Highlights:

- Protection and annuity segments get top billing

- Diversified product mix and improving distribution channels a big positive

- Healthy return ratios add to the momentum

-Rich valuations justified, given the superior franchise; buy for the long term

-------------------------------------------------

HDFC Life, a leading private insurer, posted strong earnings for 2018-19 on the back of healthy growth in premium and margin improvement.

Return ratios continues to be good. Despite the premium valuation, tailwinds for the sector and HDFC Life’s vantage position make it a stock worth looking at.

Healthy premium growth with balanced product mix

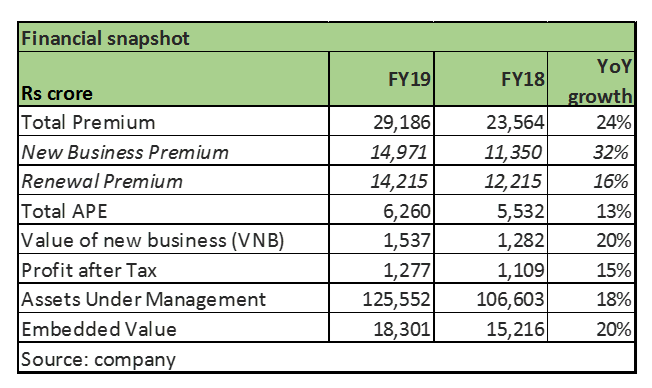

HDFC Life reported a 24 percent year-on-year (YoY) growth in total premium as new business premium grew 32 percent, outpacing the modest growth (16 percent) in renewal premium. The insurer's individual annualised premium equivalent (APE) rose 13 percent to Rs 6,260 crore for FY19.

Two highlights of its performance are a 67 percent jump in term protection APE at Rs 1,045 crore and annuity APE expansion of over 140 percent, though on a smaller base.

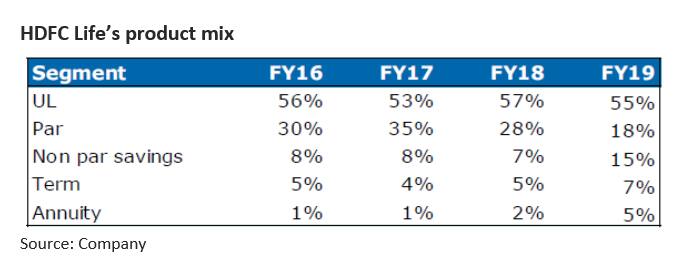

As for the business mix, the share of unit-linked insurance plan

(ULIPs) in individual APE declined 200 basis points YoY to 55 percent, while the annuity business reported a robust growth. HDFC Life’s continuous focus on the relatively high margin protection business (term insurance) was clearly visible as its share improved to 17 percent in FY19 compared to 11 percent in FY18 on an overall APE basis.

India has a high protection deficit among key Asian countries at 92 percent, according to 2014 estimates by Swiss Re. This implies that for every $100 required for protection, only $8 is spent by a typical Indian household, leaving a massive mortality protection gap. This represents a huge opportunity.

Given the significant potential in the annuity and protection business, we expect a further improvement in the product mix of HDFC Life, which should aid profitability.

Improving operating performance

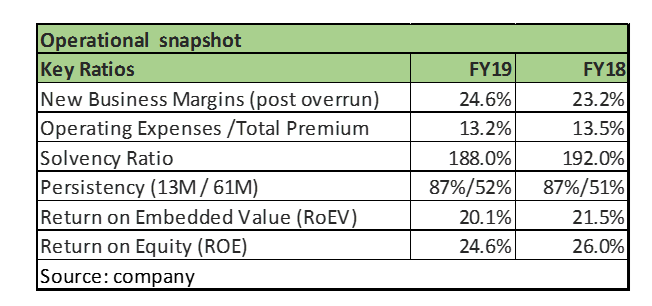

New business margin (post overrun) rose to 24.2 percent in FY19 compared to 23.2 percent a year ago. The insurer reported a 30 bps increase in operating expenses to 13.5 percent on the back of investments in expanding distribution channel, product innovation and digital platforms. For instance, distribution mix improved further, with the share of direct channel in individual APE rising to 19 percent against 14 percent in FY18.

Persistency ratio remained almost stable, aiding the renewal business. Overall, return ratios were strong and steady, with Return on Embedded Value (RoEV) at 20.1 percent and Return on Equity (RoE) at 25 percent for 2017-18. Solvency ratio declined to 188 percent as the insurer infused capital into its subsidiaries.

Stretched valuations, but a long-term compounderWe believe that the insurance sector is in a sweet spot, driven by structural factors such as a gradual but steady shift to financial savings, increasing share of life insurance within financial assets, buoyant capital markets, a favourable product mix and cost structure changes.

HDFC Life, in our view, is best positioned in the insurance space, with its strong and trusted brand recall, balanced product mix with leading position in the protection business, expanding distribution network, high technology focus, product innovation and experienced management.

In terms of valuation, the HDFC Life stock trades at 4.4 times its trailing Price-to-Embedded Value (P/EV), with a significant premium to its peers.

Given its best-in-class return ratios and profitability levers, we believe premium valuations might sustain and expect the stock to deliver steady returns over the medium term.

Investors looking for high quality business with consistent earnings growth may look to utilise adverse market volatility, if any, as an opportunity to add to the stock.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.