Neha Dave

Moneycontrol Research

Highlights:

-Q1 FY20 earnings weaker than expected

-Loan growth stumbles, margins compress

-Asset quality deteriorates with high slippages

-Valuation moderates but upside contingent on growth trajectory

------------------------------------------------

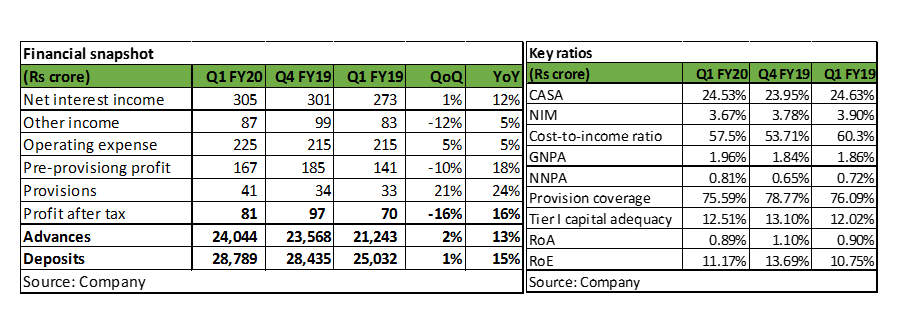

DCB Bank reported weak performance in the first quarter of FY20. Broader numbers showed a miss on many counts – margins, growth and asset quality. Q1 FY20 net profit growth decelerated to 16 percent YoY, mainly after lower advances growth and higher slippages.

With a balance sheet size of Rs 36,282 crore as of June-end, DCB is a small-sized private bank. Hence, the bank must grow higher than the industry to remain relevant and gain scale.

We concur with the management that the current environment has turned slightly challenging. But at the same time, a large part of the banking system (public sector banks) has been rendered weak and NBFCs are stepping back following the liquidity crunch. Investors would expect DCB bank to grab this opportunity and garner market share. In this context, Q1 numbers as well as the management’s cautious commentary are extremely disappointing.

The stock corrected sharply on weak Q1 results. As such, the valuation has turned reasonable. But considering the softer future growth, we don’t see much upside to the stock price in the near term.

That said, DCB has delivered gradual, but steady improvement in the return ratios over the last two years and has levers to improve it further which makes it worth keeping it on the radar.

Key positives

DCB posted lower advances growth compared to its historical run rate. But if we exclude corporate banking which is not a focus area for the bank, the loan growth was much better at 19 percent YoY.

Deposit profile of the bank improved as it garnered more retail term-deposits, which grew by 28 percent YoY while reducing the share of the inter-bank deposits, which now constitute 13 percent to the total deposits.

Despite deteriorating in this quarter, DCB’s asset quality is still better than peers. Additionally, the bank’s low restructured advances (0.16 percent) and policy to maintain floating provisions (Rs 84 crore in Q1) provide a lot of comfort.

Key negatives

DCB’s overall loan growth slumped to 13 percent YoY in Q1. The bank had earlier guided to double the loan book in 3 years, which translates into targeted loan book growth of 22-24 percent CAGR. The target is modest, considering the bank’s small loan book size, which is less than 1 percent of overall banking system advances. And now the softer growth in Q1 calls for closer look at the loan growth in coming quarters.

Net interest margin fell to 3.67 percent in Q1, down 11 bps sequentially. While yields on loans expanded, the increase in cost of funds was much more and compressed margins. Funding cost increased on the back of the bank’s efforts to garner more retail term-deposits and reduce the share of bulky inter-bank deposits. While this approach to improve the deposit profile is a long-term positive, it is likely to adversely impact NIM in the near term.

Non-interest income remained lacklustre. Bank’s core fee income declined by 9 percent YoY.

Operating cost growth was muted at 5 percent YoY. However, cost-to-income ratio increased to 57.5 percent in Q1, from 53.7 percent in the previous quarter, on modest growth in income.

Asset quality deteriorated with gross non-performing asset (GNPA) ratio increasing to 1.96 percent due to higher slippages in agriculture and commercial vehicle portfolio. Slippages rose to 2.5 percent (highest in the past 12 quarters), but higher write-offs contained the headline GNPA numbers.

The bank’s funding profile remains average, with a low share of CASA deposits at 25 percent, much lower than the industry average.

Other comments

In a bid to boost its deposits franchise, DCB has made an offer to Abu Dhabi Commercial Bank to acquire the business of its two branches amounting to Rs 1,155 crore of deposits (mostly retail/ NRI) and Rs 997 crore of advances (mostly short-term corporate).

Outlook

Going forward, improvement in return ratios for DCB bank hinges on balance sheet growth and operating leverage. The bank’s ability to maintain its margins and asset quality as it grows its book will be crucial. Slippage on any of these variables will make the bank’s journey more arduous.

DCB’s stock has corrected 18-20 percent from its 52-week high price and is trading at 1.7 times FY21 estimated book, which is reasonable. However, valuation re-rating is unlikely till the bank improves the growth momentum. With not much room for valuation re-rerating, the upside to stock price in the near term will be in tandem with earnings growth.

Nevertheless, long term investors should keep the bank on the radar and utilise the further weakness in stock price as an opportunity to accumulate the stock.Follow @nehadave01

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.