Neha Dave

Moneycontrol Research

- IndoStar Capital Finance is transforming from a wholesale financier to a diversified lender

- Diversification strategy to gradually push-up operating cost

- Asset quality has been resilient so far but remains vulnerable

- More-than-adequate capital and comfortable liquidity are key differentiators

- Company maintains growth outlook despite tight funding environment

- Strong return ratios and compelling valuations makes it a worthy buy

Non-banking financial companies (NBFC) stocks have seen a sharp fall since September-end following liquidity concerns that engulfed the sector. While the correction has eliminated valuation froth creating some interesting investment opportunities, funding in the near term is expected to remain constrained, demanding a selective approach.

After running through a long list of NBFCs that have been penalised by markets, but stand out in terms of business fundamentals and valuation, we zeroed in on IndoStar Capital Finance.

Incremental loan growth driven by retail assets

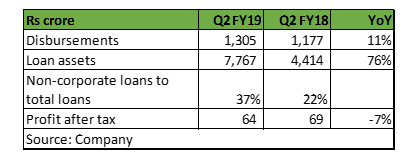

Primarily a wholesale financier, the company forayed into SME, vehicle and housing finance to de-risk its loan book. The result of its diversification strategy is clearly evident in the changing mix of its Rs 7,767 crore loan book. Non–corporate loans now constitute 37 percent of its loan book as at September end as against 22 percent a year ago. In fact, 68 percent of disbursements in Q2 FY19 was towards the three focused retail segments (SME, vehicle and housing finance).

Asset quality vulnerable but diversification to help

IndoStar’s asset quality has been resilient so far, with overall gross non-performing assets at 0.9 percent as of September-end.

The lender’s real estate exposure, at 33 percent of its asset book, is a contentious issue in the current environment. The management said it has been mainly lending to reputed developers in the residential market, staying away from the luxury segment where the slowdown is prominent and targeting projects with apartment ticket size between Rs 60 lakh to Rs 2-3 crore in the Mumbai region.

Project cash flows are escrowed and at times it resorts to selling a portion of its realty loans to avoid concentration risk and free up capital. In some cases, the loan is structured in a manner that enables mandatory prepayments, resulting in early repayment of loans. For instance, Q2 witnessed large pre-payment of real estate loans, which was refinanced from banks.

Overall, asset quality remains susceptible to cyclical downturns in the realty space. However, we draw comfort from its prudent risk management and increasing proportion of retail loans, which will bring further granularity to its medium term loan portfolio.

Healthy earnings profile

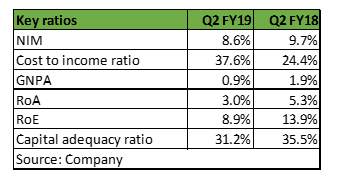

IndoStar enjoys a healthy earnings profile, with return on assets (RoA) around 3 percent.

With a focus on new segments, cost-to-income ratio has inched up in recent times as management created retail infrastructure for the same. While expansion in retail segment will diversify its income, it will also result in normalisation of RoA as retail tends to have lower spreads and higher operating expenses compared to wholesale financing.

Despite the diversification strategy putting slight pressure on return ratios, we view the move as desirable as it will de-risk its loan portfolio. We don’t expect any significant fall in return ratios as scaling up in these segments will be gradual and measured. For instance, the company doesn’t intend to open new branches till Q1 or Q2 next fiscal by which it expects all its branches opened in phase 1 to break-even.

Comfortable capital and liquidity position

Thanks to its fund raising in May, where it raised fresh capital of Rs 700 crore, IndoStar’ overall capital adequacy ratio (CAR) is very healthy at 31 percent as on September 30. Large quantum of equity gives it an edge over peer group in raising funds though currently it has depressed its return in equity (RoE) to below 10 percent.

We are most encouraged by the fact that company has maintained its disbursement target of Rs 550-600 crore, despite the tight liquidity conditions. Having disbursed Rs 3,500 crore in H1 FY19, the management sounded very confident of achieving Rs 6,000-7,000 crore as annual disbursement. Maintaining growth guidance is testimony of company’s comfortable liquidity position.

Experienced management

IndoStar has an experienced senior management team and is sponsored by reputed institutions (Everstone Capital, Goldman Sachs) and benefits from their high level of involvement. While the company is not backed by a big group, its professional and experienced management gives us lot of comfort.

Compelling valuationsIn October, its market capitalisation fell to less than its Q1 FY19 net worth. From that level, the stock has seen smart recovery of around 24 percent, but is still down more than 40 percent from its high. Its risk–reward is extremely favourable with the stock currently trading at 1.1 times FY20 estimated book. The limited history of the company and sectoral concerns have made investors jittery. However, the stock’s current valuation is compelling, pricing in most concerns, making it a worthy long term bet.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!