Borrowers can heave a sigh of relief as the Reserve Bank of India (RBI) decided to keep its policy repo rate hike unchanged at 6.5 percent in the first bi-monthly monetary policy review of FY24.

The Monetary Policy Committee (MPC) of the central bank has a taken pause on hiking the repo rate, contrary to industry expectations, while terming it ‘temporary’ and retaining its stance at ‘withdrawal of accommodation’ taking into account the turmoil caused by global banking crisis and the contagion risks.

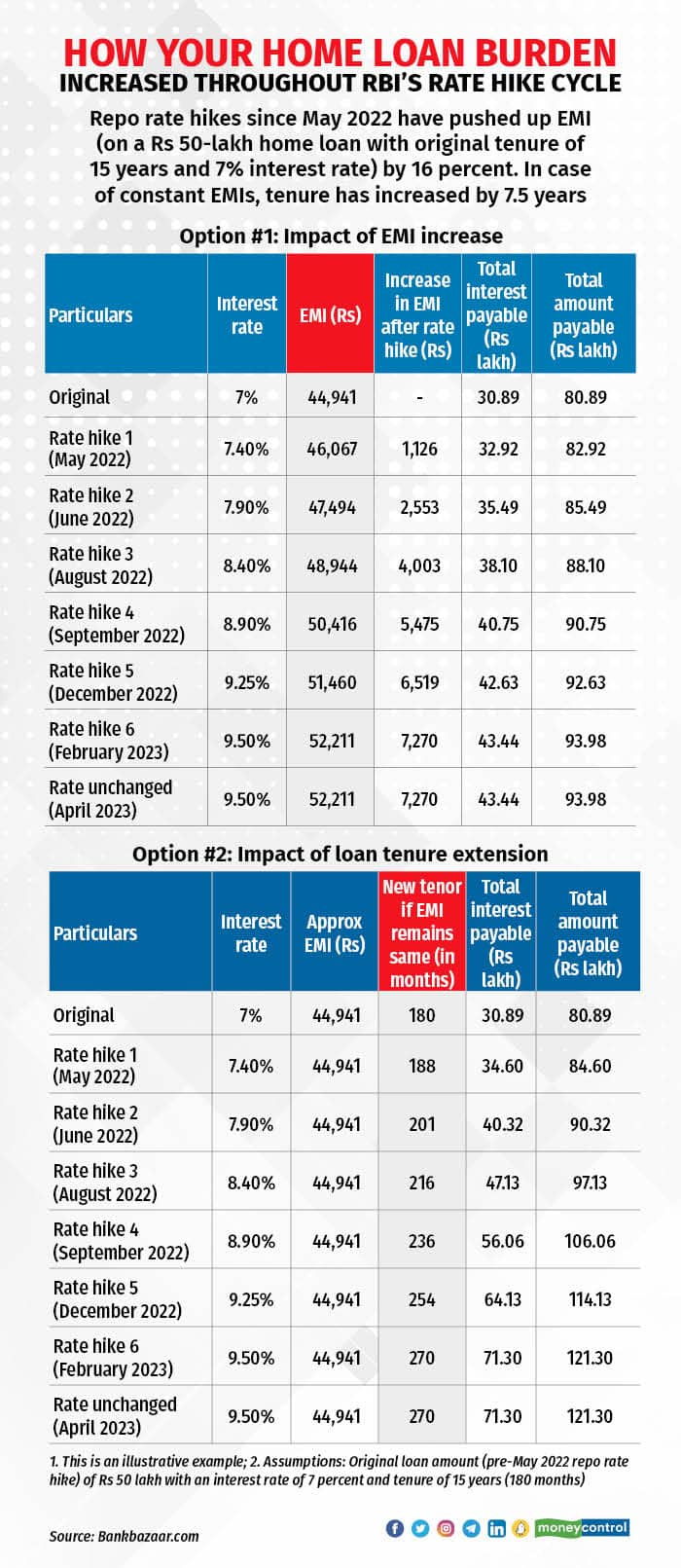

“Given that the RBI has hiked the repo rate by a total of 250 basis points (bps) since May 2022, which has caused home loan interest rates to rise to 9 percent and more, the stable repo rate is expected to provide some relief to homebuyers,” says Subhash Goel, director of Goel Ganga Developments.

Borrowers be cautious: RBI’s war on inflation not over yet“Reeling under the pressure of lengthening loan tenors and rising interest rates, this pause will help borrowers assess their current liabilities in the face of the 2.5 percent increase in the last one year, and help them devise strategies to optimise their overall interest outflow and tenor increases,” says Adhil Shetty, CEO, BankBazaar.com.

Nevertheless, the communication from the RBI during the policy announcement has highlighted that the battle to tame inflation is not yet over and the MPC will be ready to undertake further hikes if concerns on inflation increase. Suman Chowdhury, chief analytical officer, Acuité Ratings & Research, says, “The likelihood of a continued pause and a pivot to lower rates in the current year is still uncertain,” adding that the RBI has highlighted the potential risks of core inflation levels above 6 percent in the near term due to resilient domestic demand.

250 bps rate hike impact on borrowersIt is important to understand that a 250 bps repo rate hike in the last one year implies that EMIs have gone up by approximately 16 percent in the case of a 15-year loan, 20 percent in the case of a 20-year loan, and 26.5 percent in the case of a 30-year loan. “This will have an impact on the eligibility of borrowers and, hence, their purchasing power,” says Shetty.

He adds that for existing borrowers, this means higher EMIs or longer tenors and, in most cases, both. Many borrowers, especially those who have just taken out loans, have seen their tenors increase instead of decrease over the last one year despite timely repayments. Most banks have fully passed on the repo rate increase of 250 bps to home loan customers till date.

Back-of-the-envelope calculations show that if you had taken a home loan of Rs 50 lakh for a 15-year period, a rate hike of 250 bps will result in an increase of interest outgo by Rs 12.5 lakh, assuming you choose the option to increase the EMI. In the case of constant EMIs, the 15-years tenure has now extended by seven and a half years, i.e. to 22 and a half years (see graphic).

You could consider making part-prepayment of the loan out of your savings and investments rather than increasing EMIs. Long-term loans like those for housing allow this and in a rising interest rate environment, rethink your repayment strategy. Just an extra few thousand every month can reduce your interest payout over the long term.

“Prepaying your home loan as and when funds are available can do wonders and shorten your ballooning loan tenor,” says Shetty.

A good strategy is to earmark a portion of your annual bonus to prepay your housing loan every year.

Switch the lenderEven in a high interest rate scenario, there will always be opportunities to switch. According to a study by Bankbazaar, spreads on the benchmark rate have been falling over the last one year, from as high as 3.5 percent before the pandemic to 1.9 percent currently for new home loan borrowers. “So, if your loan is two to three years old, you stand to gain a substantial reduction on your interest rate on refinancing if you have a good repayment track record and credit score,” Shetty.

“You should actively look to switch even if the difference between the rates offered by existing and new lenders is just 35-50 basis points,” says Vipul Patel, founder, MortgageWorld, a loan consultancy firm.

Given the high interest scenario, your best option in such a case is to refinance at a lower rate and retain a higher EMI. This will help you keep down the costs of borrowing.

Opt to pay a higher EMIFinancial advisors suggest paying the higher EMIs as per your savings ability, as your loan gets paid off faster. Say you have a home loan of Rs 50 lakh, 20 years’ tenure (240 months) at an interest rate 9 percent and EMI of Rs 44, 986. Assume you can afford to pay an EMI of Rs 50,000; this home loan gets paid off in 186 months.

Also read: Looking for a new home loan? You may have to settle for a lower amount now

What should new home loan borrowers do?Those planning to avail home loans should not make their home purchase decision based on the policy rate changes. As home loans are typically long-term loans, a home loan borrower would witness several changes in the interest rate cycle during his or her loan tenure.

“Fresh home loan borrowers seeking higher liquidity can opt for the home saver option, a home loan variant branded by various lenders as Maxgain, Maxsaver, Home Advantage, etc,” says Naveen Kukreja, Co-founder and CEO, Paisabazaar. He adds that an overdraft account is opened for the home loan borrowers in the form of savings or current account, which can be used to park their surpluses and make withdrawals as per their financial requirements.

The interest component of their home loan account is calculated after deducting the account balance of the overdraft account from the outstanding home loan amount. Thus, availing the home interest saver option allows borrowers to derive the benefit of making prepayments while retaining their liquidity.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.