Neha Dave

Moneycontrol Research

DCB Bank, a small-sized private sector bank, delivered sub-par earnings in the first quarter of FY19. Significant margin contraction and elevated operating expenses undermined its performance.

The retail focused bank stands out for its comfortable asset quality in a sector marred by high non-performing assets. It enjoys strong parentage of the Aga Khan Fund for Economic Development (AKFED), which has provided capital as and when required. The healthy capitalisation will support future growth, making it a worthy contender in a weak banking environment.

Weak Q1

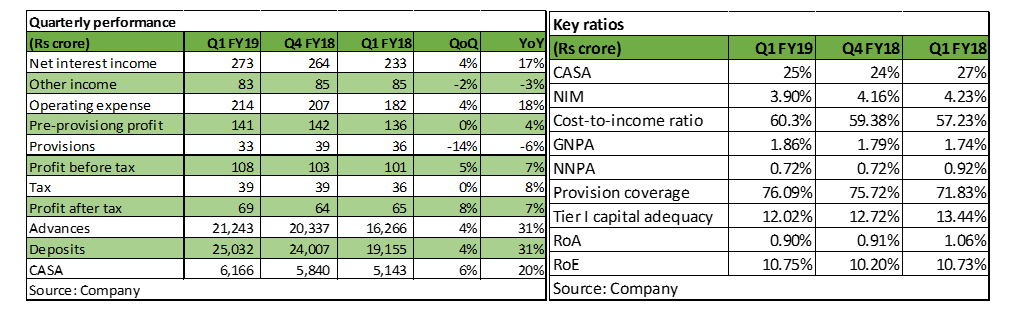

DCB reported subdued net profit growth of 7 percent year-on year (YoY) in Q1 FY19. Robust loan book growth (31 percent) was partially offset by a fall in net interest margin (NIM). As a result, net interest income (NII) growth was muted at 17 percent YoY.

NIM fell 26 bps sequentially and 33 bps YoY to 3.9 percent. There were too many moving parts, including higher cost of tier II bonds (9.85 percent) and decision to maintain excess liquidity, which adversely impacted NIMs. The latter compressed as the yields on advances declined due to rise in competition, especially in the corporate and mortgage segment, while the cost of funds increased due to rise in interest rates. The management guided at a margin of around 3.75-3.80 percent for the near future, indicating a possibility for further downside.

Non-interest income reduced 3 percent YoY as the 17 percent growth in core fee income was negated by a fall in treasury income. Thanks to branch expansion, operating expenses increased 18 percent YoY.

Though declining, the bank’s asset quality is relatively better compared to peers, with gross non-performing assets (GNPAs) at 1.86 percent as at the end of June. The provision coverage ratio remains healthy at 76 percent.

Profitability targets intact

Despite a weak last quarter, the management reaffirmed its FY19 guidance, which was comforting. The bank had earlier guided to achieve return on assets (RoA) of a percent and return on equity (RoE) of 14 percent by Q4. The management said the fall in cost-to-income ratio to 55 percent will aid in delivering its targeted profitability. While these targets are achievable, downside risks have increased considerably.

Balance sheet growth continues

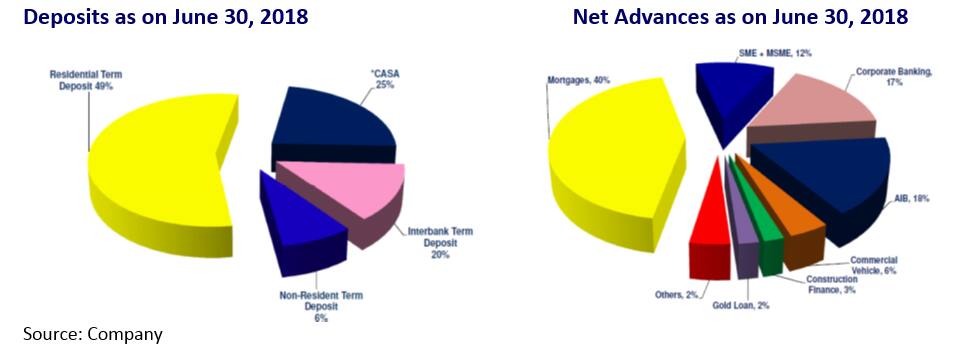

DCB has grown its advances at a very healthy pace, higher-than-industry average, albeit on a modest size. Growth has been driven by mortgage, agriculture and inclusive banking (AIB), corporate banking and small and medium enterprises (SME) segments which constitute 40 percent, 18 percent, 17 percent and 12 percent, respectively, of net advances as on June 30. Loan book has doubled in the last 3 years, with the management expecting the same run rate to continue in the future as well. This translates to targeted loan book growth of 22-24 percent for the next 3 years.

Generating operating leverageDCB has been on an expansion spree for the past 5 years, doubling its branch count from 154 in FY15 to 318 in FY18. As a result, its cost-to-income ratio and operating expense remains on the higher side, adversely impacting profitability. Going forward, the bank intends to add 15-18 branches per year over the next 2 years. As branches mature, we expect operating expenses to moderate and become more RoE accretive.

Complemented by improving funding profile

The bank’s funding profile remains average, with the share of current account-savings account (CASA) deposits at 25 percent, much lower than the industry average of around 35 percent. We draw comfort from the share of retail deposits (retail term deposits including NRI deposits), which stood at 51 percent of total deposits as at the end of June and lends stability to the bank's resource profile. We expect newer branches to achieve scale and bank’s retail deposits to grow at a healthy pace, which would aid lower borrowing costs.

Earnings traction could lead to a re-rating

Though margins might continue to be remain under slight pressure due to increased competition and rising rates, we don’t see much downside from here as the bank has increased marginal cost of funds (MCLR) linked lending rates which will support NIMs in coming quarters.

On the operating front, we see significant improvement as recently added branches start generating revenues. Comfortable asset quality, with negligible restructured accounts on books, negates the risk of higher provisioning as well. In fact, the bank has outstanding floating provisions of Rs 60 crore.

The big lever will come from accelerated loan book growth. Strong capital adequacy can support potential high loan book growth. However, the bank’s ability to maintain its margins and stable asset quality as it grows its book are key monitorables. Slippage on any of these variables will make DCB’s journey towards its stated target more arduous.

Going forward, we see the moderately paced improvement in return ratios primarily driven by balance sheet growth and operating leverage. However, it may take longer than the next 3 quarters to deliver the targeted returns.

On the valuation front, the stock is currently trading at 1.7times FY20e price-to- book, which is at a premium to many of its old private sector banking peers. We see the current valuation sustaining with levers of profitability improvement in place. However, upside in the stock will be driven by improvement in earnings growth. In the interim, as the stock continues to be weighed down due to uncertainty, investors could look to utilise this opportunity to accumulate the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.