CRED, a fintech firm, has launched CRED Mint, a peer-to-peer (P2P) lending platform. It allows eligible CRED members to lend money and earn interest rates of up to 9 percent a year. Though not comparable, this is higher compared to interest rates offered by bank fixed deposits (FDs). Should you invest or lend via this platform?

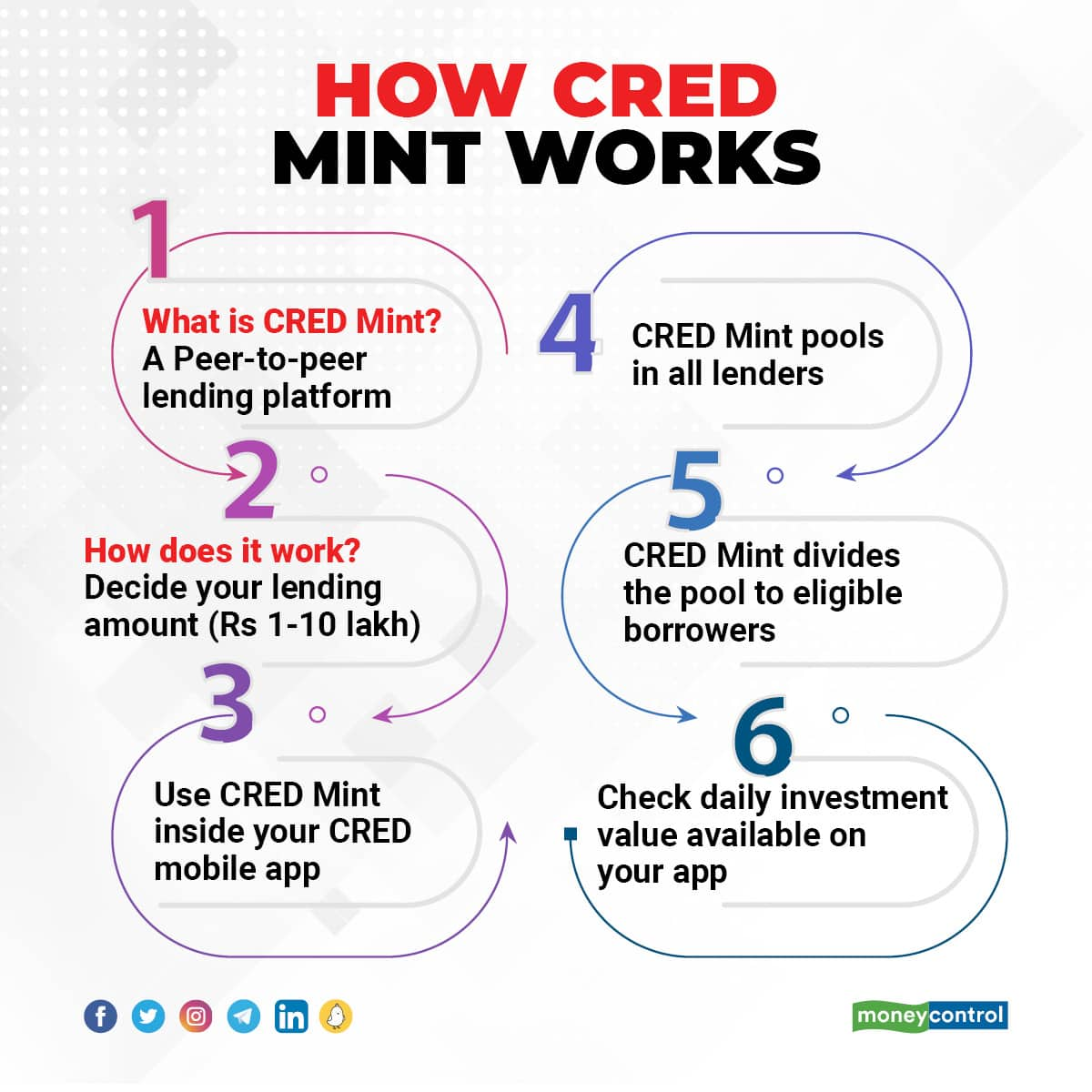

What is CRED Mint?CRED Mint has been rolled out in partnership with Liquiloans, a RBI-registered P2P non-banking finance company. It is a community-driven product that enables CRED members to earn up to 9 percent interest per annum on idle money by lending to other CRED members with a credit score above 730. It’s important to note that the return rate is not a guaranteed or fixed like in the case of bank FDs. A P2P platform is an online space where borrowers (typically with lower credit scores or those with little or no credit history) can avail loans from individuals willing to lend.

For investors (lenders), higher returns come with more risk. For instance, ICICI Bank offers 4.4 percent interest on one-year fixed deposits. While investing (lending) on CRED Mint, the interest rate could be higher by at least 3 to 4 percentage points.

For borrowers, this would be similar to personal loans of banks, except that the interest rates are lower. For example, ICICI Bank charges 10.5-19 percent, plus a processing fee of up to 2.5 percent of the loan amount. “One could expect P2P borrowing rates to be lower by at least 2-3 percent than such rates,” says Srikanth Meenakshi, Co-founder of PrimeInvestor.in.

How is it different from other P2P platforms?Typically, P2P platforms have one product that brings together borrowers and lenders. The borrower puts in a request in the app and the lender puts the money on the table. CRED works a bit differently.

CRED Mint focuses on the lending side of this transaction, or what it calls, ‘investment’. So, CRED members can lend – or invest – Rs 1-10 lakh on CRED Mint. Lenders can check the value of their investments daily on the app. Recoveries or repayments of loans taken, as and when they happen, get added to the pool and divided among the corpuses of lenders.

Investors can request borrower details and CRED will provide this information. A CRED spokesperson says, "The money invested through CRED is held in an escrow account with a Bank promoted trustee and is then lent out to the borrowers based on the auto-invest criteria chosen by the lender. The lender can choose to see his portfolio of borrowers and other related information by placing a real-time request to CRED."

What worksThe on-boarding process is quick and easy. The guide map is exhaustive enough to answer all your queries.

Parijat Garg, a digital lending consultant, says, “The statistics such as number of people invested a day before on CRED Mint, average amount invested, and credit score profile of borrowers give confidence to new investors. So, investors get higher returns compared to bank FDs with a marginal risk in CRED Mint.”

CRED would split every investment over 200 borrowers with a credit score above 730. “High credit quality borrowers and diversification across such a high number of borrowers are good. Both mitigate risks for an investor,” says Meenakshi.

Further, there is no lock-in period. An investor can take his/her money back any time after investing. So, there are no pre-mature withdrawal charges, unlike bank FDs.

The ‘value’ of an investment is displayed on the app, and an investor can request withdrawal through the app.

Also read: Lending on P2P platforms: A risky proposition; not an investment

What doesn’tThe biggest downside of P2P lending is the default risk. There is no security to recover loss by default. A CRED spokesperson says “Each lender is lending to 200-plus borrowers, creating a well-diversified and fragmented portfolio. By diversifying across 200-plus borrowers, we minimize exposure to bad borrowers. Only borrowers with higher credit scores, low net default rates, solid credit history and track record of on-time repayments qualify for this product.”

On the point of the unsecured nature of the credit, the spokesperson says, “Diversification across more than 200 borrowers minimizes default risk and the loss on an investor’s portfolio closer to historical average of ~1 percent. Even when losses cross this threshold, the variable fee model - which allows the product to withstand up to 4x of historical defaults - ensures that the investor repayments happen are the first priority and their indicated return rate of 9 person is met first. CRED and Liquiloans (RBI regulated NBFC powering CRED Mint) commission will depend on the portfolio performance. To further minimize the risk of loss, Liquiloans and CRED systems are designed to flag unprecedented default on the portfolio well before it happens.”

The returns from an investment on CRED Mint are taxable as per the slab rate of the investor. “A non-guaranteed returns product with zero tax benefit is not a very attractive proposition,” says Meenakshi, who adds that a debt fund offers similar liquidity with lesser risk.

CRED Mint appears to be a product where returns are moderately high, but risk is higher and taxation is unfriendly. “For the inherent risks entailed in P2P lending, the return rate looks modest,” says Meenakshi. “As a lender, the return offered on CRED Mint could be expected to be higher in future as there is a similar P2P scheme from BharatPe offering up to 12 percent returns, of course, with very different risk profile,” says Garg.

Should you invest?A high minimum investment requirement and no guarantee on returns make CRED Mint an unattractive proposition for many. Besides, P2P platforms are prone to defaults by borrowers. Investment in bank FDs gives guaranteed returns and deposits up to Rs 5 lakh are insured, under Deposit Insurance and Credit Guarantee Corporation (DICGC) scheme of the Reserve Bank of India (RBI).

Mrin Agarwal, Financial Educator, Money Mentor and Founder of Finsafe India suggests traditional investments such as index funds or stocks. “With P2P lending, no information of borrowers is available to the lenders,” she adds.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.