Neha Dave

Moneycontrol Research

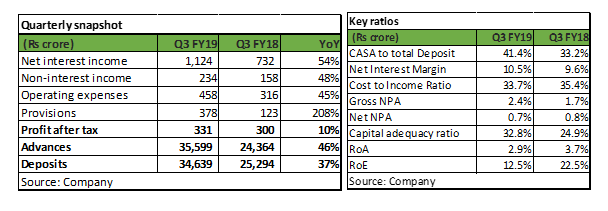

Bandhan Bank reported yet another quarter of strong growth. Net profit growth was subdued at 10 percent year-on-year (YoY) as the management fully provided Rs 385 crore as exposure to Infrastructure Leasing & Financial Services (IL&FS) during Q3 FY19.

Key positives

- Advances book grew at an accelerated pace (46 percent YoY) in Q3 increasing to Rs 35,599 crore.

- In a short span of three years after receiving a banking licence, Bandhan Bank has built a formidable deposit franchisee. Growth in current and savings account deposits (CASA) at 71 percent YoY outpaced the bank’s total deposits growth of 37 percent as at December 31, 2018. Consequently, the bank’s CASA ratio improved to 41.4 percent, increasing by almost eight percent compared to same period last year.

- Its high yielding loan portfolio (87 percent of advances is micro lending) and low cost of funds resulted in high net interest margin (NIM). The same was stable at 10.5 percent in the quarter under review and remains much higher than the industry average.

- Strong other income growth of 48 percent YoY was underpinned by growth in fees from selling priority sector lending certificates (PSLC). This is potent source of fee income for the bank, since 96 percent of its advances qualifies for priority sector lending (PSL).

- The bank enjoys pristine asset quality though gross non-performing assets (GNPA) inched up 2.4 percent from 1.3 percent as it recognised IL&FS exposure as a non-performing asset (NPA). Nevertheless, the bank fully provided for it, hence net NPA remained almost stable at 0.7 percent as at December-end.

- Low cost-to-income ratio at 33.7 percent in Q3 reflected the bank's superior operating efficiency.

Key negatives

- Despite attempts to scale-up its non-micro asset book, which grew 64 percent YoY, albeit on a lower base, Bandhan Bank is predominantly a micro finance lender as 87 percent of its book still comprises of micro banking loans, which renders it asset quality highly vulnerable. That said, merger with GRUH Finance will reduce concentration of micro loans to around 58 percent of its total loan book.

-Bandhan Bank enjoys high spread and return on asset (RoA) of 4.3 percent (trailing) compared to 2.6 percent for GRUH Finance. Post-merger, RoA of the merged entity is expected to compress, though return on equity (RoE) is expected to inch up.

-GRUH Finance is an expensive acquisition and will be book value dilutive to Bandhan Bank.

Other observations

- Merger with GRUH Finance does not fully resolve promoter stake dilution concern. The bank needs to further pare down its promoter holding to 40 percent from 61 percent.

- Smooth integration of GRUH Finance and scaling up of affordable housing book will remain a key monitorable.

OutlookWhile micro finance is a relatively riskier asset segment, with inherently weak borrower profile susceptible to socio-political issues and the resulting unhealthy credit culture, few in the industry boasts of a track record as Bandhan Bank. Superior return ratios, pristine asset quality, strong capitalisation, improving funding profile and highly experienced management and promoter profile clearly makes Bandhan Bank an outlier in this segment.

In a reaction to the merger news, the stock corrected and is now down more than 30 percent from its 52 week high.

Even after a sell-off, the stock trades at 5.5 times FY20 estimated book value. With substantial progress on promoter stake reduction and full provision to IL&FS, the key overhang on the stock is behind us. We see the premium valuation sustaining, given its strong return profile, with levers of improvement in place.

With not much room for a valuation re-rating, the upside in the stock will be in tandem with earnings growth. Long term investors should look to buy this high quality business operating at the bottom of the pyramid on further correction, if any.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!