T. Srikanth Bhagavat

The term ‘financial independence’ simply means that you have sufficient savings to live your life as you please. To some, it simply means retirement from work at the age of 58 and spending time with their families. For a few others, it is about pursuing their passions, without having to worry about the money. So, it can be time spent with NGOs or chasing a hobby, or even converting a hobby to a profession. Still others may want to continue working, but on their own terms.

To live such a life without having to worry about how your needs are going to be met, or rather with the knowledge that your needs will be satisfied comfortably is financial independence.

How does one reach such a state of bliss? There are financial and spiritual angles to it.

Getting to the financially blissful state

It is important to be debt-free. Having to pay EMIs when your income stops is like retiring with a millstone around your neck. By no stretch can you call it independence. Plan your independence day such that you repay your debts by then. A lot of forethought goes into spending only as much as you can afford. Hence, the need to borrow would be limited.

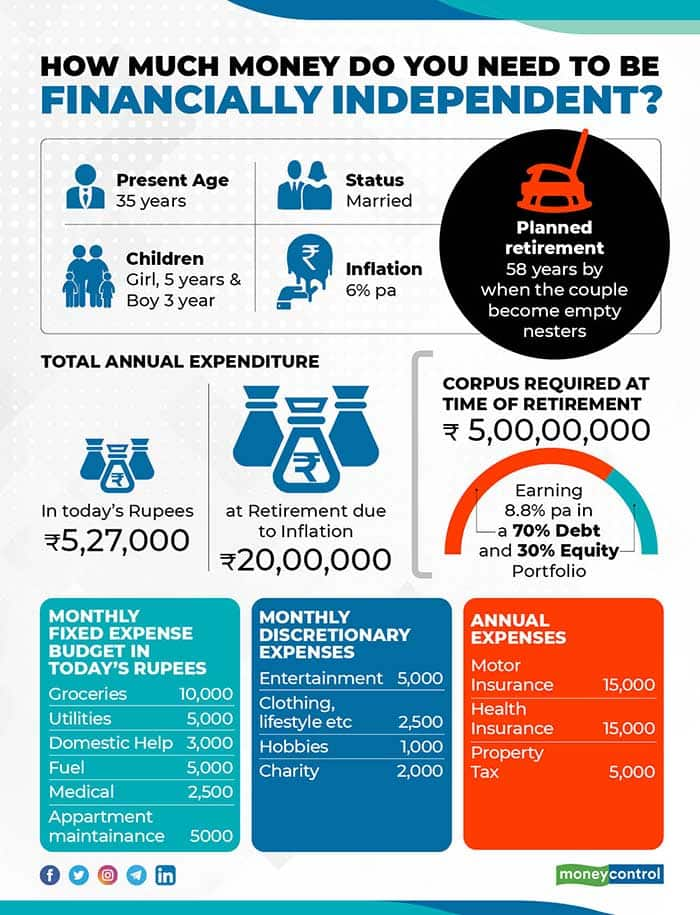

You have to build a retirement nest egg that can sustain your expenses through the rest of your life and your partner’s. This is a complex topic by itself, but the principles that determine the size of the corpus are your spending pattern, the rate of inflation and the manner in which you invest those savings when you retire, and the number of years that you want the corpus to last. An illustration is included here.

Apart from your normal living expenses, you need to plan for a few other costs.

Family needs: If your children or any other family members remain dependent on you into adulthood or are yet to finish their education, then this corpus needs is to be accumulated separately.

Emergency corpus: Set apart some funds to draw on in case of an emergency – medical or otherwise – regardless of how much insurance you possess.

Holiday fund: You plan to travel till your last breath. Great. Just ensure that you have a separate fund for it. The size depends on whether your travels are domestic or international; luxury or budget. Fix the frequency of trips. This amount should be kept separate so that its depletion does not affect your day-to-day living.

Maintenance fund: You need to regularly repair, renovate, repaint the house, and refurnish it too.

Depreciation fund: You may want to change cars periodically, replace home equipment, computers, phones etc. Unknowingly, you may end up spending a lot on such things. It is better to plan for those purchases.

When estimating your post-retirement expenses, do not forget to factor in cultural needs such as gifting. I remind many to factor in giving (charity) as well. So is the case with the cost of pursuing your hobbies. If you want to pursue any kind of entrepreneurial dream, build a corpus for it, so that such that the venture’s success or failure does not impact the security of your retirement.

Finally, increase allocation for medical expenses as you get older.

These lists can go on endlessly. Longer the list, the tougher the plan. Tougher the plan, the longer the time you need to accumulate the corpus. Longer the time needed, the more the sacrifices you need to make now. All this begs the question, what then is the real secret to financial independence? It is actually “contentment.” Contentment comes out of limiting your desires and living a minimalistic life (not necessarily that of a monk!). But think like a monk. This kind of thinking results in less baggage for you to manage through your life. Striking that balance between need and want is the prime determinant of your financial independence. It will eventually impact your work-life balance, which has surprising results on the need for premature retirement also! This is the spiritual angle to financial independence that in my view is as important as the financial angle.

(The writer is the Managing Director, Hexagon Capital Advisors, A Registered Investment Advisor)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.