Arm Holdings Plc’s Nasdaq debut was supposed to energize the anemic initial public offerings market. But its roadshow, powered by more than two dozen investment banks, is looking like a hard sell. In their desperate attempt to earn fees and de-risk from Arm parent SoftBank Group Corp, bankers are getting investors worried.

The chip designer’s IPO shares are reportedly more than five times oversubscribed. It is now seeking to price at the top or above its range, valuing the Cambridge-based company at as much as $54.5 billion. Arm expects to price on Wednesday and start trading this week.

The oversubscription is not an indication of investor enthusiasm, however. SoftBank plans to sell only 9 percent of Arm’s shares, and will pledge out a 75 percent stake for margin loans once the stock debuts. Looking at data between 1980 and 2022, Jay Ritter, a finance professor at the University of Florida, found that historically, a company going public in the US, on average, offered 29 percent of its shares. Even those in the lower 25th percentile floated 20 percent, according to Ritter.

As such, Arm’s tiny float is an extreme outlier. Anticipating that the stock will be included in major indices, asset managers are forced to chase after the few shares available, with “little price sensitivity,” reported the Financial Times.

During marketing presentations, Chief Executive Officer Rene Haas and his bankers tried to convince investors that Arm would be a big winner in AI. Jensen Huang, founder of Nvidia Corp and the largest beneficiary of this year’s Nasdaq rally, showed up in a pitch video seen by Bloomberg Opinion calling Arm an “extraordinary company” with a “world-class management team.”

If AI exposure is what investors are buying into, this debutante is arriving a bit early, reckons AllianceBernstein Holding LP analyst Sara Russo. While Arm indicated in the prospectus that its central processing units, or CPUs,

were already running AI workloads in devices like smartphones and cars, it did not discuss explicitly their market opportunities. As it currently stands, an AI boom is most likely to boost demand for chips that go in servers, rather than in smartphones, where Arm is dominant but growth is slowing. “We didn’t see evidence of significant growth aligned to AI and machine learning, leading to whether Arm is a way to invest these themes,” noted Russo.

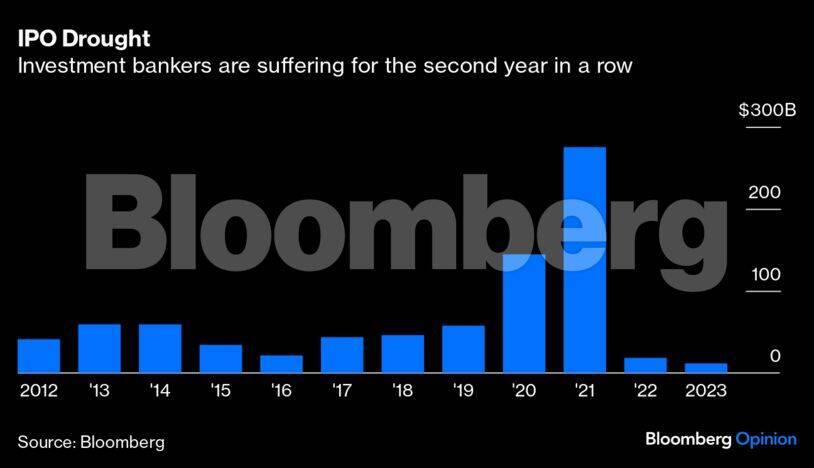

But when there is an IPO drought and SoftBank dangles millions of dollars, bankers are willing to tell any story, however stretched it is. The 28 investment banks working on this deal are set to share as much as $100 million in fees. The four leading underwriters — Barclays Plc, Goldman Sachs Group Inc, JPMorgan Chase & Co and Mizuho Financial Group Inc — can get paid $17.5 million each, with the remainder divided among the other brokerages. So far this year, banks have collected only $323 million in IPO fees, according to data compiled by Bloomberg.

Banks need to ring-fence their own balance sheets, too. Last year, as part of their effort to win this IPO, they had given SoftBank $8.5 billion in term loans backed by Arm’s shares. This risky financing came despite the collapse of Archegos Capital Management in 2021, whose failure to meet margin calls inflicted huge losses on Wall Street brokers. Once Arm becomes publicly listed, it will be easier for banks to offload the pledged assets in the event of margin calls.

For $100 million, SoftBank makes sure Wall Street works hard. After the IPO, its bankers will offer a new $8.5 billion loan that is backed by 75 percent of Arm’s stake. Because of the tiny public float, their counterparty risk is only partially mitigated. In the event of a margin call and if SoftBank is unable to deposit additional funds, banks that do not have strong relationships with hedge funds and private wealth clients may end up being forced to sell Arm shares in the open market — probably at a substantial discount — and take credit losses.

SoftBank founder Masayoshi Son’s incentives are clear. Give the public only a few shares so they can bid up Arm’s valuation, which he can then use to get better margin loans. But what does it mean for the broader market? By telling a difficult story, bankers are signaling to investors that we are near the end of an AI-fueled rally.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. Views are personal, and do not represent the stand of this publication.

Credit: Bloomberg

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.