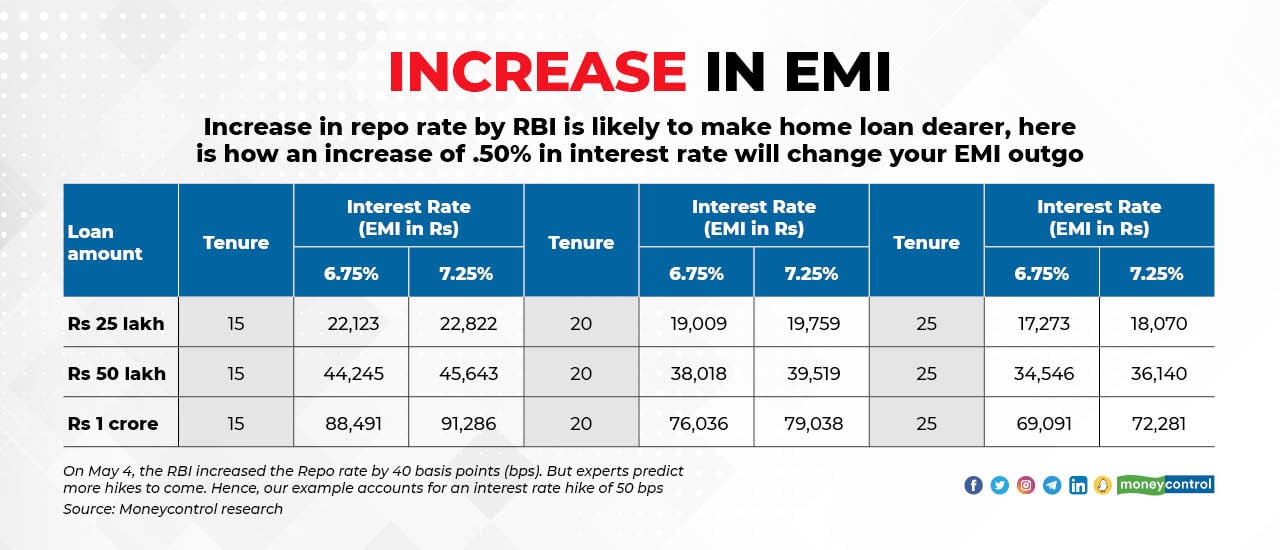

With the Reserve Bank of India (RBI) unexpectedly increasing the Repo rate by 40 basis points (100 basis points is equal to one percentage point) on May 4, when the next monetary policy meeting is just a month away, lenders are expected to increase the equated monthly instalments (EMI) of borrowers, a typical practice.

That’s a tough one, as inflation is also going up. Prices across the board from food to fuel are going up. If your monthly budget feels stretched, then here’s what you can do.

Also read | How the RBI 40 basis points REPO rate hike affects borrowers and depositorsIncrease in tenure Start by requesting the bank to increase the tenure of the loan, instead of the EMI. “The extension of tenure can offer a cushion when cash flow is strained,” says Arun Ramamurthy, Director – Andromeda Sales and Distribution.

“On a Rs 50 lakh loan for a 25-year term being serviced at 6.75%, the EMI will only increase to Rs 35,800 from Rs 34,500. But if the EMI is kept intact, the tenure will increase by 36 months,” says Vipul Patel, Managing Director and Founder, mortgageworld.in.

When interest rates are hiked, borrowers can either increase their loan-paying tenure or EMI

When interest rates are hiked, borrowers can either increase their loan-paying tenure or EMIA concern in increasing the tenure is that banks usually like their borrowers to be under the age of 65. If increasing the tenure means that you might be over the age of 65 and still have dues left, your bank might not like that. “Beyond the age of 65 years they won’t allow an increase in tenure and will automatically increase the EMI,” adds Patel.

But, there are more interest rate hikes on the anvil. “We expect three more rate hikes in this fiscal by the RBI now with the repo rate likely to end the year at 5.15 percent,” says HDFC Bank in its report “Stealing the Fed’s Thunder, RBI Hikes”.

Even if you are not affected by the 65-year age limit for the home loan term in the current rate hike, the next one would mean a steeper EMI burden.

Partial pre-payment To avoid feeling the pinch and offset the pressure from a higher EMI, you have the option of pre-paying your loan, at least partially. “Pre-pay at least a sum equivalent to the interest increase. So, if you have a Rs 1 crore loan, then prepay Rs 5 lakh to ensure that the interest payment is now outstanding only on Rs 95 lakh. There is a need to re-allocate resources from existing savings toward a home loan,” says Ramamurthy.

So, for instance, if you have any surplus amount or have received arrears thanks to a dearness allowance hike by the Government or received your annual bonus, then divert the same to the home loan pre-payment.

Also read | Juggling several loans? Here's how you must balance your debt repayment and liquidityHome loan savings account switch Lately, many lenders have been offering a home savings account or a home-plus loan account, which is a home loan with an attached overdraft account.

The advantage here is that you can park any kind of surplus funds in this overdraft account and the same is accounted toward the outstanding home loan and interest is applicable on the balance. The surplus can be withdrawn when there is a need.

So, if your outstanding is Rs 35 lakh and you have parked Rs 7 lakh in the overdraft account for, say, four months, then the bank will charge interest on Rs 28 lakh for those four months, thereby reducing the total interest outgo.

“If you have parked funds in a savings bank account or fixed deposit with the bank, then this overdraft facility attached to a home loan helps you benefit from the idle funds. You can use the funds in case of an emergency, but also save when you don’t need them,” says Ramamurthy.

If you have high liquidity in hand and have uneven cashflows, then opting for a home loan with a linked overdraft account helps you keep the interest rate burden low, says Gaurav Gupta, founder and CEO of MyLoanCare.

But before opting for the home loan savings / plus account, ascertain the interest rate, which can be higher than a normal home loan rate.

“There is a premium of up to 50 bps (0.5 percent) that banks charge for the home loan overdraft account. But many lenders do not charge anything over and above the usual home loan interest,” says Gupta.

Look before you switch lenders Switching to another lender when interest rates have been escalated is a natural move. But loan advisors suggest that this is futile. “When the repo rate has increased, the interest rate change will be effected across all lenders and there will be no benefit in moving to another lender,” asserts Gupta.

However, some borrowers who recently switched lenders now have restrictions placed on them. “Due to moratorium worries and for a low interest rate, a person switched to a public sector bank. Immediately, the bank increased the rates by 35 bps (0.35 percent) to 7.35%. Now, this same individual will have to pay 7.75 percent interest on his home loan. When she attempted yet another switch recently, she was told: ‘You should stay with the same lender for 16-24 months for us to ascertain that you have the repayment capacity,’” says Patel.

Restructuring If your salary cut post COVID-19 hasn’t yet been restored and you are still recovering from the after-effects of the moratorium ending (wherein your interest outgo increased), then it’s best to visit your bank branch. Have a chat with officials at your bank and request them to restructure the loan.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.