Madhuchanda DeyMoneycontrol Research

Yes Bank’s strong operational performance for the December quarter should for now allay concerns over asset quality divergence flagged by the RBI audit. Well-capitalised after the latest round of fund raising, Yes Bank is gaining market share, building a strong deposit franchise, and increasing exposure to better quality corporate and retail assets.

Valued at 2.9X FY19 book, Yes Bank has a strong earnings growth trajectory ahead. But for the stock to get re-rated, Yes Bank would require a more balanced asset mix (in favour of retail) and “a clean chit from RBI” in the next audit.

Strong performance

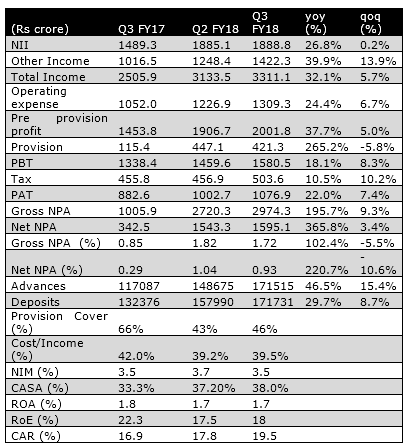

Profit-after-tax grew 22 percent and pre-provision profit, 38 percent. Growth in net interest income (difference between interest income and interest expenses) at 26.8 percent was helped by a stable net interest margin at 3.5 percent and robust 46.5 percent growth in advances.

The non-interest income growth too was a healthy 40 percent driven by a big increase in core fees. Provisions jumped sharply as the bank may have created additional buffer against SR (security receipts against assets sold to Asset Reconstruction Companies) and taken steps towards having a provision cover of 60 percent in the next couple of years. While cost was well-contained, the bank targets to achieve a much better cost to income ratio in the future.

The 20 basis points sequential reduction in interest margin was attributed to the bank raising Rs 9,415 crore quasi capital (including Tier II bonds) that are much costlier than the bank’s overall cost of funds (nevertheless improved its capital adequacy). Part of the decline was also attributed to Security Receipts. Net Security Receipts (SRs) for Yes stood at 1.06 percent of gross advances with a net increase in the quarter of Rs 421.9 Crores.

Business showing traction

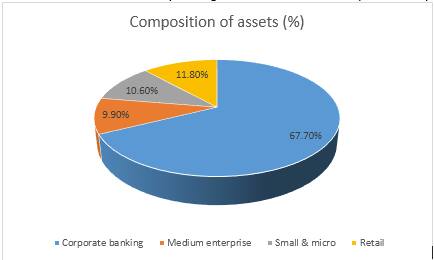

The bank has been aggressive in capturing market share. Advances rose 46.5 percent and Yes Bank now has close to 7 percent share in incremental advances. Going forward, the focus would be on improving the share of non-corporate, especially retail.

The bank has been able to compete in the market, thanks to the low-cost liability profile it is building up steadily. While overall deposits grew by 29.7 percent, the low-cost CASA (Current & Savings account) deposits grew by 48 percent and constitute 38 percent of total deposits. The bank has close to 9.5 percent share in the incremental deposits of the system. The bank is eyeing CASA ratio of 40 percent before September 2018.

Confident of achieving 4 percent interest margin

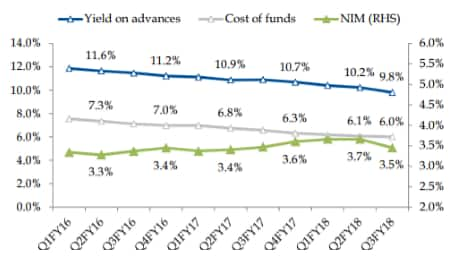

Thanks to the strength of the low-cost liability, Yes Bank has been able to maintain stable margins even as stiff competition has been eroding yield on advances.

The bank is eyeing 4 percent net interest margin as it takes the low-cost deposits share to a formidable level of 40 percent. This is all the more helpful, especially in a rising rate environment. Since the bank offers close to 6 percent on its savings account (compared to 3.5 percent of most banks) there is headroom to reduce costs there. Finally, Yes Bank expects to earn better as it originates more of its own priority sector lending (PSL) loans than the predominant buyout that it had done in the past.

Asset quality – awaiting the clean chit?

The bank has embarked on a journey to incrementally de-risk its book which is also reflected in the falling lending yield. Over 75 percent of the corporate portfolio is now rated “A” or above with a well-diversified sectoral composition.

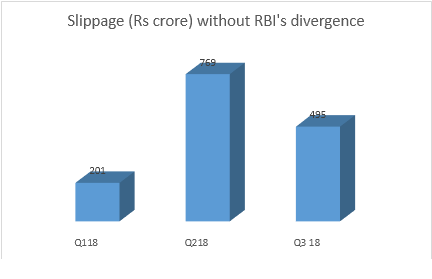

While the reported NPL (non-performing loan) picture looks better in the quarter, we would like to monitor the slippage closely as that number has not fallen significantly.

In the quarter, out of the total slippage of Rs 495 crore - Rs 245.4 crores was from accounts previously classified under ‘SDR’, ‘5:25’ and ‘NCLT’ categories.

A recap on divergence

Riding on the strength of its superior loan structuring skills, the bank had only taken a small quantum (Rs 1219 crore) of the latest round of divergence of Rs 6355 crore into gross NPA in the last quarter.

Close to 47 percent (Rs 2977 crore) of the divergence had been classified as standard assets by the bank. In this quarter, Yes Bank reported nil slippage into NPA for accounts classified as ‘Standard’ with significant principal loan repayments and with no interest overdue.

If we were to monitor all known troubled exposure (under various dispensation like restructured, SDR etc., outstanding SR and RBI divergence classified as standard assets) the quantum is close to Rs 5500 crore – 3.2 percent of advances. With the incremental better quality of growth, the problem, therefore isn’t going to impact financial performance meaningfully. However, to establish credibility of its numbers, the clean chit from RBI is important.

While we do see provision remaining elevated especially as the bank has set a target to achieve 60 percent cover within the next few quarters, the earnings momentum should enable the same.

The next round of inspection is for FY18 (which is at least a good 9 months from now). We do not see any imminent near term uncertainty. The bank is well-capitalised (Capital adequacy of 19.5 percent), steadily capturing market share in advances and building a solid low-cost liability franchise.

With the systemic NPL resolution moving into high gear, we are staring at an end of the bad asset cycle. The recapitalisation of PSU banks and resolution of bad assets should pave the way for recovery of the capex cycle that stands to benefit most corporate lenders including Yes Bank. The bank has already guided to a strong momentum. Hence at 2.9X FY19 book Yes Bank will remain a candidate to look at for its long road to profitable growth ahead.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.