It’s that time of the year when you look forward to receiving your annual bonus.

While you decide how to spend this surplus amount, the big question for those paying equated monthly instalments (EMI) is: should I repay a part of my loan or invest the extra money?

The decision is difficult when you see that home loan rates are hovering at around 7 percent, while fixed income returns are around 5 percent.

The better option

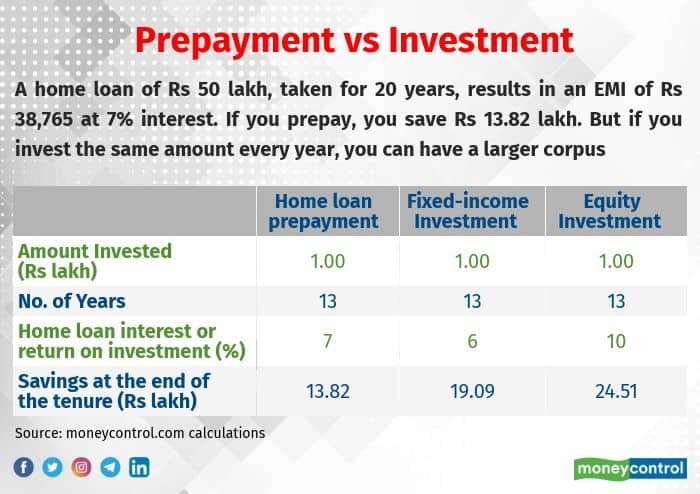

If you have a home loan of Rs 50 lakh, taken for a period of 20 years, at 7 percent interest, your EMI comes to Rs 38,765. So, you pay Rs 4.65 lakh each year towards your home loan.

Now, when you prepay any amount under the home loan, your principal outstanding – or the amount you owe to the bank – reduces. So, the overall interest that you pay during the entire loan term (on the reduced principal) also decreases.

Under normal circumstances, it takes you 20 years to clear this loan and your total interest outgo is Rs 43.03 lakh, if the interest rate continues to remain the same. But as we are toward the lower end of the interest cycle, the rates would increase during the term of the loan, fluctuating periodically.

Now if you make a partial prepayment of Rs 1 lakh in the first year, then this total interest payment would reduce to Rs 40.40 lakh, resulting in a saving of Rs 2.63 lakh. The loan term would decrease to 231 months from the original 240 months. This amount, however, if invested in an avenue earning 6 percent returns, would have resulted in a sum of Rs 1.03 lakh, fetching a little higher amount of Rs 1.05 lakh if it earned a return of 10 percent in the first year.

Prepayment of a loan, even though the interest rate is 7 percent, results in savings toward the start of the cycle.

If you continue to pre-pay a lump-sum of Rs 1 lakh at each loan anniversary, then you save about Rs 13.82 lakh over the tenure of the loan, which itself would reduce to 171 months due to the acceleration in repayment of the loan.

The same amount invested in fixed instruments each year could help you earn about Rs 19.09 lakh at 6 percent and Rs 24.51 lakh if invested in an instrument earning 10 percent returns over a period of 13 years, when the home loan would be completely repaid if we consider similar pre-payments.

Pre-payment when rates low

However, pre-paying the loan when interest rates are low helps you close your loans faster.

Gaurav Gupta, founder and CEO of MyLoanCare says: “When you repay your loans when interest rates are low, a higher amount gets diverted to repaying your principal. And your loan tenure reduces quickly.”

Penalties and the loss of tax benefits

At present, no partial prepayment charges are levied on floating rate home loans.

However, there are restrictions on the number of partial payments you can make in a year. The minimum partial prepayment amount is also decided by banks. Also, you can’t start pre-paying from the first month itself. Gupta says that typically banks do not allow prepayment during the first six months of a loan term.

You also lose out on the income-tax benefits that a home loan payment brings you. Apart from a tax deduction of Rs 1.5 lakh under Section 80 (C), a person in the 30 percent tax bracket can save Rs 60,000 worth of taxes through the interest deduction allowed on home loan.

What should borrowers do?

By pure mathematical calculation, it typically makes sense to invest the money in equities. Suresh Sadagopan, Founder of Ladder7 Financial Advisories says that an investment like equities that can earn 10-15 percent in the long run is preferred to pre-paying, say a home loan, where your rate of interest could be as low as 7 percent. “This loan doesn’t hurt you and banks aren’t coming after you to prepay,” he says. Using the extra bonus earnings to top-up your systematic investment plans through lump-sum payments can help you get closer to your financial goal, he adds, especially if you haven’t been saving up regularly thus far.

However, some types of loans are best repaid as fast as you could. D. Muthukrishnan, a Chennai-based certified financial planner says: “If you have a personal loan or credit card rollover, then you must repay. The costs of these type of loans are far higher; in the range of 11 percent and above.”

It's also easier to pre-pay your loans, if you must, via internet banking these days.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.