")

Krishna KarwaMoneycontrol Research

Aditya Birla Fashion & Retail (ABFR) is among India’s largest pure-play fashion and lifestyle companies with a strong bouquet of leading fashion brands. As on March 31, the company’s network spanned e-commerce portals, 2,465 brand stores (including 275 Pantaloons stores), 4,982 multi-brand outlets (MBOs) and nearly 4,054 points of sale in department stores across the country.

The company operates through two segments. The Madura arm includes lifestyle brands (Louis Philipe, Van Heusen, Allen Solly and Peter England), fast fashion brands (Forever 21, People) and other businesses (branded innerwear and international brands). Pantaloons is a value-fashion business that caters primarily to aspirational buyers through its medium-priced branded apparel products.

Growth in lifestyle brands, brand-building measures, product innovations and reduction of losses in the fast fashion sub-segment will chart ABFR’s growth trajectory. In Pantaloons, addition of new outlets and operational efficiency should bolster overall profitability. However, the stock’s valuation seems to have discounted most of these positives and a staggered entry is being recommended.

Performance review

The company ended FY18 on a strong note due to improved performance in both segments and accounting for deferred tax benefits. In the case of Madura, lifestyle brands grew due to wedding and festive sales, fast fashion brands managed to cut their losses through cost optimisation, and branded innerwear business scaled up rapidly. Growth in Pantaloons was led by 66 new stores.

Why should investors consider ABFR?

Fast fashion (sub-segment within Madura)

‘Forever 21’, a brand in this category, has been witnessing a turnaround because of the management’s initiatives to channelise store-level processes and shut loss-making outlets. In ‘People’ brand, impetus will be on tapping large format stores, while simultaneously rationalising small format ones.

Other businesses (sub-segment within Madura)

For branded innerwear, the management is aggressively adding new outlets to its existing 6,700-store network. Investments relating to international brands will be scaled up too. These measures should yield healthy top-line traction in the long-run.

Pantaloons

Given the immense scope for growth in the under-tapped geographies in the value/mass fashion domain, the management is ramping up store launches at a quick pace. To keep the business asset light, most of the 50 new outlets proposed to be added in FY19 will be franchise-run. This could lead to better profit margins.

Fund raising

The board has approved a plan to raise up to Rs 1,000 crore through equity or convertible debt to strengthen its balance sheet. The proceeds will be primarily allocated to fund FY19 capex of about Rs 270 crore (Madura: Rs 150 crore; Pantaloons: Rs 120 crore). Consequently, 350 outlets will be added across all formats.

GST boost

Post implementation of the Goods & Services Tax (GST), tax rates remain largely neutral for the industry and segments in which ABFR operates. As the Indian economy undergoes formalisation, organised players are expected to garner a higher share of the market from unorganised counterparts by virtue of the level-playing field.

Other tailwinds

Online shopping is growing fast, thereby necessitating adoption of omni-channels. Increasing influence of globalisation and rising disposable incomes are fuelling growth of foreign brands in India. This bodes well for ABFR in terms of achieving strong brand visibility and facilitating product differentiation.

Risks and valuation

Prevalence of seasonality (the first half of a financial year typically tends to be weak) and extended ‘end of season sale’ periods can dent the company’s turnover/margin, respectively. Recovery in wholesale channels is weak, especially in south India. Infusing additional equity will be earnings dilutive till organic growth plans don’t translate to a corresponding operating and bottom-line leverage.

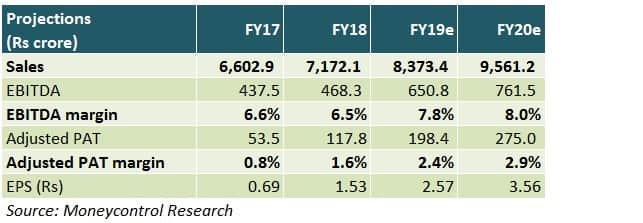

Owing to lack of clarity on the timing or terms of the additional Rs 1,000 crore capital infusion, we have not incorporated its impact in our estimates. Nonetheless, at 42.4 times FY20e earnings, the steep valuation leaves little room for immediate upside. Therefore, gradual accumulation would be the preferred choice.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.