Last week, the Finance Minister announced that employers will be allowed to contribute 10 per cent – instead of the mandatory 12 per cent – of your basic pay as their contribution to the provident fund.

This reduction in the statutory employees’ provident fund (EPF) would be applicable for the months of May, June and July 2020.

Likewise, your contribution will also come down by two percentage points. While your take-home pay will increase correspondingly, this move, along with the reduction in employers’ contribution, means that your retirement corpus will take a minor hit.

If you need the money now because of a cash crunch, then this move helps. But for those who don’t really the funds now, this measure isn’t a big plus. But there’s a way to compensate for the reduction in your EPF corpus and ensure your long-term savings don’t get impacted. Enter the voluntary provident fund (VPF). If you have already started your VPF, you can ask your employer to increase your contribution to make up for the reduction in both employer and employee contributions.

What is VPF?

Let’s look at the basics first. Employers deduct 12 per cent of their staff members’ basic wages as employees’ contribution to the EPF every month. They contribute an equivalent amount to the employee’s account as employer’s contribution. Out of the employer’s contribution, 8.33 per cent goes towards the employee’s pension scheme (EPS). The monthly contributions, along with interest accumulated over the years, make up your retirement corpus.

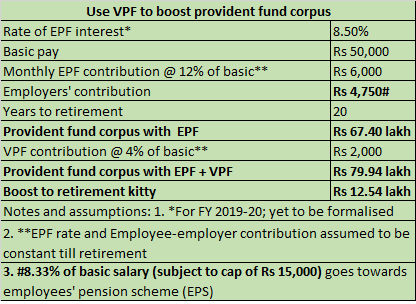

But, if you want to bump up your retirement corpus, you can choose to contribute an additional amount, over and above the mandatory 12 per cent, every month. Let’s assume your basic salary is Rs 50,000 and your EPF contribution works out to Rs 6000 a month (12 per cent). For someone who is to retire after 20 years, VPF monthly contribution of four per cent of basic pay can push up the retirement corpus by Rs 12.54 lakh, assuming an interest rate of 8.5 per cent a year for the entire period. VPF, like EPF, can be transferred when you switch jobs.

How do I enrol?

Decide how much extra you can afford to set aside every month. You can even contribute up to 100 per cent of your basic pay, if you can afford to, but that’s not practical. Many employers offer an online facility to activate VPF, allowing you to earmark a fixed sum or percentage of your basic pay for this additional contribution every month. Since it is voluntary in nature, unlike the statutory 12 per cent contribution, you can reduce or increase your contribution on a monthly basis, before the cut-off date specified by your human resources team. However, ensure that you make adequate enquiries before you start contributing as flexibilities could vary as per employers’ policies.

Does it offer tax benefits too?

Yes. VPF contributions are eligible for tax deductions under section 80C, subject to the overall Rs 1.5 lakh limit, just like EPF contributions. Moreover, these investments, too, will get the EEE status like EPF – exempt from tax at the investment, accumulation and maturity stages. So, if your EPF contributions are not adequate for exhausting the 80C limit, starting the VPF will double up as your tax-saver too.

Can I dip into the corpus in times of need?

Since your VPF contribution lands up in your EPF corpus, the rules for premature withdrawal for certain specified causes such as house purchase, marriage, education and critical illnesses remain the same. You can make partial, premature withdrawals after at least five years of service, depending on the purpose. If you have been unemployed for more than a month, you can withdraw up to 75 per cent of the corpus. This apart, to tide over any COVID-19-induced financial crunch, you can make use of the one-time withdrawal facility announced by the government in March. You can take an advance of up to 75 per cent of your EPF account balance or three months’ basic wages or the amount that you actually need, whichever is lower .

Should you opt for VPF?

Surely, yes, provided you have the required surplus. It is a highly secure, tax-efficient avenue that offers better return than most debt instruments. Moreover, you need not to go through complicated KYC procedures or paperwork for opening an account to start investing, as you can start contributing through your employer. Since the amount you earmark as VPF will be deducted from your salary every month, your tax as well as retirement planning is taken care of with minimal hassles.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.

")