With rising awareness and greater regulatory oversight, more investors are considering bonds as reliable tools for stable and predictable returns.

The growing interest recently prompted the Securities and Exchange Board of India (SEBI) to advise investors to avoid unregistered online bond platforms, offering investment services without the required regulatory approval.

Why retail investors prefer bonds?

Retail investors are turning to bonds for two reasons. “Many people today want steady monthly income due to job changes or the need for predictable cash flow. Bonds provide that stability very well. They also offer meaningful diversification,” said Saurabh Bansal, Founder, Finatwork Investment Advisor, a SEBI RIA (registered investment adviser).

Another reason is higher yields and easier access through digital platforms. This trend has accelerated, as bond returns now surpass those of fixed deposits (FDs) and provide competitive alternatives to debt mutual funds.

“Typically, top-rated corporate and government bonds deliver returns in the range of 7–9 percent, while select high-yield NBFC (non-banking finance company) bonds may offer as much as 10–12 percent. In contrast, FDs generally yield 5–6 percent,” says Prashant Mishra Founder and CEO, Agnam Advisors.

The combination of rising financial literacy and user-friendly digital platforms has made bond investments more accessible and transparent, attracting a broader segment of younger and tech-savvy investors.

Bonds also offer tax advantages, stable and predictable income streams, and lower volatility compared to equity markets, making them especially appealing for conservative investors and retirees.

Popular bonds on digital platforms

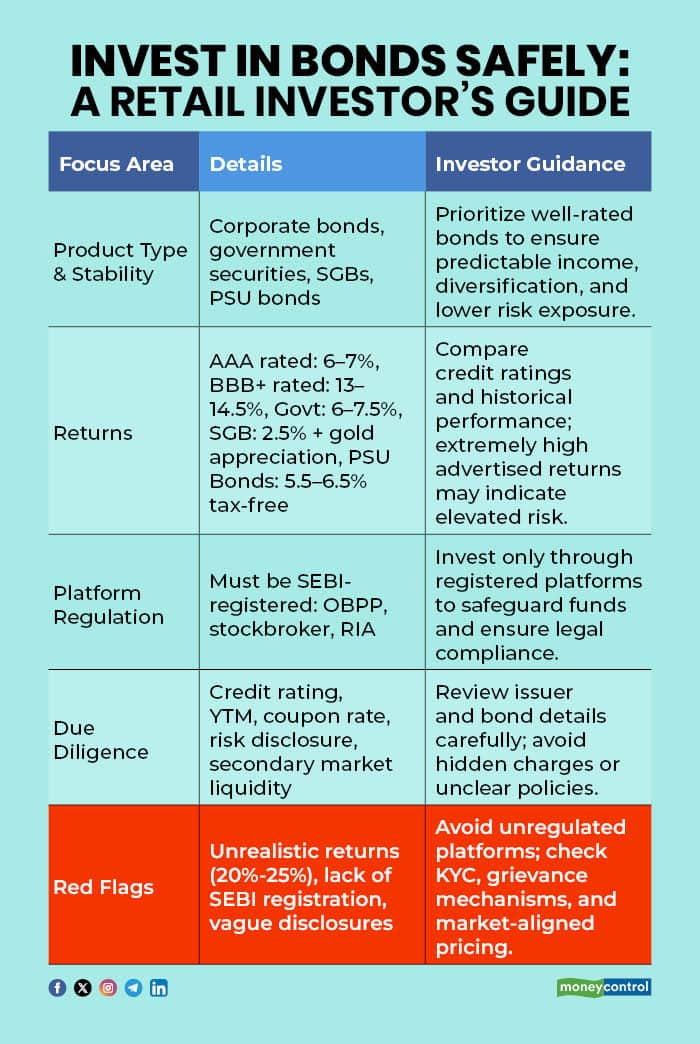

Most digital bond platforms primarily offer listed corporate bonds, largely from NBFCs along with government securities. Returns vary based on the credit rating of the bond.

“AAA-rated bonds typically offer around 6–7 percent. BBB+-rated bonds can offer anywhere from 13 percent to even 14.5 percent. Most platforms avoid hosting C or D rated bonds because of the extremely high default risk and to protect investors from potential losses,” said Vishwajeet Goel, head , Pensionbazaar, an online retirement planning platform.

Government securities generally offer 6–7.5 percent over the long term, while PSU bonds generally provide 5.5–6.5 percent tax-free interest.

Check credit ratings and yields

Do remember that returns that are advertised by a bond app have to be realistic because it’s a regulated product and SEBI defines a certain nomenclature for how returns must be shown.

For example, there is a concept called YTM, or yield to maturity, which typically acts as the ROI substitute - rate of interest, or return on investment substitute.

“When assessing bond investment opportunities on an app, investors should carefully review the credit rating of the issuer, the quoted yield to maturity (YTM), and the coupon rate. Any advertised yield above 12 percent warrants caution, as it may signal either elevated risk or unrealistic projections,” Mishra said.

Reliable digital bond platforms share detailed information on issuers, ratings, risk profiles, and settlement procedures. Warning signs of possible misrepresentation include hidden charges, vague risk disclosures, and lack of secondary market liquidity. Investors should ensure the platform’s pricing and redemption policies align with prevailing market conditions for bonds with similar ratings, say experts.

“If the app shows extremely high returns, such as twenty or twenty-five percent, that is a clear warning sign. A strong issuer would not need to borrow at such high rates,” Bansak said.

SEBI licensing and investor protection

A bond platform must have SEBI registrations such as an Online Bond Platform Provider (OBPP), stockbroker registration, and RIA registration.

“These registrations ensure that all transactions take place through regulated channels, safeguard investors even if the platform shuts down, and reduce the risk of mis-selling when promised returns are not delivered,” said Swapnil Aggarwal, director, VSRK Capital.

Red flags and risk mitigation

Retail investors should watch out for: promise of abnormally high returns without credible issuer or rating information; inadequate disclosure on risks, pricing, or settlement; lack of SEBI or exchange registration. Absence of proper KYC procedures or grievance redressal mechanisms, misleading statements such as “guaranteed returns” that exceed market norms or platforms that obscure fees and settlement details, too, are red flags.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.