Life insurance is one of the important pillars of personal finance. In the COVID-19 era, this has assumed greater significance.

In case of the death of the insured individual during the policy term, the death benefit (a lump-sum amount) is paid by the insurance company to the beneficiaries named by the individual. If the person survives the tenure of the policy, he/she doesn’t get anything back.

The fact that insurance is not an investment has gained traction over the last few years. Term plans are pure insurance covers. They are cheaper than normal life insurance-cum-savings plans.

The objective of taking a term cover is to provide financial independence / freedom to your dependents, so that they are able to take care of their lifestyle as well as milestone costs (education / marriage expenses, parent’s health / loan repayments etc.).

Preserving lifestyles

Lifestyle expenses account for 40-50 per cent of taxable income, and assuming a post-tax return of 4-5 per cent on investments, a term cover enables dependents to maintain the present cost of living after the death of the policy holder. Additionally, the term policy should cover inflation, milestone costs and contingencies, especially if the individual's savings / investment corpus is not sizeable.

Human life is an appreciable asset for a variety of reasons; at least income generally keeps rising till the person retires. In addition to income rising, the financial responsibility on the individual also increases.

Insurance is taken to mitigate a potential risk. Here the risk is of a premature demise. So, the individual's term insurance cover should be calculated after factoring in the existing savings / investment corpus.

You should consider the following factors:

- Future Value cost of living expenses for all financial dependents

- Future costs of important milestones

- Liabilities: Home Loans and any other outstanding loans (existing outstanding amount)

- Any other financial commitments made: Guarantees / contingent liabilities, especially in the case of the self-employed

Factoring inflation

Future costs are computed by compounding the present costs using inflation as the basis. The cost of living can be increased using the inflation rate and compounded till the retirement age. For milestone expenses, it is better to reflect on immediate past history as to how the expenses have increased over a period of time. So, if the targeted post-graduation expenses have doubled in the past eight years, then the inflation for education must be projected at 9 per cent annually.

The aggregate quantum of money associated with the above items is the bare minimum amount for the term cover. In addition, depending on an individual's lifestyle risk, the cover should include:

-Accident and disability related coverage if he/she is a frequent traveller or has an adventure streak

-Additional costs for expenses which are not provided under medical insurance (applicable for those families who are genetically prone to certain ailments and / or hereditary issues)

An individual needs to address this as a first step before he commences his financial planning exercise, as, investment allocation in different asset classes can subsequently be easily aligned to meet the above target.

In other words, if an individual believes his investment corpus will meet all the above expenses as well as any eventualities, then he could limit / avoid his term insurance.

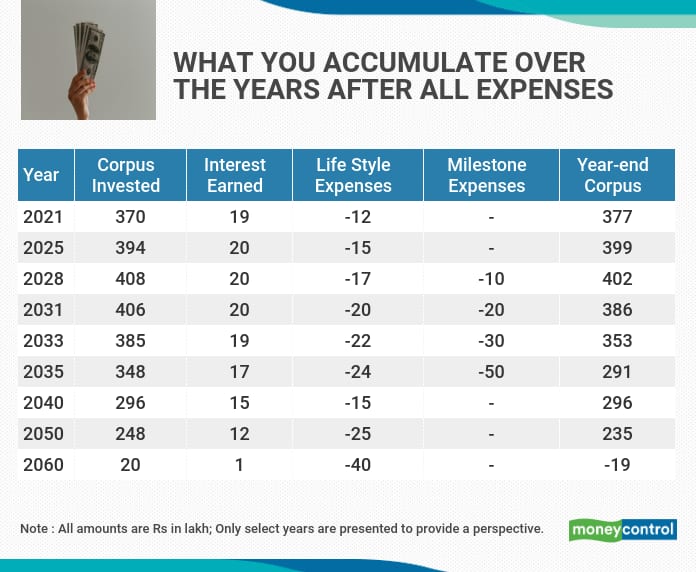

Example, X is 35, with retirement expected at 60. His annual income of Rs 24 lakh. He is married and has twins aged 10, with no other dependents. He has zero savings. His current monthly expenses are Rs 1 lakh. He has an outstanding home loan of Rs 30 lakhs. Life expectancy is assumed to be 75 years considered for his spouse. Lifestyle expenses to halve after girl are settled.

His term cover should be Rs 4 crore. After paying off the home loan, his wife will have Rs. 3.7 crore, which she can invest and meet her expenses for life, as shown below. Interest on investment and inflation, both are considered at 5 per cent per annum.

A thumb rule used by many insurance companies is that the maximum term cover they can offer is equal to number of years to retirement multiplied by your current income. So, in the above example of Mr X, his maximum coverage could be 24 lakh x 25 (60-35) = Rs 6 crore.

This is the maximum term cover you can get across multiple insurance companies. You should always disclose the current term coverage to insurance companies when you are opting for a new policy, or else dependents could face issues while making claims.

It is advisable to not take term covers from multiple companies. Restrict to 1-2 companies, which are likely to survive in the foreseeable future.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.