) can claim a deduction of up to Rs 50,000 for interest income earned in a financial year. This applies to interest income from bank savings and fixed deposit accounts, as well as from deposits with post offices and cooperative banks. This deduction is not available under the new tax regime.

Furthermore, under section 194A, no TDS gets deducted on interest payments of up to Rs 50,000 per financial year to resident senior citizens. “This limit is to be computed for every bank / payor individually for all deposits with them. The TDS deduction is not impacted by the choice of tax regime by the payee,” says Sirwalla.

If your income does not exceed the basic exemption limit and you have been unable to submit Form 15H that facilitates a TDS waiver, your bank would have withheld 10 percent of the interest earned. In such cases, you can claim a refund for the excess tax deducted while filing your returns.

Deduction for health insurance premium

Under section 80D, a resident senior citizen (60 or above) can claim a deduction of up to Rs 50,000 per financial year for health insurance premium paid for himself or family (all senior citizens). Here, family means spouse and dependent children.

If no health insurance policy has been taken, then a senior citizen can claim deductions for medical expenses up to Rs 50,000 per financial year for himself or family.

Not only that, according to Sirwalla, a senior citizen is also allowed an additional deduction of up to Rs 50,000 per financial year for premium paid (or for medical expenditure incurred where no insurance is taken) for parents who are senior citizens.

In either case, the deduction can be claimed only if the payment has been made in a mode other than cash. This deduction is not available under the new tax regime.

Deduction for specific medical expenses

Under section 80DDB, a resident senior citizen (60 or above) can claim deduction for expenditure incurred on medical treatment of prescribed diseases / ailments either for himself or for a dependent. Under this section, a senior citizen can claim a maximum deduction of up to Rs 1 lakh per year. Those under 60 can claim a maximum deduction of Rs 40,000.

Sirwalla highlights that this deduction is available net of the amount received from an insurer and / or reimbursed by an employer for such medical treatment. This deduction is not available under the new tax regime.

The benefit of the deductions under sections 80D and 80DDB is available not only to those aged 60 or above but even to other taxpayers. However, for the latter, the extent of deduction allowed is lower.

Providing more clarity on claiming deductions under these sections, Mohanka says, “The deduction can be claimed only by the person who has paid for the health insurance premium or incurred the medical expense. So, if a senior citizen wants to claim this deduction, then this payment / expenditure must be met from his / her bank account only.”

Deduction for Senior Citizens Savings Scheme

Under section 80C, senior citizens are allowed deductions for investments made in the Senior Citizens Savings Scheme (SCSS), as part of the overall limit of Rs 1.5 lakh per year. This deduction is not available under the new tax regime.

So, if you are a senior citizen getting ready to file your IT returns, do remember to claim these deductions, wherever applicable. Make sure you have appropriate documentary proof to support your claims.

Also read: Financial year just got over. Where do I throw these tax documents now?

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.