Madhuchanda DeyMoneycontrol Research

Thermax is a company catering to broad segments of energy and environment, with a presence across a gamut of engineering services from power, heating, cooling, water, chemicals, waste water, air pollution control, hazardous waste treatment and waste-to-energy generation.

With its technological prowess, it is positioned rightly for the future. However, reported numbers for the final quarter and FY18 were uninspiring. Order inflow and backlog was worth taking note of. While the management alluded to much better visibility in coming years, valuation at 31 times FY20e earnings limit near-term upside.

Quarter at a glance

For the quarter-ended March, the company reported a revenue decline of five percent year-on-year. Adjusted for Goods & Service Tax (GST), the same stood at three percent YoY. The decline was contributed by energy and chemical segments.

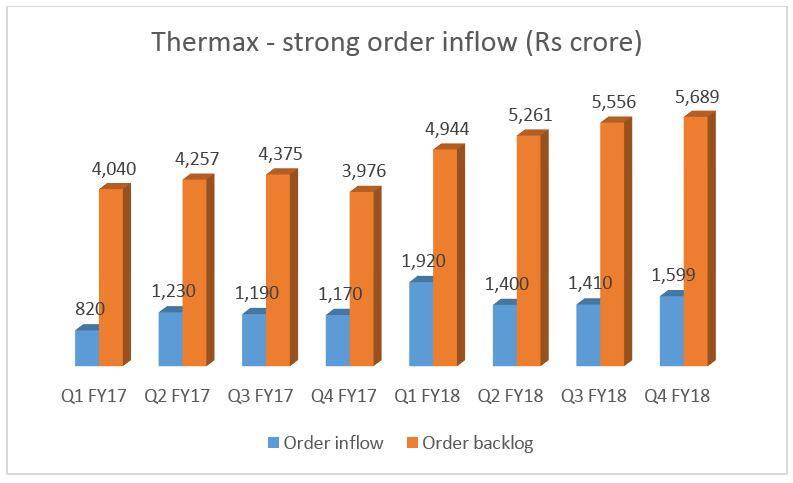

Source: Company

The management attributed revenue loss to the tune of Rs 200 crore in the quarter gone by to implementation of the e-way bill. Profitability margin too was impacted on account of lower revenue and disappointing performance of overseas subsidiaries. Quarterly margin was hit by temporary losses in Danstoker and its Chinese subsidiary as the company provided for four litigations there.

In the air pollution business, the company bore the brunt of rising steel prices, while up fronting cost of the new plant impacted margins in the chemicals segment.

While topline and profitability were lacklustre, momentum in order inflows has been extremely encouraging.

Order inflow the sole bright spot

In Q4 FY18, the company reported a 37 percent YoY increase in order inflow at Rs 1,599 crore and a 43 percent YoY increase in order backlog at Rs 5,689 crore (1.3 times FY18 revenue). Total order inflow in FY18 stood at Rs 6,380 crore, an increase of 45 percent over FY17.

Growth in topline (as it is sitting on a healthy order book) should benefit operating leverage. With an improved ordering environment, passing on of higher input prices might be easier, especially since a majority of its clients are repeat customers.

The company should also reap the benefits of rupee depreciation, positively impacting margins on export orders. The management sounded hopeful about increasing its margin into double-digits in FY19 but is still cautious about the same magnitude of order flow. In FY18, it bagged five large orders that substantially helped grow the book. While ordering momentum has improved, the ticket size of orders are much smaller.

Where are the green shoots?

The company is witnessing green shoots in all areas of infrastructure, besides power. It is expecting orders from the capacity expansion of two large Indian steel majors. The management is also hopeful of receiving orders from the oil & gas space in the second half of FY19. Cement manufacturers are planning to expand capacity owing to improvement in utilisation. Thermax also expects capacity addition in aluminium, copper and fertiliser sectors.

Capacity in place – waiting for the momentum

The company has requisite capacity in place to take advantage of any revival. Thermax has invested in three additional manufacturing facilities that will start contributing to incremental revenue.

The facility in Indonesia would be the manufacturing hub for Association of Southeast Asian Nations (ASEAN) and should start contributing immediately. The market potential is around $400 million and the company aims to garner 14-15 percent market share.

The first phase of the specialty resins plant in Gujarat (at Dahej) is ready and a full ramp-up will happen by Q2 FY19. Thermax is planning to further expand its chemicals capacity at Dahej.

Work has already started at Sri City (Andhra Pradesh) for setting up a manufacturing plant for vapour absorption chillers. This will be a state-of-the-art facility, highly automated and would require much less manpower. The plant should contributing in the second half of FY19.

The management has decided to acquire Babcock & Wilcox’s 49 percent stake in the joint-venture for manufacturing subcritical and supercritical boilers. While details of the transaction has not been shared, the management feels it will own a world-class facility at a competitive price (less than the replacement cost). This move will give Thermax access to air pollution-related NOX (reduced nitrous oxide) technology as well.

While the company’s Chinese operation is facing challenges in the local market, it plans to continue with the same for the world-class facility in China, which will enable it to cater to short-cycle orders for the global market.

In the past one-year, the stock has risen 17 percent and is now valued at 31 times FY20e earnings. Only if the green shoots translate into robust ordering can a further re-rating take place. Hence, we recommend a buy on dips. For existing shareholders, riding the early momentum may be worthwhile.

Source: Company, Moneycontrol Research

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.