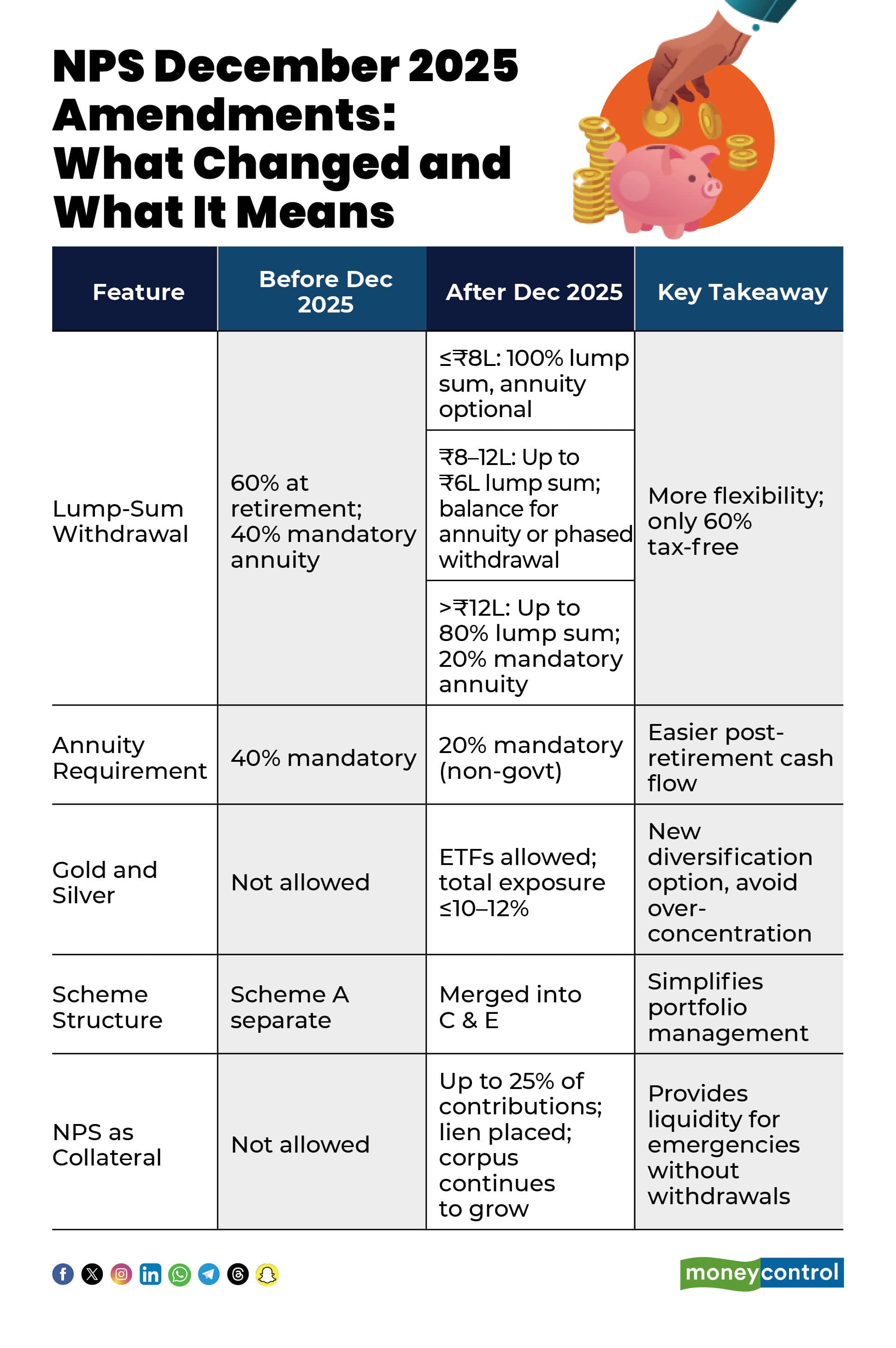

The December 2025 NPS overhaul brings a new era of flexibility and control for retirement planning. Subscribers can now withdraw a larger portion of their corpus as a lump sum, while a smaller fraction is mandatorily used to buy an annuity, helping secure inflation-adjusted income. Gold and silver ETFs are introduced, alternative assets are merged into equity and corporate bond schemes, and the NPS corpus can now serve as collateral for loans.

These changes give investors more tools to manage emergencies, diversify portfolios, and plan withdrawals strategically. However, careful planning is crucial, as using NPS wisely ensures your long-term retirement sustainability.

NPS 80% Lump-Sum Withdrawal: Tax Ambiguity

Under the new NPS rules for non-government subscribers, the withdrawal options vary depending on the total accumulated pension wealth. If your corpus is up to Rs 8 lakh, you can withdraw the entire amount as a lump sum, and purchasing an annuity is optional.

For a corpus between Rs 8 lakh and Rs 12 lakh, you can take up to Rs 6 lakh as a lump sum, while the remaining amount can either be used to buy an annuity or withdrawn gradually over at least six years. If your corpus exceeds Rs 12 lakh, you can withdraw up to 80 percent as a lump sum, with the remaining 20 percent required to be invested in a mandatory annuity through a registered annuity service provider.

The December amendments also extend the investment age to 85. However, the 80 percent withdrawal rule has created a critical tax ambiguity. Under the current Income Tax Act, Section 10(12A) provides tax exemption specifically for up to 60 percent of accumulated corpus at normal retirement (age 60+).

The remaining 40 percent must be mandatorily annuitized, and the annuity income is taxable. “The recent amendment allows withdrawal of 80 percent as lump sum instead of the previous 60 percent, with only 20 percent mandatorily annuitized. However, the Income Tax Act has not been amended to extend the tax exemption from 60 percent to 80 percent,” says Krishna.

Until the Govt amends the tax law only 60 percent of the NPS corpus is tax-free and the additional 20 percent allowed during retirement under new rules is taxable as per one’s income tax slab. So the entire 80 percent of NPS corpus is not automatically tax free as currently only the first 60 percent gets tax exemption.

“Withdrawing the balance 20 percent by spreading the withdrawals across multiple years one can reduce their overall tax liability if including this withdrawal from NPS puts them in the lower tax brackets during that financial year,” says Kumar.

20% Annuity Rule Reshapes Retirement Planning

This December 2025 NPS rule change allowing 80 percent withdrawal while mandating only 20 percent annuity purchase fundamentally shifts retirement planning strategy. This flexibility requires disciplined analysis to ensure the 20 percent annuity provides sufficient inflation-adjusted income.

“The monthly pension from a 20 percent annuity depends on three variables: the corpus size, annuity rate, and annuity type selected. Current annuity rates range between 5.5 percent to 7.5 percent across different Annuity Service Providers (ASPs) and plan types,” says Madhupam Krishna, Securities and Exchange Board of India (Sebi) registered investment advisor (RIA) and chief planner, WealthWisher Financial Planner and Advisors.

The 80 percent lump sum, therefore, plays a crucial role. It can be invested across a mix of debt, hybrid, and equity mutual funds, depending on risk tolerance, to generate a steady cash flow while allowing the corpus to grow.

“This approach helps support a long post-retirement phase, often spanning 20 to 30 years, and improves the chances of the overall retirement pool keeping pace with inflation,” says Saurabh Bansal, Founder, Finatwork Investment Advisor, a SEBI RIA (Registered Investment Advisor.

You need to determine your inflation-adjusted expense target. This is the critical step, as your retirement expenses today will differ significantly from expenses at retirement age due to inflation. You can calculate it using the simple inflation calculators via internet. If you not very much in numbers you can go for thumb rules like normally retirement expenses are 70-75 percent of pre-retirement income (excluding work-related costs, retirement savings, transportation).

So, if your current gross income is Rs 10 lakh monthly, your retirement spending baseline should be approximately Rs 7 lakh to Rs 7.5 lakh in today's rupees, adjusted forward by inflation.

“This figure also needs to be adjusted with inflation during retirement. For example, suppose you get Rs 50,000 as monthly pension but after 20 years this will be not be sufficient as inflation will reduce the purchasing power of this pension amount,” says Krishna. That is why fixed pensions or problematic if not adjusted with inflation.

“So based on their current expenses, expected inflation during retirement and their life expectancy they should estimate the additional amount that they would require and then set up a system to withdraw the additional amount using systematic withdrawal plan require over their lifetime to manage their expenses,” says Abhishek Kumar, a Securities and Exchange Board of India (Sebi)-registered investment advisor (RIA), and founder and chief investment advisor of SahajMoney, a financial planning firm.

NPS Gold and Silver ETFs: Watch 10–12 percent Limit

The December 10, 2025 PFRDA Master Circular has introduced gold and silver ETF exposure for NPS subscribers, but this new option creates a critical portfolio risk when combined with existing physical gold or Sovereign Gold Bond (SGB) holdings. The apparent diversification across multiple products masks a fundamental concentration problem that all three forms, track the same underlying commodity and move in near-perfect lockstep.

“This high correlation violates a foundational principle of portfolio diversification which is “true diversification requires holdings with low or negative correlation. Holding multiple forms of the same commodity across different accounts creates just the illusion of diversification while portfolio is concentrated on a single-asset bet,” says Krishna.

Now if someone has invested 8.5% in gold via NPS, he may think it is optimal. But we all know, Indian households hold significant unmeasured physical gold (ancestral jewelry, hidden savings, ornaments), which could push total gold exposure to 12-15% or beyond, entering the diminishing-returns zone.

As a rule of thumb, keep total gold exposure, including NPS ETFs, SGBs, and physical gold, within 10–12 percent of your overall portfolio to avoid unintended concentration risk. The same with silver.

Also, PFRDA has merged NPS Tier I Scheme A (alternative assets) into Schemes C (corporate bonds) and E (equities). Now, instead of a separate bucket, these assets blend directly into your bond or stock choices. This cuts complexity, no more juggling extra schemes. Your portfolio auto-adjusts for better diversification, with easier switches (one free by Dec 25, 2025).

NPS Corpus Can Now Secure Loans

Now, NPS subscribers can now use their accumulated NPS corpus as collateral to raise loans from eligible lenders. Subscribers can pledge up to 25 percent of their contributions to a regulated financial institution.

The lender places a lien on the pension account as security for the loan. The money stays invested in the NPS and continues to earn returns. The loan must be used to pay off financial obligations with the lender. Once the loan is fully repaid, the lien is removed, and the subscriber has full control of their account again.

This means investors do not need to prematurely exit or partially withdraw from NPS to meet short-term liquidity needs such as medical emergencies, education, or major personal expenses.

However, Kumar warns that NPS should be used as loan collateral very judiciously, so that it does not materially impact your long-term retirement corpus. It works best for rare, once-in-a-lifetime needs or genuine emergencies not discretionary spending because money taken out may never fully find its way back into the system.

“If you are unable to service or repay the loan, it directly puts your retirement sustainability at risk. That is why borrowing against NPS should remain an exception, used only when all other avenues are exhausted, and never become a habitual source of funding,” he adds.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.