Krishna KarwaMoneycontrol Research

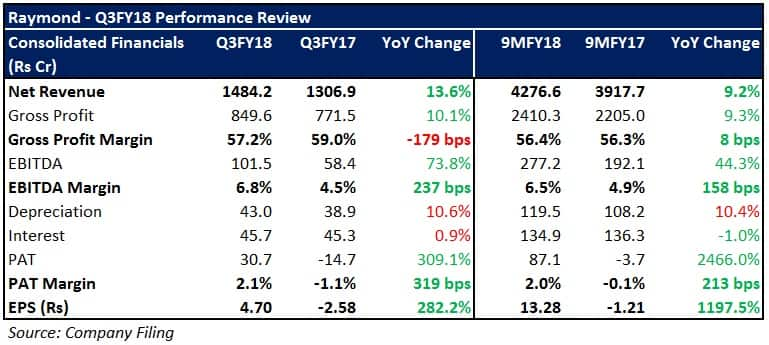

Raymond (market cap of Rs 6,608.5 crore) reported a good set of numbers in Q3FY18.

While the low base (demonetisation in Q3FY16) had a big role to play, top-line traction across all segments, lower ad spends, and operational efficiencies were the primary drivers for the visibly better performance in the quarter gone by.

Raymond’s branded fabric division witnessed growth owing to a seasonally strong Q3 (onset of the wedding phase). Early commencement of the end of season sale period in Q3, and store additions helped the company’s branded apparel division to do well.

Higher offtake by customers, lower cotton costs, and a tweak in product mix enabled Raymond’s shirting fabric segment to garner higher revenues. The company’s garmenting segment grew due to favourable demand from North America, but currency changes and initial set-up costs in Ethiopia impacted margins.

The auto component division grew on the back of a positive order book from clients and higher export realisations. The turnaround strategy adopted for the tools and hardware division resulted in cost optimisation, whereas growth in the operating income was driven by orders from Asia and Africa.

The outlook going ahead?

Network expansion

Raymond added 34 outlets (including 17 mini ‘The Raymond Shop’ stores and 11 exclusive brand outlets) and closed 15 in Q3, taking the total count to 1161 stores. Going forward, in a bid to keep the business model asset-light, 70-80 percent of the company’s new outlets will be run by franchise partners.

Sentiment recovery

Resumption of normalcy in trade channels and an uptick in consumer demand suggest the GST-induced disruptions seem to be fading gradually. Despite a weak start to Q4FY18, continuation of the end of season sale and marriage-related sales will put things back on track.

Capex

Raymond envisages capital outflows to the tune of Rs 90-100 crore in Q4, the utilisation of which will take place as under:-

For FY18, the company has guided for capex amounting to approximately Rs 370-400 crore with an objective to boost the top-line and ensure that investments in manufacturing facilities yield incremental returns. The effect of these initiatives on the financials could be visible from early FY19.

Fabric impetus

Raymond is anticipated to lay more emphasis on increasing the volumes and realisations (through marketing campaigns and introduction of premium variants) of its branded fabrics division. Consequently, the segment’s EBITDA margins are expected to improve from 14-15 percent to 18-20 percent by FY20 end.

What should an investor do?

Raymond, by virtue of the points stated above, targets achieving high single-digit EBITDA margins and becoming a positive cash flow company in the next two fiscals. Prospects of a few segments (branded fabric, shirting fabric, auto components, tools and hardware) appear fairly promising.

However, significant improvement in future earnings will largely hinge on the manner in which the company’s branded apparel and garmenting divisions (jointly contribute roughly 30 percent to the consolidated turnover) perform in due course.

A steep rally in recent months has caused the stock to re-rate. At 27.4x FY20 projected earnings, Raymond's valuation seems to be pricing in most of the tailwinds. Therefore, gradual accumulation is recommended.

For more research articles, visit our Moneycontrol Research Page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.