The introduction of direct plans has been one of the bigger regulatory changes in Rs 57-trillion Indian mutual fund industry in the 15-odd years gone by. All asset management companies (AMCs) launched direct mutual fund plans for all their open-ended schemes from January 1, 2013, as directed by markets regulator Securities and Exchange Board of India (Sebi).

About 45 percent of the Industry AUM has been routed through the direct plans, industry data shows. Here we explain how the direct plans delivered returns compared to their regular counterparts, expense ratios and adding a note of caution for novice investors who are willing to opt for it without proper guidance.

Direct vs RegularIn India, mutual fund schemes have traditionally been sold through distributors and financial advisors. AMCs pay commission for the service rendered by the intermediaries that are deducted as expenses from the schemes’ NAV which in turn reduces the return made by investors in the scheme.

Since the direct plans were introduced, investors get an opportunity to buy schemes directly from mutual fund companies at lower costs. Under direct plans, the commission paid to intermediaries and the distribution expenses are excluded from the expenses charged to investors, thus causing a difference in the expense ratios. This results in direct plans earning higher returns than regular plans.

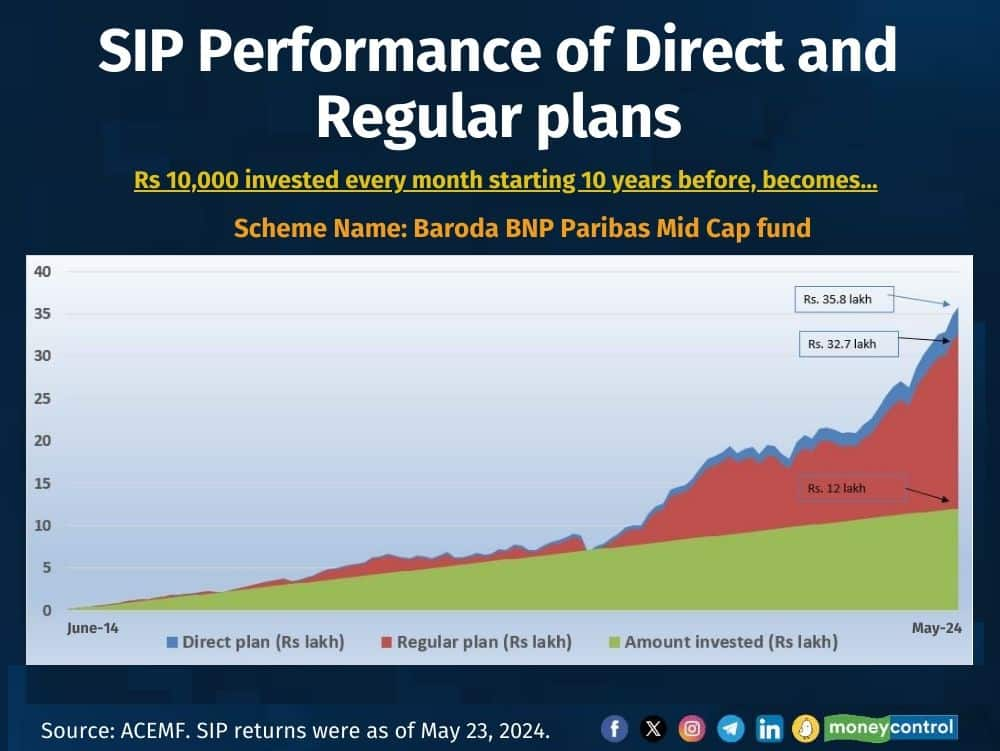

For instance, a SIP of Rs 10,000 made on a monthly basis in the direct plan of Baroda BNP Paribas Mid Cap fund that started 10 years ago has now grown to Rs 35.8 lakh. On the other hand, identical SIPs during the same period in the regular plan of the same fund has accumulated Rs 32.7 lakh. The direct plan has generated about 1.8 percentage point higher annualised returns, or Rs 3.1 lakh more, than the regular plan.

Also see: Explained: How direct plans carved a niche in the Indian mutual fund industry

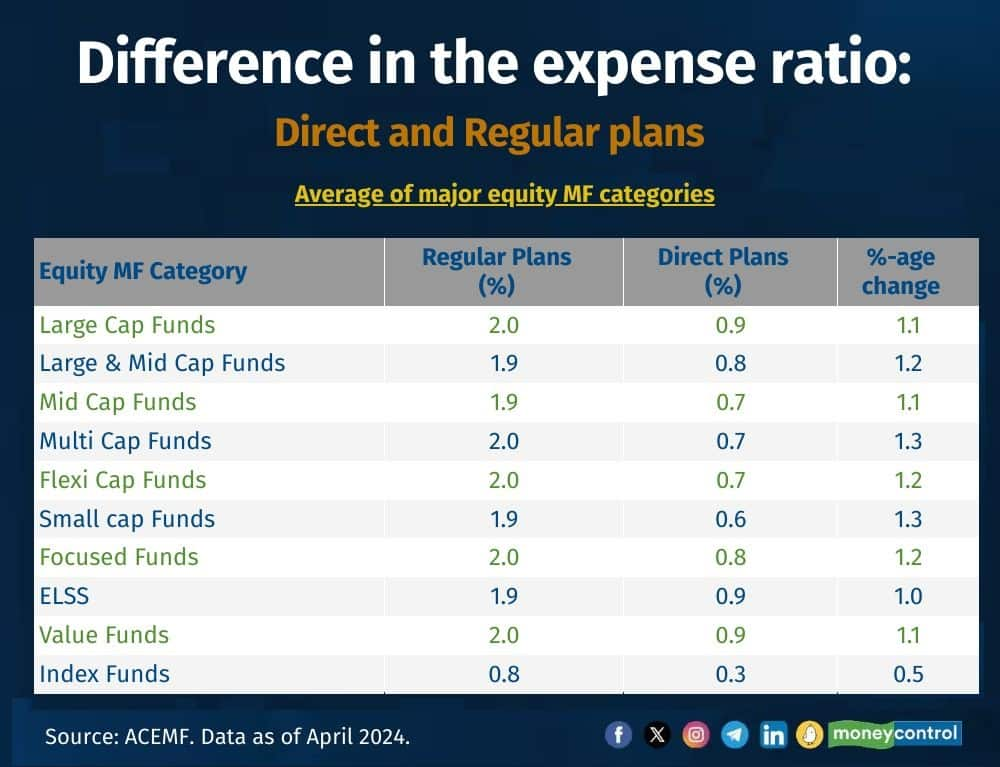

What makes the difference in the expense ratio?Total expense ratio (TER) is the fee charged by the AMCs to manage the investors’ money. The expenses, including investment management and advisory fee, trustee fee, marketing and selling expenses, and distributor commissions, are calculated against the daily average net assets of the fund. The NAV of each day is calculated after accounting for such expenses and hence, borne by the investor.

Direct Plans have a lower expense ratio as they exclude distribution expenses, commission, etc.

As per the ACEMF data, the difference in the expense ratio of direct plans and regular plans of all equity-oriented schemes as of April 2024 was in the range of 30 bps to 190 bps. A 100 basis point is equal to 1 percent. Eventually, the difference is what the direct investors tend to get extra in return.

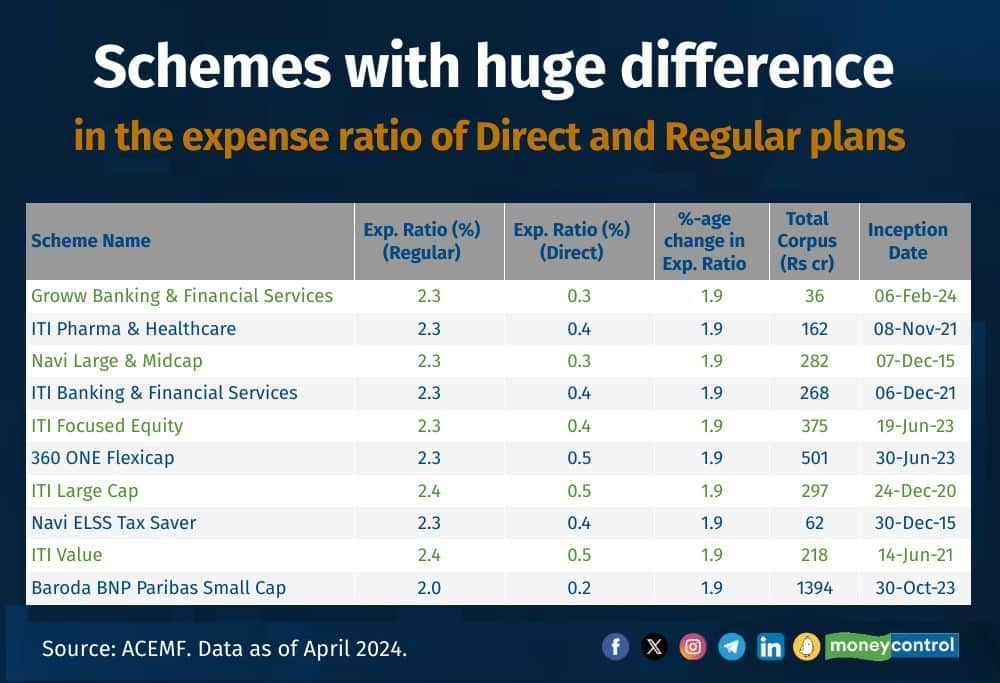

It is observed that mainly the schemes either with lower corpus or newly launched or change in management have a significant difference in the expense ratio between direct and regular plans. Needless to say, established schemes with larger assets do not require a harder nudge, or advertising if you may, to attract investors, given their long-term track record.

Also see: Mid-cap and Small-cap Funds: How can retail investors get the best out of them?

Why experts’ advice is still important?Only savvy investors who can cherry pick mutual funds on their own can opt for direct plans. Do-it-yourself (DIY) investors who are new to equity markets may end up choosing an unsuitable scheme if they pick schemes just by look at the difference in the expense ratio between direct and regular plans.

“Direct plans are especially suitable for investors who are either savvy enough to manage own mutual fund portfolios or those who are availing advisory services from a qualified advisor. At the same time, it is imperative that the investor does not require operational services typically rendered by a commission-earning distributor,” Nirav Karkera, head of Research at Fisdom, said.

But if you do not have the wherewithal of selecting funds or you can’t decipher markets, it’s best to go to an advisor. Even Sebi-registered investment advisors offer direct plans, but they charge an advisory fee on the overall portfolio. That is also a good option. Else, if you have a good distributor who handholds you, it’s best to stick to them instead of venturing out on your own.

Remember though that the expense ratio should not be your only criteria for choosing a mutual fund. A sound track record of consistent returns is critical to achieving your long-term financial goal.

Also see: Retail investors drive MF growth, here's how they played the game

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.