Your residence – whether owned, rented or leased out – can give you to a range of tax benefits. Be it interest paid and principal repaid on a housing loan or rent paid to your landlord, the Income Tax Act allows deductions and breaks under various sections. In the last few years, several tax incentives have been announced – and some withdrawn. Here’s your guide to the tax breaks on offer currently.

Home loan principal repaid

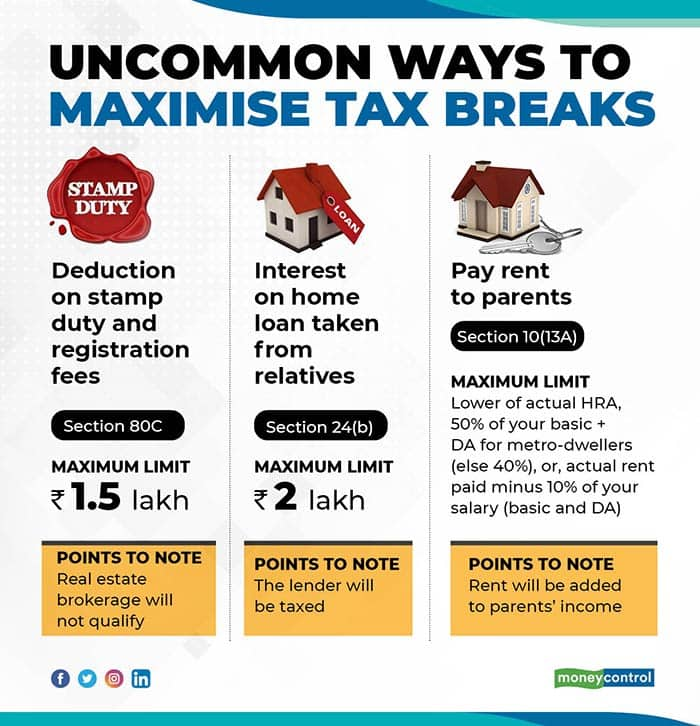

The most widely-known section, section 80C, allows tax-payers to claim deductions on a host of avenues, including on investments made in equity-linked saving schemes (ELSS), public provident fund (PPF), and also on life insurance premium paid among others. The overall limit is Rs 1.5 lakh. If you are in the process of repaying your home loan – taken to fund the construction or purchase of a house occupied by you – the principal repaid during the year is entitled for deduction.

In the initial years, the principal component is not sizeable and, hence, cannot help in completely exhausting the limit. It is possible that even after factoring in ongoing commitments including provident fund contribution, you will need to make additional investments to maximise the tax breaks.

Interest paid on housing loan

Just as you can claim deduction on principal repaid under section 80C, section 24(b) gives tax relief on interest paid during the year. This section allows deduction of up to Rs 2 lakh a year on interest paid on housing loan taken to finance a self-occupied house property. If you own two house properties and none of them are let out, both can qualify as self-occupied properties. This clause was brought about by an amendment announced in the interim Budget of 2019-20.

Now, the second house will not be subject to tax on deemed or notional basis if it is used as a family residence or remains vacant for the entire year due to, say, your employment at another location. However, if both have been financed by home loans, the total deduction under this section will be restricted to Rs 2 lakh a year. “Until this amendment was made, tax-payers were allowed to consider one property as self-occupied and the interest paid on the other property’s loan could be claimed as deduction separately,” explains Kuldip Kumar, Partner and Leader PwC India Global Mobility Practice.

The loss (tax relief) under such provision was limited to Rs 2 lakh a year, but the balance amount – to be set off against house property – could be carried forward for eight assessment years. “Now, this tax benefit can be claimed only if you actually let out the other house property. There is no option to treat the second house as ‘deemed to be let out,” he adds.

If your loan pertains to an under-construction property, you can take the tax relief on interest payment over five years, starting from the year in which the construction was completed. “If you have been paying pre-construction interest, it can also be claimed in five equal installments on a yearly basis,” says Archit Gupta, CEO and Founder, ClearTax. However, the maximum deduction is capped at Rs 2 lakh.

First-time home-buyer’s interest outgo

Union Budget 2016-17 allowed an additional deduction of up to Rs 50,000 to first-time home buyers whose loan was sanctioned between April 1, 2016 and March 31, 2017. The tax break, allowed under section 80EE, is applicable to houses whose value does not exceed Rs 50 lakh and the loan amount is under Rs 35 lakh. Union Budget 2019 introduced a section 80EEA that covers interest on housing loan taken between April 1, 2019 and March 31, 2020. This, too, pertains only to first-time home-buyers. The deduction limit under this section stands enhanced at Rs 1.5 lakh, while the value of the property is capped at Rs 45 lakh.

The perks of HRA

If you are entitled to house rent allowance (HRA) as part of your compensation, the amount is eligible for exemption under section 10(13A). The exemption will be the lower of the actual HRA received, 50 per cent of your basic salary and dearness allowance (DA) if you stay in a metropolitan city (else, it is 40 per cent), or actual rent paid minus 10 per cent of your salary (basic and DA). Even if your employer does not provide this allowance or you are self-employed, you can claim deduction on rent paid after making a declaration under Form 10BA. It will be restricted to Rs 5,000 a month, 25 per cent of income or excess of actual rent paid over 10 per cent of the total income, whichever is lower.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.