P/E is 24.25x while industry P/E is 37.34x.")

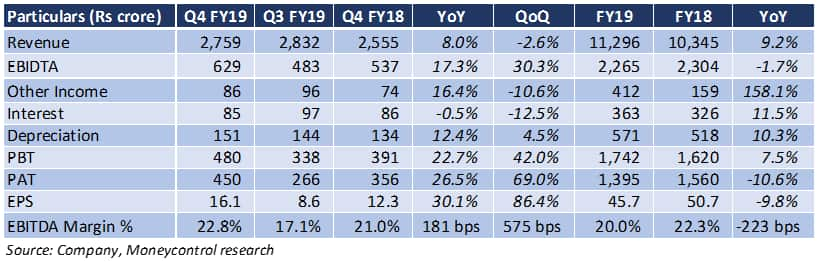

Tata Chemicals (TTCH) has some spring in its step. After several lacklustre quarters, it finally churned out a healthy set of earnings, signalling improvement across segments in the March quarter.

Improved realisation and currency gains made this possible. However, Europe offered a jarring note and volumes remained under pressure across geographies.

Key positives

- Consolidated revenue saw a healthy eight percent year-on-year (YoY) jump, driven by improved realisations across geographies

- Consolidated soda ash revenue was up 13.5 percent on the back of improved realisations

- While margin in the basic chemistry segment saw a healthy growth, specialty chemicals came under pressure

- Revenue from consumer products business saw good traction, chiefly because of higher sales volumes across categories and controlled marketing investments during the quarter gone by

- The company has forayed into non-food products like detergents, which are in the pilot phase and receiving a positive response from the market

- With supply tightness in the domestic market, the company was able to pass on higher power and plant fixed costs, partially protecting its margin

- Improved realisation and currency gains led to improvement in the North American business. However, a six percent YoY decline in volumes offset some of the gains. Performance in 2019 took a hit from power outage and maintenance issues, which the management expects to overcome in the coming year

- Kenya business reported a healthy quarter with increasing operational efficiency, lower fixed costs and higher realisations. However, high fuel costs knocked off a chunk of the profit

Key negative

- Despite higher realisations, performance in Europe strained due to high energy and fixed plant costs. Discontinuation of the low-margin trading business in Europe led to noticeable contraction in volumes from the region

- Rallis (a subsidiary of Tata Chemicals) reported a disappointing quarter with a substantial contraction in profits and margin despite a uptick in revenue. Overhang of high input costs cast a shadow profitability for yet another quarter

Other takeaways

- The management is planning a capex of $370 million towards capacity expansion at its Mithapur facility to ramp up soda-ash capacity by about 200,000 metric tonne, salt production by 400,000 metric tonne, and a portion for upgrading turbines to reduce its carbon footprint

- The Nellore plant for nutraceuticals is in the final stage of commissioning. The plant will go through a pilot stage and the company is targeting commercial production by December-end

- The company announced plans to foray into three segments: Lithium ion business, majorly manufacturing, recycling and chemical coating of batteries. The management expects final production and supply to begin from 2021-22, but stressed that the same would be dependent on commercial orders

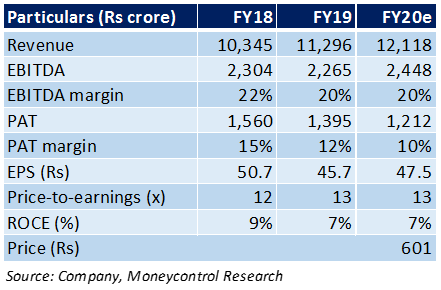

OutlookThe management indicated confidence in the strength of soda ash prices in coming quarters. Moreover, the consumer business is picking up pace. Capacity expansion in soda and salt are expected to drive growth in 2021.

At an estimated FY20 price-to-earnings of 13 times, the stock is trading close to its 52-week low and has seen a noticeable uptick after the result. Stabilisation post one-offs across geographies would be something to watch out for. A successful deployment of capital in high margin businesses can improve earnings and trigger a re-rating for the stock.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.