Malls in India are going through their share of challenges following various lockdown-like measures by state governments. There is either a complete closure of the malls or they are open for restricted business activities for grocery and other essential retail services with strict timings. Since the start of the pandemic, multiplexes have either been shut or running at very low capacity.

How is this affecting the investor sentiment in Indian retail malls? Does the argument for more malls based on growing Indian middle class and their purchasing power still hold good?

To answer these questions, we have to look at the intrinsic nature of shopping malls as places that necessarily facilitate social interaction and superior consumer experiences. Multiplexes and entertainment centres within malls act as anchor tenants, generating large footfalls which then leads to more business for food courts and fine-dining restaurants. Premium shopping malls attract well-known domestic and global shopping brands, leveraging the reputation of these destinations as major crowd-pullers.

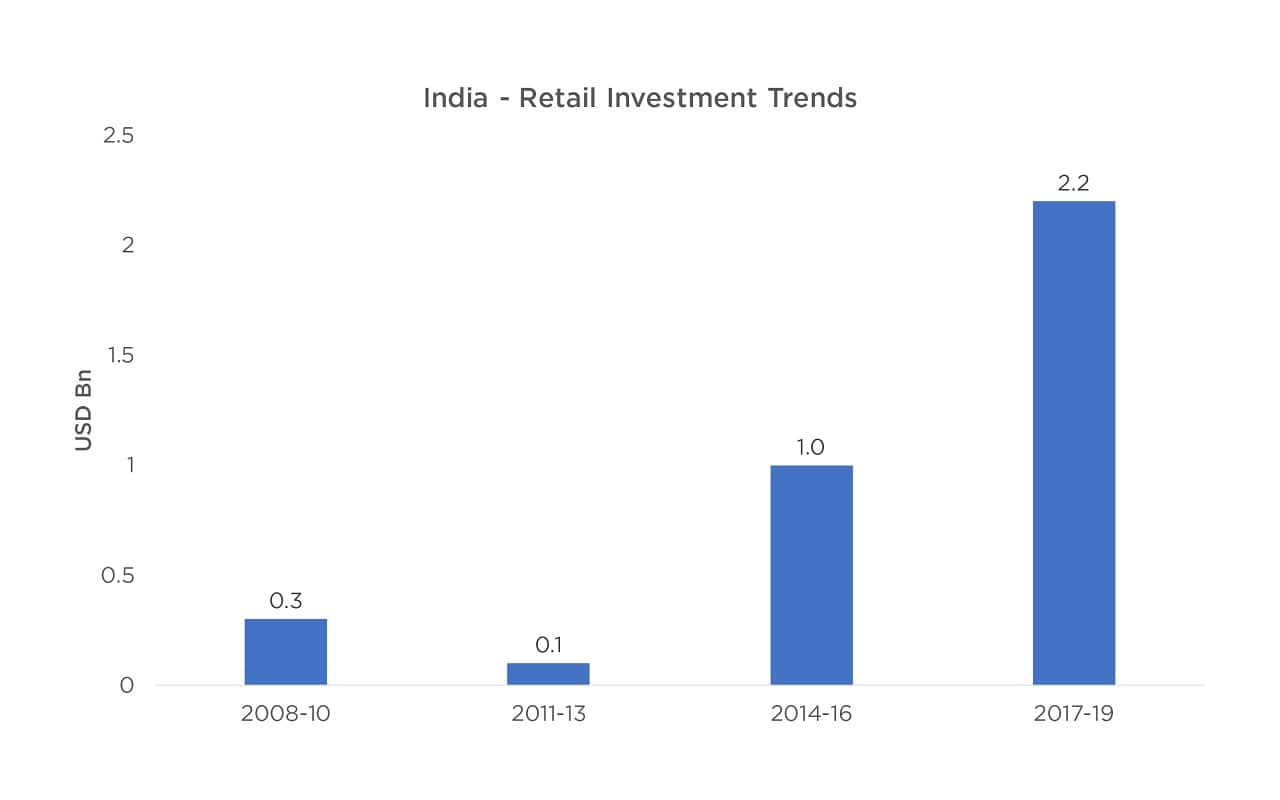

Over the past decade, as the tastes and preferences of Indian consumers have evolved and shopping malls have attracted large amounts of foreign capital. The retail sector has attracted foreign direct investment (FDI) in both completed and under construction malls to the tune of $3.5 billion from 2008 to 2020 but out of this, around 65 percent of the investment has come in the last three years (see Chart 1 ).

Given that India is still an unexplored story and the country remains an undersupplied market of premium Grade A shopping malls, we can safely say that the retail growth story is far from over despite the near-term Covid-induced uncertainties. Indian malls are here to stay and are likely to outperform other real estate asset classes over the medium to long term.

Source: CWI Research

Evolution of Indian shopping malls

India started with retail development in the early 1990s but it was restricted to the big cities like New Delhi and Mumbai. The real scale of development began after a decade or so and the mall revolution was expected to reach even the Tier II cities with projects being announced in Aurangabad, Nashik, Nagpur, Coimbatore, among other cities.

However, the entire euphoria around malls became muted after the 2008-09 global crisis and the impact it had on financial markets. It may not have impacted the rising middle class and their purchasing power but it clearly impacted the outlook for financial/investment decision-making. Hence, the mall revolution hit a pause before it gathered any significant momentum in any of the major Indian cities.

Nevertheless, without delivering meaningful supply, many mall developers started selling spaces and units to investors or occupiers (retailers) to generate enough liquidity to complete the mall or to reduce the debt burden at the group level.

The performance of most of the malls which were strata-sold declined over a period as there was a lack of management focus and interest from the owners. Many developers learnt the hard lesson that retail mall business was not only brick and mortar real estate but required components of hospitality (property management and providing a great experience to the consumers) and a very active management that arranged promotions, events, manages tenant mix/churn, etc.

Low mall density, consumption growth will drive expansion

Over the past decade, the performance of some shopping malls has declined and vacancy levels have risen, which, in turn, have created funding challenges for mall developers. With new mall developments becoming a challenge for smaller players, the sector has witnessed a few strong pan-India developers like DLF, Phoenix, Inorbit and Prestige with established reputation in terms of project quality and management taking a lead in Grade A mall projects.

Mall density in India is significantly lower than other nations in the Asia-Pacific (APAC) region but that is likely to provide immense scope for growth over the next few years. Favourable long-term consumption trends and growth of Tier 2 and 3 markets will put the retail sector in a sweet spot over the medium to long term.

The above-mentioned trends are already visible. Considering India will remain one of the fastest-growing economies in Asia, it is going to continue creating employment across sectors quite exponentially, and especially the service sector (considering the strength of the Indian IT sector).

These jobs would lead to more disposable income for the new young employees and families. Based on this potential, and pent-up demand in Tier 1, Tier 2 and 3 cities, large developers have started developing Grade A malls.

By retaining full ownership of these malls, and with a more matured understanding of the business, they have focussed on managing tenant mix quite deftly, and are comfortable signing revenue share deals with established brands. Such malls are doing very well for both developers and investors and tenants. These large developers continue to pour concrete for Grade A malls across the country.

Last year during the pandemic, Phoenix Market city opened their Grade A mall in Lucknow to a great response from the public. Even though the city has fewer malls, this is the first mall of such a size in Lucknow and will also attract shoppers from neighbouring cities, once the COVID-situation improves.

There are several other examples of new Grade A malls performing very well compared to other smaller malls in cities across the country like Seawoods Grand Central Mall in Navi Mumbai. Another example is Lulu Mall in Kochi which has had the best footfalls and trading density in the city compared to other smaller, average malls.

This reflects the public demand and acceptance of well-designed and managed malls. It may be noted that even amid the pandemic, vacancy levels in superior Grade A malls have been in the low single digits and demand for quality retail space remains robust.

Greater digitisation, experiential shopping will attract investors

Over the next few years, shopping malls are likely to evolve into locations where wholesome, superior consumer experiences are prioritised by all stakeholders.

E-commerce is often mentioned as the reason behind an adverse impact on the performance of malls but with most mall owners focussing on providing customer experience, malls are no longer just shopping destinations. Apart from movies, fine dining, events, family entertainment centres, malls are also providing enhanced social interaction.

It is important to acknowledge that most Indian cities do not have enough open parks or other recreational options unlike developed markets, resulting in mall visits becoming a weekend routine for most youngsters and families.

New-age technologies such as artificial intelligence (AI) and augmented reality (AR) are likely to become an integral part of business strategy as will greater attention to health and safety of visitors in the post-COVID era.

The above developments will attract more investors in premium-mall space. India will probably remain one of the few countries in the region where greenfield mall developments will continue, with new investment platforms formed between leading developers and large private equity partners facilitating investments. CPPIB – Phoenix, Lakeshore India, Warburg–Runwal are good examples of such investment vehicles. Long-term institutional capital inflows will continue in premium shopping malls and we have seen this play out with players like Blackstone, GIC as well.

Retail cap rates

There is a long-standing debate that retail rentals are more volatile compared to office space and hence cap rates should be higher than office assets. Retail rentals can vary considering revenue share and shorter duration of lease term compared to office space, however, as explained above, Indian retail is a different story and before we conclude on cap rates, it is important to look at the growth rates of rentals (net operating income) in these malls.

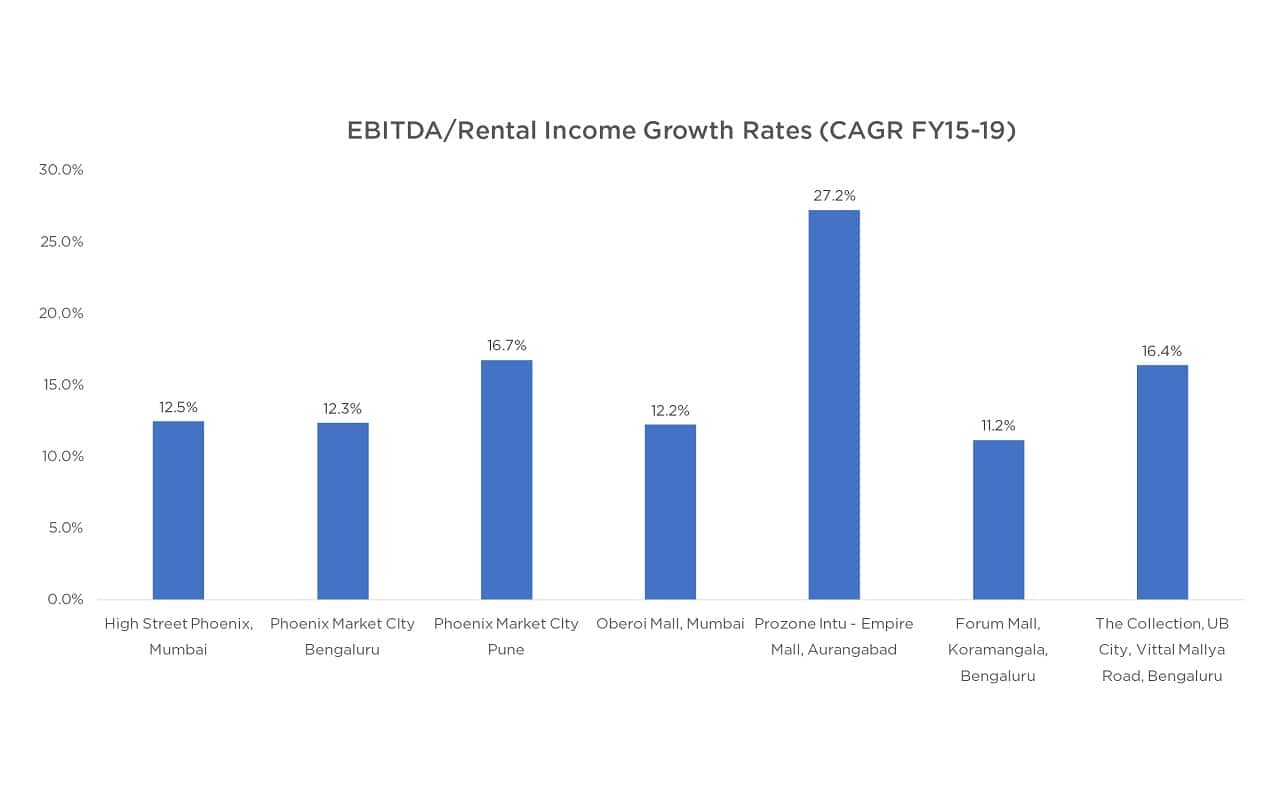

Most Grade A Malls have demonstrated higher growth rates compared to stable office assets. It is not unusual to see double-digit growth rates in malls. For the sake of comparison, we have assessed the trend until FY19 to avoid any Covid-19 related disruption.

From the chart, we can observe a CAGR of >10 percent over five years compared to office rental growth rate of 5-7 percent (depending on marked to market rental portfolio). Given this and the overall return matrix, a more competitive cap rate for a retail asset in comparison to office assets is a logical consideration.

Source: Investor presentations of Phoenix Ltd, Oberoi Realty, Prozone Intu Properties Ltd, Prestige – FY15-19.

As data is readily available for listed company’s malls, the above chart only considers data of such malls.

In conclusion, India’s demographic dividend is well known and its middle class’ increasing purchasing power augurs well for the success of retail malls. Covid-19 is a short-term setback but post stabilization of the economy and travel, this industry is going to come back stronger and deliver exceptional returns to investors.

(The author is Managing Director, Valuations and co-head Capital Markets, Cushman & Wakefield)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.