Moneycontrol Research

Highlights

- Fed seems poised for a rate cut in its July policy meet

- Commentary on global growth & domestic investment should provide crucial cues on policy direction

- Inflation trajectory remains the single-most crucial variable for central banks

- Trade talks remain “difficult to model” variable in terms of outcome

- Other central banks expected to follow Fed

Fed’s July meet (July 30-31) concludes on Wednesday, that is today, and the outcome is perhaps among the most eagerly awaited in the financial industry in recent times. In terms of policy rate direction, during the past eight months, debate in the FOMC (Federal Open Market Committee) has shifted to when and how much to cut rate, from when and how much to hike.

Also read: Fed gears up for accommodation amid inexplicable inflation & unchartered trade war

Going by CME FedWatch tool, Fed Fund futures suggest 78 percent probability for a 25 bps rate cut and 22 percent probability is inferred for even a larger 50 bps rate cut. Towards the end of 2019, implied probability is for two to three rate cuts of 25 bps.

Key variables to watch

Domestic macro: While Fed’s earlier commentary on labour market and consumption demand remains positive, commentary on business investment, which has been weak recently, would be an important aspect to pay attention to.

Global growth concerns: Global growth indicators remain subdued, partially weighed by ongoing trade spat, Brexit (no-deal scenario) and Iran sanctions. Recent progress in US-China trade talks remains a key watch. As far as the Fed is concerned, this remains a parameter which can’t be easily modelled as the outcome is purely in the executive domain and even if any trade talk outcome is round the corner, impact on the economy would come after a time lag. However, the Fed would like to avoid any flip flop in the interest rate policy direction and hence come with enough caveats before deliberating on future discourse.

Also read: China slowdown, or is it China changing and the world needs to take note of it?

Inflation readings: Key structural risk which the Fed and other central banks are struggling with is the persistence of lower inflation even if the economy is strong. For good part of interest rate hike cycle, the Fed had been well short of achieving the inflation target of 2 percent wherein near-term inflation projections have had a downward bias.

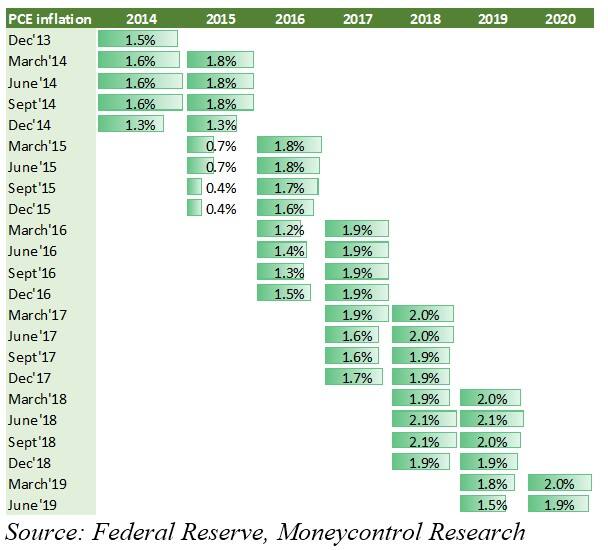

Table: FOMC inflation projections for near term

In light of this, it is interesting to note that in Fed’s previous policy meet, longer term projection for policy rate has come down to 2.5 percent (vs 2.8 percent earlier) which is closer to current Fed rate and suggests policy rates have clearly peaked in the current interest rate cycle.

Chart: Federal funds rate long-term rate projection

In the previous meet, FOMC members expressed concern about the pace of inflation’s return to 2 percent target. Near-term inflation projection for 2019 has been brought down to 1.5 percent in June meeting as against 1.8 percent in March.

However, note that recent June inflation reading has seen signs of improvement. The core personal consumption expenditures price index, which excludes volatile components food and energy, increased 1.6 percent YoY.

Set-up by other major central banks adds to global easing environment

The ECB meet on July 25 has set the context for stimulus measures to meet the threat of economic slowdown and the persistent fear that inflation readings might undershoot the inflation target of 2 percent. Its chief Mario Draghi has hinted that options would range from policy rate cuts to another quantitative easing package in the next September meet.

The BoJ (Bank of Japan) has also signalled that it would aggressively act on any further economic weakness due to global events. Interestingly, these events are not limited to global economic worries and the trade war, but also include monetary easing by other central banks.

For instance, lower interest rate decision by the Fed would lead to appreciation of the yen with respect to the dollar and that would further impact Japan’s export competitiveness. In short, a synchronous monetary easing stance may ratchet up across the global central banks.

Note that as a part of its monetary accommodative stance, the BoJ keeps a cap on 10-year bond yields at about zero and would continue to purchase bonds at the rate of more than $700 billion a year.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.