Small banks Equitas and AU Small Finance have one thing in common – both were formerly NBFCs. But the similarities seem to end at that. Equitas was roiled by the problems in the micro finance sector post demonetisation, and is still feeling the pain. AU Finance on the other hand, has been plodding steadily in its new avatar as a small bank. Not surprising then that AU commands a far higher valuation than what investors are willing to pay for Equitas. With both banks having announced their second quarter earnings, let us check which one makes a better investment bet.

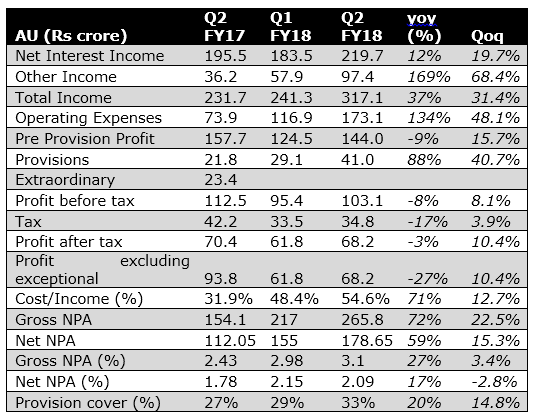

AU Small Finance Bank’s operating numbers were tepid. A steep jump in operating expenses (see table below) restricted pre-tax profit growth to 8.1 percent quarter-on-quarter even as net interest income rose 19.7 percent and total income 31.4 percent. Net profit growth was slightly better at 10.4 percent. Much of the rise in operating expenses was mainly on account of conversion to a bank

There has been no incremental deterioration in asset quality with gross and net NPA at 3.1 percent and 2.09 percent, respectively. The bank expects the cost to income ratio to moderate as operating leverage kicks in.

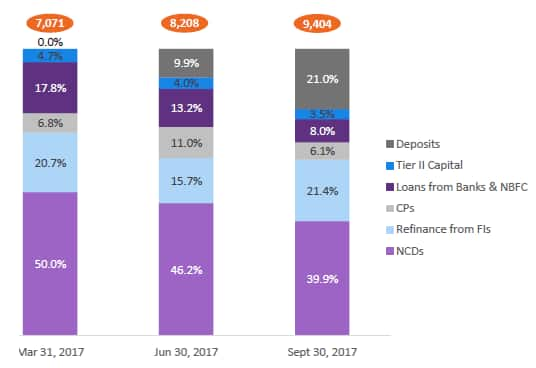

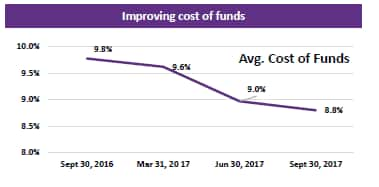

What we liked about AU’s strategy is the steady pace of execution on the asset as well as the liability side. On the asset side, disbursement has grown by 45 percent (YoY) to Rs 2500 crore. On the liability front, the growth in deposits is showing traction and the cost of funds declining that should aid margins.

The retail focused (85 percent of assets under management) entity is well capitalised (Tier I CAR of 20.6 percent) and is executing a well-chalked out strategy including several tie-ups in the third party distribution front to strengthen its business focus. Investors should see the 30 percent plus growth in business translating into decent earnings in the next couple of quarters. But valuation at 8.1 times FY18 book leaves little upside. Investors should only look at this stock when there is a meaningful correction.

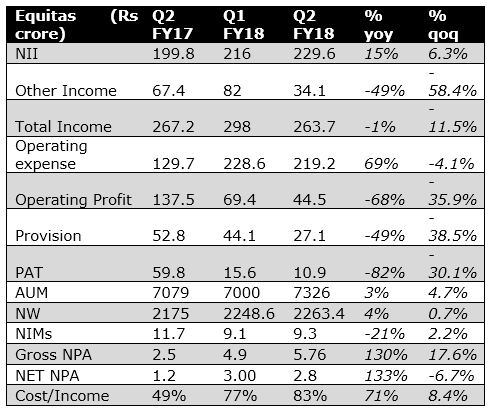

Equitas optically looks much more reasonably valued at 2.2 times FY18 book. But the conversion to a bank was accompanied by a jolt to its micro finance portfolio (MFI), which pushed up its gross NPA from 1.6 percent in Q1 FY17 to 5.76 percent in the quarter gone by and a squeeze on profitability.

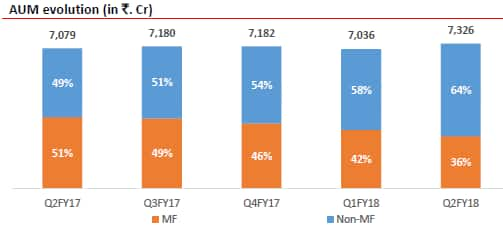

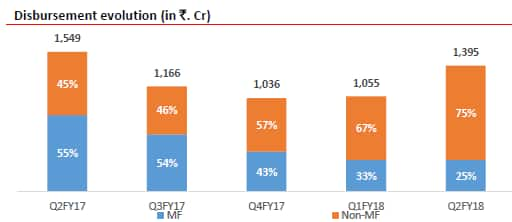

The company nevertheless has been steadily de-risking its asset book and the share of micro finance business has been coming down steadily.

It is also heartening to note that loan growth is picking up and the incremental growth in the loan book is being driven by the non-micro finance portfolio. The management’s strategy is not to let any product to dominate the portfolio.

The other key positive takeaways from the otherwise lacklustre second quarter performance is the relative stability in operating expenses, slight improvement in the ground reality for the micro finance business(stability in the collection ratio) and the management’s clarity of growing the business in a diversified/de-risked manner.

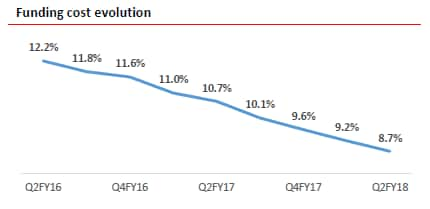

Interestingly, Equitas is garnering deposits at a steady clip and deposits now constitute 42 percent of total borrowing (with low cost CASA at 11.9 percent). Cost of funds are falling and this should cushion the margins at a time when the bank is trimming its exposure to ultra-high yield, but risky, products.

The asset quality is not very comforting, but almost 80 percent of the “portfolio at risk” in the micro finance book of Rs 176 crore is already a part of gross NPA. Hence, the bank is a couple of quarters away from putting its micro finance related asset woes behind.

The clarity of strategy should lead to resumption of earnings growth and improvement of return ratios few quarters down. The interim weakness could be used as an opportunity to accumulate this intrinsically high ROA (return on assets) business at a discount.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.