The last of the four advance tax instalments for income earned in the current financial year 2020-21 falls on Monday, March 15. If you fail to do so, you might face needless penalty on the due taxes.

Advance Tax

The Income Tax law requires specified assessees to estimate their income, compute income-tax liability and pay taxes in four instalments during the course of the financial year. The assessees are usually not expected to pay taxes in one instalment.

As per the law, the taxpayers are required to pay annual estimated tax in instalments of 15 percent, 45 percent, 75 percent and 100 percent, on or before June 15, September 15, December 15 and March 15, respectively. It effectively means that they pay as they earn and at the same time the system ensures a steady flow of taxes to the exchequer.

Who needs to pay advance tax?

Every person, whose estimated tax liability for the financial year is Rs 10,000 or more, is required to pay advance tax. Advance tax, according to Neha Malhotra, Director, Nangia Andersen LLP, "applies to all taxpayers, salaried, freelancers, and businesses. However, a resident senior citizen (an individual of age 60 years or above), not having income from business or profession is not liable to pay advance tax."

A salaried person, who doesn’t have any income other than salary, need not pay advance tax instalments, as employers are required to deduct the applicable tax from monthly salary and pay to the department.

Penal interest for missing payments

Failure to pay correct advance tax on time or short payment of tax attract penal interest. “In case an assessee fails to pay advance tax on or before prescribed due dates or deposits an amount less than the stipulated percentage, he/she shall be liable to pay simple interest under section 234C at the rate of one percent per month or part of the month, on the amount of shortfall for the next three months,” said Malhotra.

For instance, if your tax liability would have been assessed on June 15, 2020, i.e. when the first instalment of advance tax become due as Rs 2 lakh for fiscal 2020-21, you should have paid Rs 30,000 (15 percent of Rs 2 lakh) as the first instalment of the advance tax.

If you had missed paying the entire amount, your total advance tax liability for the second instalment on September 15 would be Rs 90,000 (45 percent of Rs 2 lakh). Interest will be applicable one percent per month for three months i.e., April to June Rs 900, which shall be due along with self-assessment tax liability at the time of filing the return.

If you also failed to clear the second instalment of advance tax liability, your total advance tax liability for the third instalment would be Rs 1,50,000 (75 percent of Rs 2 lakh). Interest will be applicable one percent per month for three months i.e., July to September Rs 2,700 which shall be again due along with the filing of self-assessment tax liability.

If you have not paid any advance tax instalment to date, you should pay the entire Rs 2 lakh by coming to the fourth instalment on March 15. Interest will be applicable one percent per month for three months i.e., October to December Rs 4,500 which shall be due along with self-assessment tax liability.

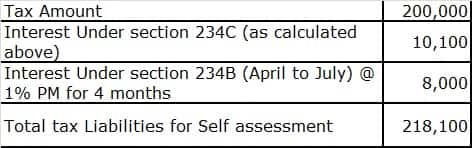

Further, if you fail to pay the final instalment of advance tax, the interest calculation will continue till you pay the due taxes. Interest will be applicable one percent per month for one month i.e., March Rs 2,000 which shall be due along with self-assessment tax liability.

While calculating final tax at the time of self-assessment, let’s assume the return filing date as July 31, 2021. You need to pay tax along with interest at the time of filing of return as mentioned below.

However, it may be mentioned that the interest will not be levied if the shortfall is within the specified range or in some other cases. “No interest shall be levied if the advance tax paid by the assessee, on or before the 15th day of June or the 15th day of September, is not less than 12 percent or 36 percent, of the tax due on the returned income, respectively,” said Malhotra.

In simple words, this means that if you pay a large chunk of your advance tax instalment- but not the full amount- then the interest penalty will not be imposed on you. For instance- and we told you so far- you are meant to pay advance tax of 15 percent of your annual estimated income by June 15. And 45 percent by September 15. However, if by June 15 you end up paying at least 12 percent (instead of the mandated 15 percent) or 36 percent on September 15 (instead of the mandated 45 percent), then no penalty will be imposed. The logic here is you have at least paid a large chunk of your advance tax liability.

Interest shall also not be charged if the shortfall is on account of under-estimation or failure to estimate (a) amount of capital gains (b) income in the nature of winnings from lotteries, etc. (c) business income in case where it accrues or arises under the said head for the first time, added Malhotra.

HOW TO PAY?

You can pay the advance tax offline as well as online. To pay it offline, use tax payment challans (challan no. 280) at bank branches authorised by the Income Tax Department. For paying it online, log on to the income tax department’s website, www.incometaxindia.gov.in, and click on e-Pay taxes. You will then be directed to the National Securities Depository Ltd (NSDL) website. Click on challan number 280, fill in the required details and make the payment.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.