A total of 531.3 million JanDhan bank accounts, a cumulative deposit balance of Rs 2.3 trillion with 67% in rural and semi-urban areas are impressive achievements for a decade old program. It had reportedly started out with a target of covering 7.5 crore uncovered households but ended up opening 12.5 crore accounts in less than six months from launch. Only a decade earlier, the 2011 census data showed that that nearly 41% the population did not avail banking services. Thanks to this push, by 2021, 78% of Indian adults had a bank account.

PMJDY was by no means the first initiative for financial inclusion but what set it apart was the mission mode and the use of technology, an element that was missing earlier. The nationalisation of banks and the setting up of SBI in the 1950s were in fact the earliest initiatives, which had approached the problem in terms of bringing banking majorly under State control. Later, the no-frills savings accounts and business correspondent schemes in 2005 sought to extend the physical reach of banking. But what changed the dynamics was technology, specifically the Digital Public Infrastructure (DPI) that had come into place. DPI covered three crucial elements viz digital identity, bank accounts and processing infrastructure. Around 1.4 billion Aadhaar numbers were issued (near universal coverage), a refurbished Basic Savings Bank Deposit (BSBD) with added benefits like built-in overdraft and accident insurance replaced the no-frills accounts while processing infrastructure came in the form of affordable mobile phones and low-cost internet. This fortuitous combination helped ramp up the number of mobile based internet users to nearly a billion now. Interestingly, all of this happened even before the true game changer arrived in the form of the UPI, a real-time payment system, which came much later in 2016.

Controversies Around JanDhan

The impressive growth also had its share of controversies. Even though they were pitched as accounts without minimum balance requirements, as many as 75% of the JanDhan accounts opened had zero balances which, many argued, reflected the real state of rural well-being where people could not afford to bring in even small sums of money. Not unsurprisingly, there hardly any transactions in the accounts given the low average balance (Rs. 3839 in 2023). The built-in overdraft facility of Rs 5000, for instance, was barely utilised. RBI data show that in 2015 only 76 lakh accounts of the total 40 crore BSBD accounts availed the overdraft at an average Rs 2600 per account. In subsequent years these numbers dropped significantly to a modest Rs. 572 in 2023. The low average account balances and low credit availed were pointing to the fact that access to a bank account was a necessary but not sufficient condition for improving financial well-being.

The argument is not without merits. Undoubtedly the increase in bank accounts, internet connections and mobile phones resulted in improved digital infrastructure, but they are really the plumbing in the system. Money would flow only from economic growth and the test of infrastructure would be in enabling growth. This is the case with physical infrastructure too. Power, roads, airports are vital to economic development, but their first order effects, usually the increase in construction activity or output in related sectors such as steel and cement, have only a limited effect on overall growth. What matters for growth are the second order effects- the increased number of new industries or businesses, the new jobs created or income generated from the improved infrastructure. Likewise, access to bank accounts, credit and payments infrastructure need to reflect in economic growth. This is not to suggest there has been none; digital payments have spawned a whole new genre of businesses and services that would have been unthinkable earlier. But for addressing the larger issue of poverty which is what financial inclusion really targets, programs have to go beyond the setting up of infrastructure.

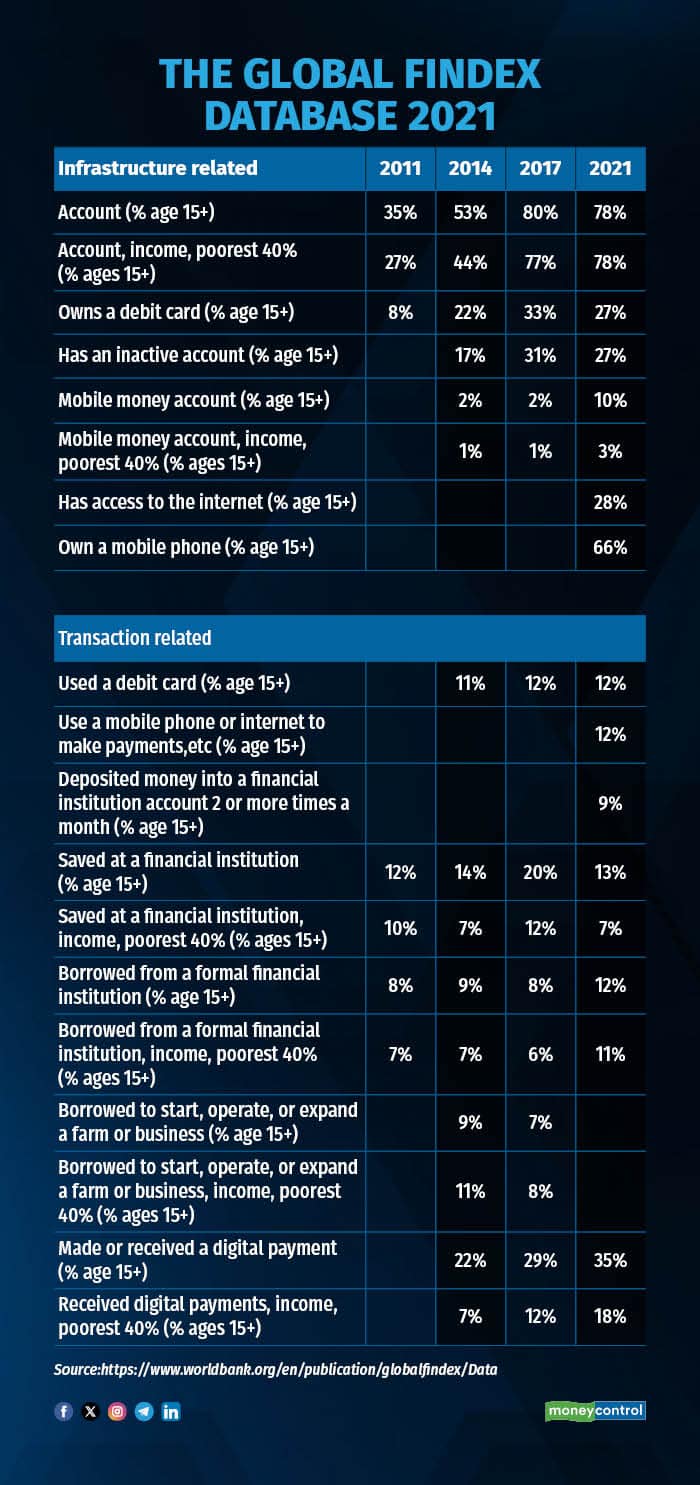

Gaps in JanDhan Usage

This also what data reveal. The World Bank’s Global Findex database, which tracks financial inclusion metrics across more than 140 economies, has a plethora of metrics under financial inclusion.

If we categorize them broadly as infrastructure (access) and transactional (usage) metrics, the differences are striking. Infrastructure refers to access to bank accounts, internet and mobile phones. These have improved significantly as data show. Usage typically is making and receiving digital payments, savings, borrowing, insurance and engaging in the broader financial ecosystem. Data show that the percentage of such activities has still remained, notwithstanding the improved access, pointing to where the real issues in financial inclusion are. The massive growth in digital payments maybe an outlier, coming mainly from the success of the UPI payment system. Here again, average transaction values have been low (Rs. 1524 in 2024) again pointing to the fact that economic outcomes may not have significantly changed, although more people have embraced the digital world.

All said, the JanDhan program definitely gave a shot in the arm to bank account opening which had been meandering till then. BSBD accounts jumped up by 50% in the five years from 2015 while the deposit balances went up by a massive 183%. The growth has since tapered off but the number of unbanked Indians still remains a high 190 million (recent estimates), which perhaps could be behind the Government recently announcing a plan to open 30 million bank accounts during 2025.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.