Khyati Dharamsi

Zareena Mistry, a 34-year-old Mumbai-based lawyer and her group of six friends were on their way to their hotel in Paris for a two-day halt before returning to India. That’s when Zareena realised that she had forgotten her bag at the airport.

Back at the airport, the missing bag had caused the authorities to panic. Paris was on red-alert at that time; the security personnel assumed that it was a threat. They just blew apart the bag. They didn’t even open it.

Her woes didn’t end there.

She had to spend around 300 Euros (Rs 24,000) the next day in Paris shopping for a new suitcase and clothes. Items and clothes worth Rs 20,000 were in the suitcase that was blown apart. Her total loss: around Rs 45,000. She was insured for a baggage loss of up to 1300 Euros (roughly Rs 1 lakh).

Despite having a travel insurance cover, Zareena had to silently bear the loss.

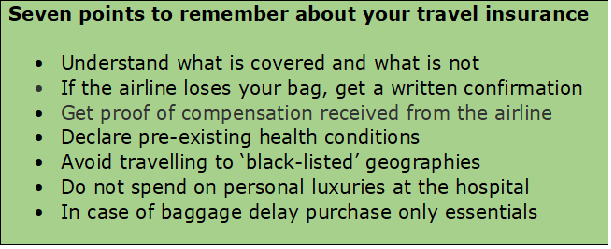

Why? Because her insurance policy covers her loss of baggage only while it is in the airline's possession. If the baggage is lost elsewhere, travel policies wouldn’t make good the loss.

The devil lies in the details

Though the glossy brochures feature attractive sales pitches using words such as ‘Secure your Trip,’ ‘Loss of Baggage,’ ‘Emergency sickness,’ ‘Trip Delay/Cancellation,’ the coverage reality is different.

As Pallavi Roy, Head - Products, IFFCO Tokio General Insurance Company states, “The insurance policy covers the damage or loss of checked-in baggage with the same airline/carrier in which the insured is travelling. Any unattended baggage left at the airport or any other place by the negligence of the insured is outside the purview of policy coverage.”

Most travel insurance policies cover loss and delay of only the checked-in baggage, from the time it is handed over to the aircraft authorities, until the time you receive the bag. Any damage or loss during the period while you are at the airport, after you alight and are out of the airport is unprotected under insurance.

“However, there are certain policies that cover loss of baggage from the start to the end of the journey and you should check for exclusions before purchasing a policy,” suggests Anik Jain, Co-Founder & CEO, Symbo India Insurance Broking Limited.

Mind the restrictions

Even if you lose or damage your luggage due to your airline’s fault, your claim amount can be restricted. Typically, the insurance firm pays you the amount, which is restricted to the sum assured mentioned under the “Loss of Baggage” clause of your policy. There are other clauses that restrict the total claim based on the number of bags you lose. “The checked-in baggage is covered as a percentage of sum assured. If the traveller is carrying one bag checked-in or carry-on, it gets 100 per cent cover; if two bags are carried then the sum assured is divided as 50 per cent for each bag,” says Jain.

Any compensation that the airline gives you for baggage delays is promptly deducted from your insurance claim. So, if you claim that your total due to the value of goods in the bag was 600 Euros and the airline compensates 150 Euros, then the insurer would deduct that 150 Euros, before handing over the insurance compensation.

That’s not all. If your money gets stolen, your travel insurance, typically, does not compensate for it. Zareena relates an incident where one of her friends was pick-pocketed in a train in Paris. Despite making a claim as early as in November and submitting documents, including a police report that she had filed in Paris, she hasn’t yet heard from her insurance company. Her insurance policy, in fact, has ‘mugging benefits’ worth $750 (or Rs 50,000) for a day.

A caveat for the ‘mugging benefits’ clause mentions that only if the policy holder is hurt or injured during the theft and requires medical help, the said amount can be paid as insurance compensation. Meanwhile, her loss: 500 Euros or close to Rs 40,000.

Trip cancellation

A Pune-based senior citizen couple were all set to embark on a two-week, Eastern Europe tour, back in September with Cox & Kings. Even as they held the visa in their hand, they got a call announcing the cancellation of the tours, just a fortnight before they were to leave.

In October, one of the travel firm’s creditors dragged it to National Company Law Tribunal to initiate insolvency proceedings. According to Economic Times, the company thereafter said that the International Air Transport Association (IATA) had terminated its licence to sell air tickets and asked it to surrender the IATA ID card.

Faced with a last-minute cancellation in September, the senior citizen couple had to re-book with another travel firm for a similar tour they eventually took. Meanwhile, the Pune-based couple who spoke to Moneycontrol said that Cox & Kings hasn’t yet refunded their tour cost (Rs 2.5 lakh). They are not alone.

Email and calls to Cox & Kings regarding the issue remained unanswered. Senior management calls too were answered stating that no one has been reporting to office, as the matter is with the NCLT (national company law tribunal).

Though Trip cancellation as a benefit is mentioned in travel insurance policies, there is no respite for such travellers under travel insurance. “While coverages vary between insurance companies, most travel insurance plans do not cover cancellations arising out of the liability of the travel agency. Thus, if a travel agency cancels a trip because it went out of business, the insurance claim may be denied in such a circumstance,” clarifies Jain.

Special situations not covered

If you like adventure, make sure you buy the right travel insurance; ordinary travel insurance won’t cover for any injury that you could incur in, say bungee jumping or sky diving.

Lost your passport? Sure, you are covered for the expenses incurred in getting another passport issued, say many travel insurance brochures. What they do not tell you is that if you lose the passport that was inside a bag left unattended, there is no guarantee of an insurance refund.

Losses due to terror attacks are not covered. So are claims made for travel made to certain black-listed countries such as Afghanistan, Cuba or the Democratic Republic of Congo, as per the policy documents of Bajaj Allianz General Insurance and Tata AIA General Insurance that Moneycontrol reviewed.

Health conditions that have been prevalent earlier and warrant hospitalisation overseas too would not be covered by the travel policy. “If the policyholder suffers from a pre-existing disease or is a smoker, the premium rises. Complications arising out of undisclosed pre-existing illness are generally not covered under a standard policy and one may have to purchase add-on covers,” says Jain.

But don’t hide the details. Disclose all your pre-existing diseases at the time of buying an insurance policy and make sure you have your doctor’s permission to travel abroad.

Make sure you have these documents

Documentation is very important while making travel insurance claims, because if you incur losses in a foreign country, you cannot possibly go back if you have not done your mandatory paperwork there. Get the Property Irregularity Report with the airline when a bag is delayed or lost. Report loss of items to the local police and get a copy of the first information report. If you were ill while travelling abroad and needed medication, get the doctors’ diagnosis, prescription for medication and the line of treatment recommended. Of course, your hospital and medicine bills are required to be filed as well.

“The customer should file a claim with the Carrier/airline as soon as possible within the time frame as defined in the policy,” says Roy of IFFCO Tokio Insurance.

If your claims have been rejected, get in touch with your insurance company’s Chief Grievance officer (your policy document has the name and contact of the person or you could even get in on the company’s website) and find out why. “In case you don’t hear back or aren’t satisfied, you can approach the insurance ombudsman or the Insurance Regulatory and Development Authority, through its website,” says MD Garde, former general manager of New India Assurance.

Moneycontrol’s take

Reading a 20-page insurance policy may be the last thing on your mind at a time when you are looking to embark on a cruise or a flight. But for every claim your travel insurance policy claims to have covered you, there appears to be a whole machinery behind that would be working to reject your claims when you get back. It pays to understand what you are covered for, and what you are not, to avoid disappointments later.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.