There are banks, NBFCs and online lenders who promote easy and quick loans on flat interest rates. These flat interest rates have been used as a marketing tool by lenders for enticing a customer by quoting low-interest rates and mislead them into taking a high-cost loan. With such interest loans borrowers fall into a debt trap.

Satyam Kumar, Co-founder, CEO, LoanTap said, “Under flat interest rates customers generally end up paying 1.7 to 1.9 times higher than the reducing balance interest rates effectively.”

Click to access Moneycontrol's EMI calculator

This fact is not known to customers in general, who perceive that they are availing a lower interest rate while they are doing just the opposite.

Let us understand flat interest rates and reducing balance interest rate methods and its impact on borrowers.

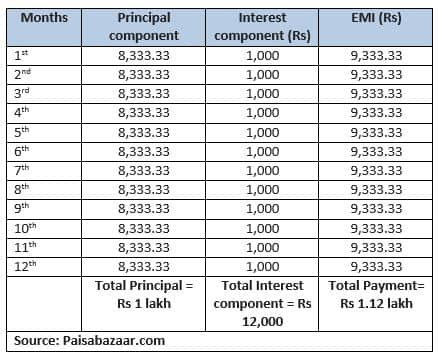

Flat interest rate method

Under this method, lenders calculate interest on the original principal amount throughout the loan tenure. Thus, both the interest and principal component in EMI remains the same throughout the tenure.

Illustration: Flat interest rate EMI table for Rs 1 lakh loan, tenure 1 year at 12% per annum.

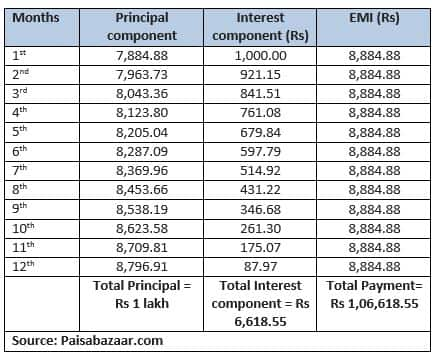

Reducing interest rate method

Under the reducing interest method, the outstanding principal amount is reduced by the amount of principal repaid and the interest for the next month is calculated on the reduced outstanding principal amount. Thus, the interest component of EMIs keeps on decreasing with the repayments of EMIs.

Illustration: Reducing interest rate EMI table for Rs 1 lakh loan, tenure 1 year at 12% per annum.

From the above illustration: Which loans are better? Reducing interest rate or flat interest rate?

Naveen Kukreja, CEO and Co-founder of Paisabazaar.com said, “Reducing interest rate method is better from the customer’s perspective as the interest cost in the loan availed in the reducing balance method is significantly lower than the loans availed at a flat rate.”

For instance, if you compare two loans availed in above illustration the interest cost in case of the reducing interest rate method would be around 44% lower than the flat interest rate method.

Gaurav Gupta, Co-founder and CEO, MyLoanCare.in added, “From the perspective of being transparent, reducing rates are always better as they reflect the accurate rate and interest to the borrower. Flat rates can be highly misleading especially if quoted on EMI loans that are the most popular loans nowadays.”

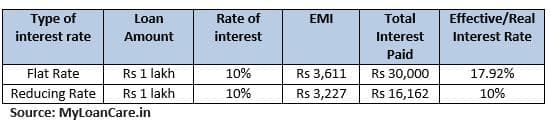

Illustration: If a loan of Rs 1 lakh was taken for a period of 3 years at a flat rate of 10%, repayable in monthly installments, you pay an EMI of Rs 3611 and your effective interest rate calculated is 17.92%. In this situation, the borrower is easily fooled by taking a high cost loan, wrongly believing it to be a 10% loan.

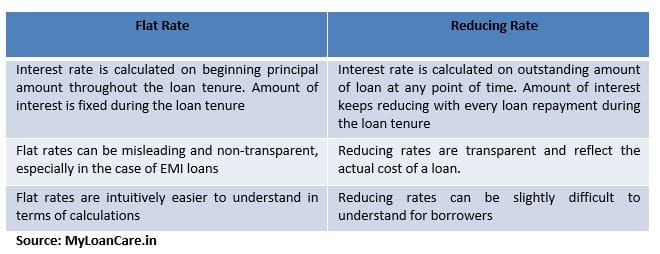

Key differences between the flat rate method and reducing balance method

Drawbacks of the flat interest rate method

There are indeed some major drawbacks as far as the flat interest rate method is concerned. Amit Prakash Singh, Principal Partner-Mortgages, Square Yards said, “The cost of the loan is much higher than a reducing interest rate loan, interest on the entire loan amount and the outstanding loan amount does not go down.”

Lastly, borrowers do not get the benefits of a reduction in interest rates based on market conditions and have to keep paying the same EMI throughout the tenure.

Word of caution

Kunal Varma, Chief Business Officer & Co-founder, MoneyTap said, “A flat interest rate is a gimmick by lenders to lure customers into taking a loan without actually allowing them to understand what the entire scheme is all about.” Consumers who are usually in urgent need of money fall for it and end up paying higher amounts as interest. It’s a trap indeed!

What borrowers should do?

Always ask the lender about the interest rate calculation method before taking a final decision to borrow. Singh added, “You can also spend a little time in the calculation of the total interest payable by multiplying their EMIs by the number of monthly installments and then deducting the principal amount from this sum. This will help compare loan offerings based on rates of interest and calculation methods.”

Also, always take into account upfront costs like processing fees when you are comparing loans from lenders.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.