Towards mid-March, some investors figure out that they are yet to complete their tax-saving investments. And the search makes them look for some quick fixes. If you too are looking for some tax-saving investment at this juncture, you may want to consider equity-linked savings schemes (ELSS) popularly known as tax-saving schemes.

What is an ELSS?Tax-savings schemes are equity schemes of mutual funds that invest at least 80 percent of the money in stocks. In most cases, they are fully invested in a diversified portfolio of stocks. Units of these schemes held by investors are subject to lock-in of three years from the date of allotment. Investment up to Rs 1.5 lakh in a financial year can be claimed as deduction by an individual under Section 80C.

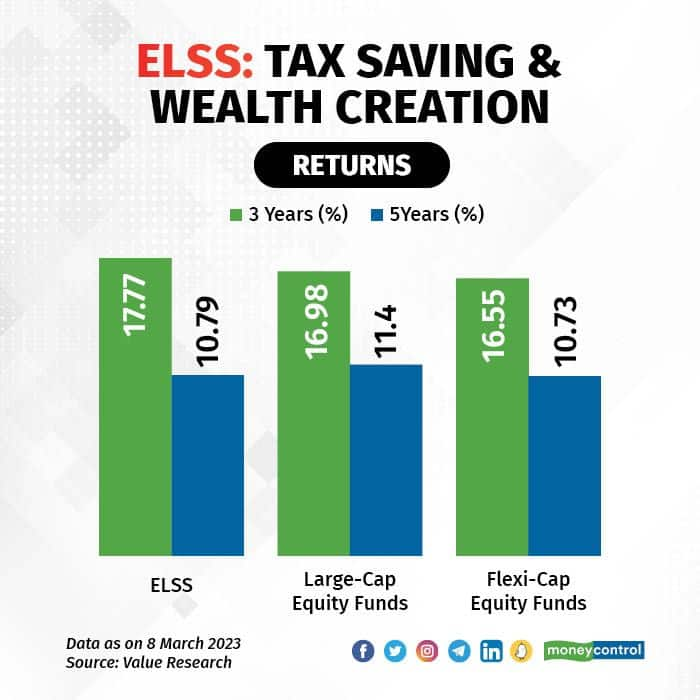

Over the last three and five years ended March 8, 2023, these schemes on average have given 17.77 percent and 10.79 percent return, respectively, as per Value Research. In the past, over a longer period of time, ELSS has beaten other tax-saving investments by a decent margin.

Despite volatility on Dalal Street over the last one year, experts are optimistic on equities, going forward.

Alok Ranjan, Chief Investment Officer at IDBI Mutual Fund, says, “When the developed economies are struggling with a fear of recession, the Indian economy has demonstrated remarkable resilience. Strong economic growth backed by various government policies such as production-linked incentives; rising expenditure on infrastructure; overall fiscal prudence and a revival in capex cycle augur well for corporate earnings growth in the medium term. An investment in ELSS can help investors benefit from it and save taxes too.”

Though it looks good to invest and complete the tax-saving ritual for the year, you should also understand a few more aspects here.

Which ELSS?There are 38 ELSS in the mutual fund industry and you are left with the arduous task of choosing one that suits your needs. Barring two, ELSS are actively managed schemes.

They in most cases run a flexi-cap portfolio. It means the fund manager has the flexibility to choose stocks across market capitalisation based on relative attractiveness. On average, 72 percent of money was invested in large-cap stocks, as on February 28, 2023. There can, of course, be some actively managed schemes that have higher exposure to mid- and small-cap stocks. Put simply, these investments can be unnerving in volatile times and, hence, you have to select one with a good track record. You may also refer to MC30, a curated basket of mutual fund schemes.

Mohit Gang, co-founder and CEO of Moneyfront, an online distributor of mutual funds, says, “Over the long term, actively managed ELSS have done better than any other tax-saving avenue. To build wealth using ELSS, one has to have a long-term view on equities and should hold on to the investments for five to seven years ignoring intermittent volatility.”

However, investors looking for exposure to large-cap stocks in their ELSS should opt for passively managed ELSS funds, he adds.

The Securities and Exchange Board of India (SEBI), the financial market regulator, last year allowed mutual fund houses to offer passively managed ELSS, with a caveat. Only those fund houses are allowed to launch a passively managed ELSS that does not have an existing ELSS. For those with an existing actively managed ELSS, it allowed for the launch of a passively managed one if the fund house chooses not to accept fresh investments in the actively managed scheme.

IIFL ELSS Nifty 50 Tax Saver Index Fund and Navi ELSS Tax Saver Nifty 50 Index Fund are two passively managed schemes available for now. As the name suggests, these track the Nifty 50 index.

Tips to make the best out of your ELSS investmentHow much room do you got in Section 80 limit?Under Section 80C, you can invest up to a maximum of Rs 1.5 lakh. You can invest more, but your income-tax deduction benefits will be available only till Rs 1.5 lakh.

Check your existing contributions to the employees' provident fund, life insurance premium, National Saving Certificate, tuition fees, public provident fund (PPF) and other eligible investments. If you still fall short of the Rs 1.5 lakh mark, then you should invest the balance amount in ELSS.

How many ELSS do you need?Do not go overboard. Roshni Nayak, a SEBI-registered investment advisor and founder of Goalbridge, is of the opinion that having only one ELSS in a portfolio is good enough. “Most ELSS funds invest an average 60-70 per cent in large-caps and the balance small portion is in mid- and small-caps. Investors tend to invest in multiple ELSS funds to save tax every year. This leads to duplication in the portfolio,” she says.

Should you withdraw after three years?Not necessarily.

Though you can redeem your investment in ELSS after three years, there is no compulsion. You can allow your money to compound. However, in times of a cash crunch, units that have completed three years of lock-in can be sold and reinvested in ELSS to achieve tax benefits for that year.

When you sell units of ELSS, you book long-term capital gains, which are taxed at the rate of 10 percent if they exceed Rs 1 lakh in a year.

SIPs invest slowly…but redeem slowly too.Since ELSS feed into stocks which is a volatile asset class, there is a need to stagger your investment. As we are closer to the financial year-end, there is little scope to do so. But you may have a lesson here—start your tax-saving investments early in April and stagger them through the year to benefit from rupee cost averaging. SIP is a series of fixed amounts of investments in mutual fund schemes at regular intervals.

Remember—each SIP purchase is subject to lock-in and each unit must be held for three years.

Extant rules prescribe that allotment of units happens only when your money reaches the mutual fund house. So do not wait till the last day. If you cut the cheque on March 31, the money will be realised by the fund house in April and the units get allotted in the next financial year.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.