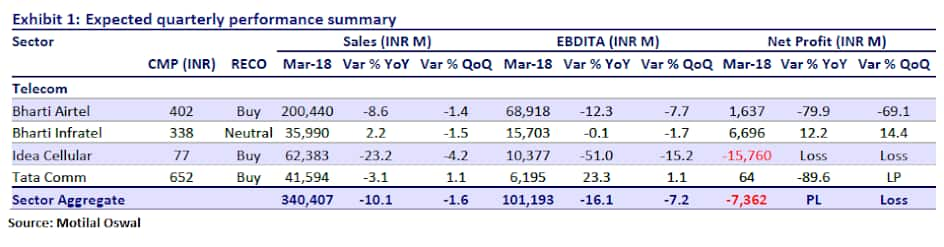

Telecom sector is expected to report yet another quarter of muted numbers except for Reliance Jio which should see double-digit revenue growth for the quarter ended March 2018, suggest experts.

Telecom universe is likely to report a loss -- Idea’s loss is expected to remain elevated while Bharti Airtel is expected to post 80 percent year-on-year (YoY) decline in profits.

The March quarter saw a fresh round of undercutting by telcos, with lower price plans focusing on market share gains compared to profitability to gain the 15 percent revenue market share still lying with smaller operators, suggest experts.

“EBITDA margins will continue to bear the brunt of revenue deceleration — estimate 300bps and 260bps dip in Bharti’s and Idea’s margins, respectively. Bharti Infratel’s (BHIN) revenue is estimated to grow mere 3.6% YoY due to industry consolidation and incumbent operators’ focus on enhancing capacity rather than coverage,” Edelweiss said in a report.

Commentary on ARPU trajectory, timelines of Idea-Vodafone merger and update on Bharti’s Africa business will be key monitorables, it said. “With smaller operators—Aircel and RCOM—shutting shop, subscriber migration to large operators will be keenly monitored,” said Edelweiss.

Edelweiss further added that RJIO’s incremental subscriber market share and pricing outlook will be key factors to decide pricing pressure in the industry.

Timelines on Idea-Vodafone merger and update on anticipated cost synergies will be key drivers for Idea Cellular. Also, Bharti’s update on demerging Africa business will be in focus, it said.

Top six stocks from the telecom sector in the March quarter:

Bharti Airtel Ltd: BUY

Motilal Oswal expects the consolidated revenue to decline by 1.4 percent on a quarter-on-quarter (QoQ) basis (and 9% YoY) to Rs20,040 crore. Given the continued ARPU down trading on account of the renewed competition from RJIo, brokerage firm expects India wireless revenue to decline 4.4 percent QoQ (and 21% YoY) to Rs10,280 crore.

Kotak Institutional Equities expects Bharti to report India wireless revenues and EBITDA of Rs10140 crore (down 5.7% QoQ, down 22% YoY) and Rs300 crore (down 15% QoQ, down 37% YoY), respectively.

At a consolidated level as well, the prognosis for the quarter is weak. We expect a 10 percent QoQ and 15 percent YoY decline in consolidated EBITDA to Rs670 crore despite healthy trends sustaining for the Africa ops, it said.

According to Kotak, Bharti Airtel could report fall in Adjusted net income to Rs3769 crores, a fall of 169 percent on a QoQ basis, and 184 percent on a YoY basis.

Bharti Infratel : Neutral

Motilal Oswal expects the consolidated revenue to decline 2 percent QoQ (but grow 2% YoY) to Rs360 crore. Consolidation in the sector is likely to continue pressurizing tenancies.

The domestic brokerage firm expects 2 percent QoQ decline in tenancies leading to 2 percent QoQ decline in consolidated rental revenue to Rs2210 crore. The Adjusted net profit is likely to fall by 6.9 percent to Rs2557.30 crore compared to Rs2747 crore reported in the year-ago period.

Idea Cellular: BUY

Idea's revenues are expected to further decline by 5.8 percent on a QoQ basis on 9.2 percent dip in the ARPU. Edelweiss expects the voice and data realisations to plummet 15.2 percent and 9.5 percent respectively, leading to 8 percent and 13.9 percent rise in voice and data volumes, respectively.

The EBITDA margin is expected to further nosedive by 260bps QoQ to 16.2 percent, which would swell net loss to Rs1440 crore from Rs1280 crore in the previous quarter. Update on timelines regarding the merger with Vodafone, strategy to tackle subscriber churn to RJIO will be key monitorables.

Tata Communications Ltd: BUY

Tata Communications’ revenue is expected to grow 1 percent QoQ (decline 3% YoY) to Rs4160 crore on steady data revenues, offsetting the impact of muted voice revenue.

Data revenue is likely to grow 2 percent QoQ (6% YoY) to Rs2950 crore whereas voice revenue is expected to decline 2 percent QoQ (and 20% YoY) to Rs1210 crore.

Core EBITDA is expected to grow by 1 percent on a QoQ basis to Rs620 crore on the back of data EBITDA, and Core EBITDA margin should remain flat at 14.9 percent. Data EBITDA is expected to grow 3 percent QoQ to Rs550 crore.

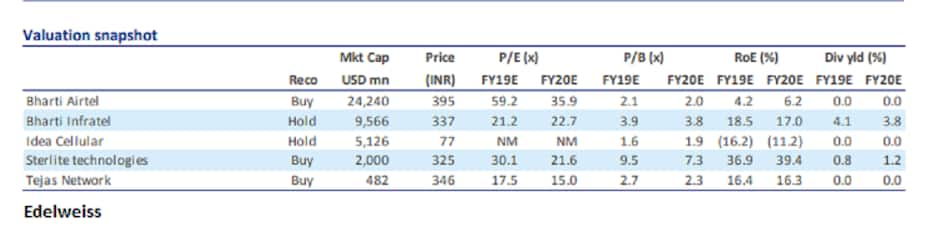

Sterlite Technologies Ltd: BUY

Edelweiss expects Sterlite’s revenues to jump 31.5 percent on a YoY basis, with products revenues growing 31.2 percent YoY and software and services revenues clocking 33.2 percent YoY growth.

The EBITDA margins are expected to rationalise by 30bps on a QoQ basis to 23.8 percent. The product and services order book, commentary on adoption of 5G technologies are key monitorables, said the report.

Tejas Network: BUY

Tejas’s Q4FY18 revenues are likely to decline by 32.5 percent YoY due to delays in receiving certain large orders. Considering the large size of orders and customer concentration, revenues of Tejas are lumpy in nature, Edelweiss said in a report.

Due to a massive decline in revenues, EBITDA margins are also expected to nose-dive 330bps YoY to 22.4 percent. Guidance for FY19, commentaries on deal-wins in BharatNet Phase II and outlook in emerging

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.