Ishita Sengupta

While 60s can be a great time to get that kitchen garden started in your backyard or taking that long holiday to your favourite destination, it also brings with it the challenges of managing expenses with a more limited stream of income. This income gets even thinner when it is impacted by tax deductions. The good news is that Finance Minister (FM) recognized this fact.

In his 2018 Budget speech, he declared that caring for those who have cared for us is one of the “highest honors”. In keeping with this sentiment, increased tax benefits were introduced for senior citizens so that they have a higher post-tax income at their disposal. This article highlights some of those provisions.

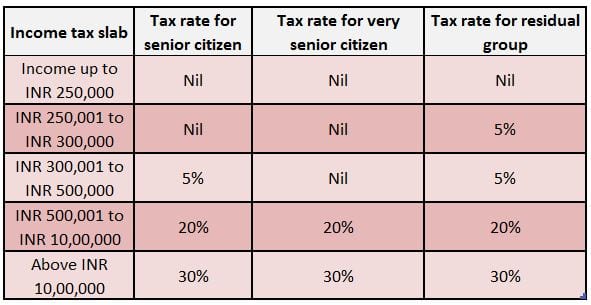

It is important to first be clear about who can qualify to avail of these benefits. Under the Income-tax Act, 1961 (the Act), there are two categories of senior citizens:

i. Senior citizen - an individual who is the age of 60 years or more but less than 80 years at any time during the FY

ii. Very senior citizen – an individual who is 80 years or more at any time during the FY

* Surcharge and Health and Education Cess (4%) as applicable. Surcharge is applicable as follows:

* Surcharge and Health and Education Cess (4%) as applicable. Surcharge is applicable as follows:

Total income of Rs 50 lakh up to Rs 1 crore - 10% of tax payable.

Total income exceeding Rs 1 crore - 15% of tax payable.

Apart from the higher threshold income as displayed above, there are other beneficial provisions too.

Tax concession on interest incomes earned from deposits

Interest income from fixed deposits, post office deposits, etc. is a major source of income for retired seniors, and usually this income is subject to tax. In the last Budget, a deduction of up to Rs 50,000 from such interest income was introduced for senior citizens. This is over and above the deduction of up to Rs 10,000 already available on savings bank account interest.

Furthermore, now banks are required to deduct TDS on such interest income only if it exceeds Rs 50,000 for the FY. If your total income is below the tax threshold, you can submit Form 15H to the banks seeking non-deduction of TDS for that FY.

Extended deduction for medical and other health-related expenses

With old age comes rising healthcare costs. Seniors can claim deduction of up to Rs 50,000 p.a. for medical expenses and/or health insurance premium. In case of specified critical diseases, an individual can claim a deduction of up to Rs 1 lakh for the medical expenditure for their dependent seniors.

Taxability of pension

Pension received in the form of annuity payments is taxable as salary income. After the renewed introduction of standard deduction last year, it has been clarified that standard deduction of Rs 40,000 will also be available on pension income.

Reduced burden of tax compliance

Even in terms of tax compliance processes, some provisions have been introduced to ease the burden on senior citizens. A senior does not have the obligation to pay ‘advance tax’ during the year. ‘Advance tax’ refers to the payment of tax liability in four instalments during the year on the estimated taxable income. Regular taxpayers are subjected to penal interest for failure to pay advance tax within the stipulated dates. Senior citizens not having business income are altogether exempted from advance tax. This helps them manage their cash flow better as they can pay self-assessment tax (SA tax) after computing the final tax liability for the FY.

SA tax can be paid at any time before filing the tax return and is paid via challan number 280. Nationalised banks facilitate the tax payment through their local branch or online. Details of the SA tax paid challan are required to be updated in the income tax return before filing.

Note that other provisions applicable to regular taxpayers continue to apply to senior citizens as well. Hence, taxability of rental income, capital gains, etc. and other sources of income should be well understood and followed. Similarly, a maximum deduction of Rs 1,50,000 is available under section 80C in respect of specified investments like 5-year fixed deposit, life insurance premium, etc.

Hence, if you are a senior citizen, ensure that your tax return has been prepared considering all of the above. With the financial year-end coming up soon, it may be a good time now to take stock of your tax liability for the year.

(The author is Partner – Personal Tax, PwC India. Komal Kotecha, Manager and Tanu Gupta, Associate at PwC India also contributed to this article.)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.