The Reserve Bank of India (RBI) has maintained the repo rate at 6.5 per cent for the 10th consecutive time in its bi-monthly Monetary Policy Committee (MPC) review meeting on Wednesday. The status quo means home loan interest rates and equated monthly installments (EMIs) will remain steady for borrowers, providing stability in their financial planning. By keeping the interest rate unchanged, the RBI aims to strike a balance between controlling inflation and promoting economic growth.

Since October 2019, banks have adopted an external benchmark system, predominantly pegging floating-rate retail loans to the repo rate. Consequently, changes in the repo rate have a direct and an immediate effect on the interest rates of these borrowings such as home loans. Borrowers benefit from rate cuts, while their interest burden increases in case of rate hikes.

Follow the latest updates on the RBI MPC right hereHigher rates may continue till DecemberThe consumer price index (CPI) inflation has stayed below the medium-term target of 4 per cent for two consecutive months. Inflation rose to a moderate 3.65 per cent in August from 3.6 per cent a month ago. The MPC, as some economists had predicted, has changed its stance from “withdrawal of accommodation” to “neutral” on Wednesday, marking a crucial shift in the approach it had adopted since May, 2022. "This means it is ready to act either way, depending on how things unfold. If inflation stays low, we may see rate cuts in the future. But for now, it's a wait-and-watch situation," says Adhil Shetty, Chief Executive Officer (CEO), BankBazaar.com.

Kanika Singh, Chief Risk Officer at the Indian Mortgage Guarantee Corporation (IMGC), expects a rate cut in December because of the improving inflation outlook in India and the global monetary easing cycle. “A minimum 25 basis points [bps] rate cut is expected,” she added.

Globally, central banks are easing interest rates. For instance, in September the US Federal Reserve eased interest rates by 50 bps. The European Central Bank (ECB), Switzerland, Sweden, Canada, Brazil, Peru, and China have also eased their monetary policy.

Benefits for existing borrowers as repo rate cut expected from DecemberAccording to Shetty, existing home loan borrowers can significantly benefit from repo rate cuts. To illustrate, consider a borrower who took a Rs 50 lakh home loan two years ago with an 8.65 per cent interest rate and a 20-year tenure. Initially, the total interest payable was Rs 55.28 lakh. However, with the 60 bps repo rate hike between October 2022 and February 2023, the effective interest rate rose to 9.25 per cent, increasing the interest payable to Rs 69.7 lakh and extending the loan tenure by another two years and eight months. Only 3 per cent of the principal had been repaid after two years.

However, a 25 bps rate cut in three tranches (i.e. 75 bps in total), starting from December, will reduce the effective interest rate to 8.5 per cent. The cut will bring the total interest payable back to Rs 55.9 lakh and restore the original loan tenure of 240 months. This demonstrates how a 75 bps cut over six months could largely offset the impact of previous rate hikes.

"The actual impact on home loan rates would largely depend on how quickly banks pass on the rate cuts to borrowers," says Atul Monga, CEO & Co-Founder, BASIC Home Loan. He adds that factors like credit demand and individual bank policies would also influence how swiftly the EMIs might reduce. Borrowers must stay informed about such developments to take advantage of potential savings on their home loans.

This year, HDFC Bank has effectively increased home loan rates for new borrowers by 40 bps, despite repo rates holding the line. One basis point is one-hundredth of a percentage point. At HDFC Bank, the lowest interest rate on a Rs 50-lakh home loan was 8.35 per cent in January. Now, the lowest interest rate is 8.75 per cent.

According to data on interest rates compiled by Paisabazaar, State Bank of India (SBI) and Bank of India (BoI) have raised their effective new home loan rates by 10 bps. In April, the lowest home loan rates at SBI and BoI for a Rs 50-lakh loan were 8.40 per cent and 8.30 per cent, respectively. From May, these rates went up to 8.50 per cent at SBI and 8.40 per cent at BoI.

Financial experts have attributed this effective home loan rates hike to liquidity constraints, which have affected not only HDFC Bank, but other banks as well.

With the rise in effective rates, borrowers have the option of switching to other lenders who offer narrower spreads and lower interest rates to save on interest costs, according to experts.

New home loan borrowers should look for banks offering loans with the narrowest possible spread to reduce the interest payable.

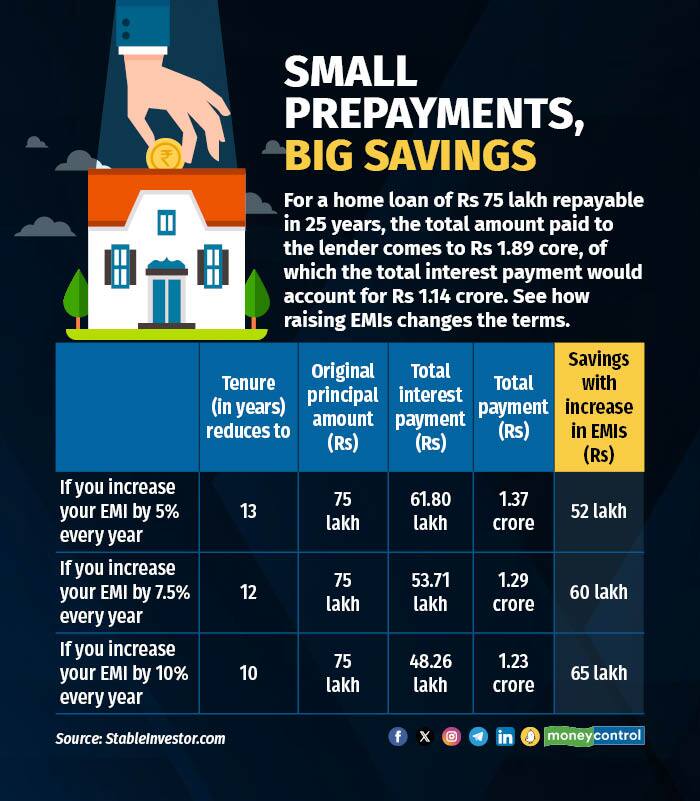

Also read | Lenders are cautious on higher NPA levels, but no alarm bells so far: Amit DiwanPrepay to lower interest burdenTo significantly reduce your home loan burden, consider making strategic partial prepayments that directly reduce the principal amount. By allocating a few thousand rupees extra each month from your savings and investments, you can substantially lower your interest payments over the loan tenure. This proactive approach may seem modest, but its long-term impact can be profound, saving you lakh of rupees in interest (see graphic).

Consider allocating a portion of your annual bonus towards prepaying your housing loan, making it a yearly habit.

There are opportunities to switch lenders in the current scenario, with several banks offering home loans, starting at 8.35 per cent.

Borrowers, who have a home loan linked to older benchmarks like marginal cost of funds-based lending rate (MCLR) or base rate, can switch lenders. It's essential to reassess your interest rate and other loan terms. You may be paying marginally higher interest rates, as compared to newer loans benchmarked against the repo rate. Opting for a loan transfer or switch could help you capitalise on lower interest rates offered by other lenders and reduce your interest burden.

Borrowers can significantly reduce their interest expenses by tracking market rates and negotiating with their existing lenders. This simple exercise can result in considerable savings. Although banks lack a formal conversion process, they may lower rates during negotiations, especially if borrowers indicate plans to switch. In contrast, Non-Banking Finance Companies (NBFCs)/Housing Finance Companies (HFCs) provide official conversion options, enabling borrowers to transition to lower rates for a fee.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.