Stories of seasoned investors and rookie traders making a fortune in the post-COVID bull run are now part of market lore. A lesser known story is the growing dominance of new-age trading companies that have been quietly scooping up small gains, and by doing just that consistently, minute after minute, growing their profit manifold over the past 4-5 years.

These are high-frequency trading firms – or algo firms in market lingo – that use complex algorithms and powerful computers to execute trades at lightning speeds. National Stock Exchange (NSE) data for December shows that trades by these firms accounted for 54 percent of the total trades on the exchange. On the BSE, the figure is 41 percent.

The numbers indicate a significant change in the balance of power on Dalal Street, where computer and mathematics whiz kids in their early 30s with limited understanding of the markets and companies are competing on an equal footing with more established banners. And, the numbers show the new kids on the block are scoring big.

The players

The names Graviton Research Capital, Alphagrep Securities, APT Portfolio, NK Research, Quadeye Securities, Dolat Algotech, Tower Research India, and iRage Broking may not ring a bell for most. They are the Big Daddies of the rarefied world of algorithmic trading, where transactions and investment decisions are driven by a potent combination of mathematics, statistics and cutting-edge technology.

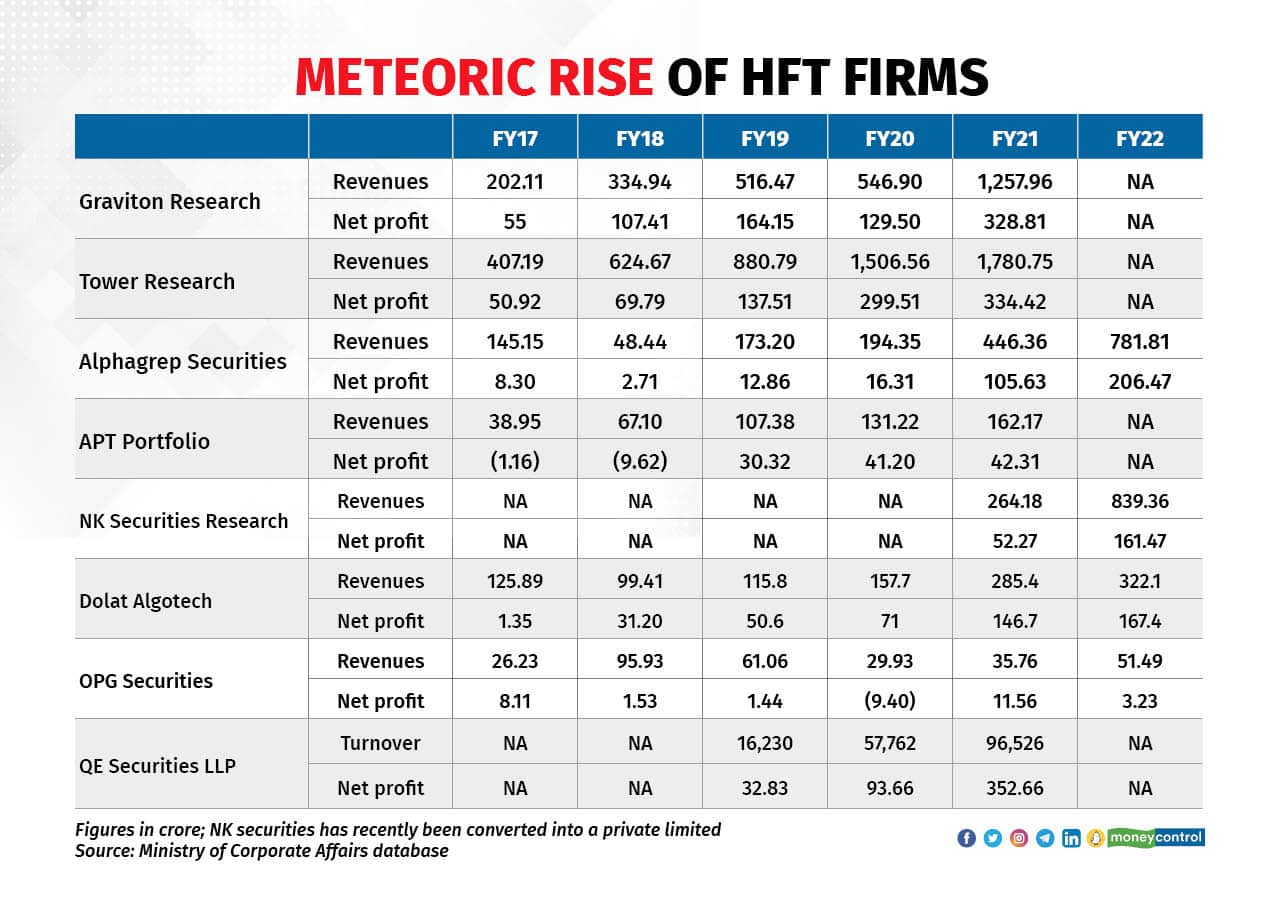

From the annual reports sourced by Moneycontrol, QE Securities (part of Quadeye group), Graviton Research and Tower Research India appear to dominate the field. QE Securities’ net profit soared from a mere Rs 33 crore to Rs 353 crore between FY19 and FY21. Turnover jumped sixfold from around Rs 16,000 crore to over Rs 96,000 crore. Numbers for FY22 were not available.

At Gurgaon headquartered Graviton, net profit grew over six-fold from Rs 55 crore to Rs 329 crore between FY17 and FY21. A similar spike was seen in revenues, which surged from Rs 202 crore to Rs 1257 crore during that period. Breaking down the net profit based on trading days during the year, Graviton’s algorithms cranked out Rs 20 lakh every minute during trading hours of the raging bull market in FY21. The outfit, founded by IIT Delhi graduates Nishil Gupta and Ankit Gupta in 2014, is present in the international markets as well. Numbers for FY22 were not available on the MCA website.

Growth at Tower Research India, the local arm of US-based Tower Research, has been even more spectacular, with consolidated net profit surging from Rs 51 crore in FY17 to Rs 334 crore by FY21. Consolidated revenues during this period rose more than fourfold from Rs 407 crore to Rs 1781 crore.

Alphagrep, among the few HFT firms to have disclosed its FY22 numbers, said net profit exploded to almost Rs 207 crore from less than Rs 3 crore in five years, as revenues rose from under Rs 50 crore to nearly Rs 800 crore. The company founded by Mohit Mutreja and Prashant Mittal in 2009, also has operations in London, Singapore, and Hong Kong.

NK Securities Research, founded by Faraz Khan and Sudhanshu Narang, reported an almost threefold jump in net profit to Rs 162 crore in FY22 from about Rs 50 crore in FY21. Revenue for FY22 leapt by as much to Rs 839 crore.

Among listed companies, Dolat Algotech’s net profit rocketed to Rs 167 crore in FY22 from Rs 1 crore in FY17, although revenue just about tripled.

Algoquant Fintech, which was recently listed on the BSE through a reverse merger with Hindustan Everest Tools, has seen its operating performance improve over the past couple of quarters. It reported a net profit of Rs 2.87 crore for the quarter ended September 2022.

Business model

So what exactly are HFT firms and how do they make so much money?

For starters, while HFT firms are commonly referred to as algo trading firms, there is a subtle difference. Algo trading, as the name suggests, involves the use of algorithms to make trading decisions and execute trades. HFT is algo trading at its core, but involves the use of powerful technology to execute trades at extremely high speeds, flipping positions in milliseconds. You can say it is algo on steroids.

For example, a basic algo for trading in the Nifty index would be to buy the Nifty if the 50-day moving average rises above the 200-day moving average and sell when the 50-DMA drops below the 200-DMA. A more complex algo will have multiple rules built into it.

The HFT version of this Nifty strategy would be to repeatedly buy and sell or sell and buy the Nifty index for very small difference, say 2 points, by predicting which way the index is likely to move. HFT algos try to predict price moves by identifying patterns in historical data, analysing order books and other market data to spot behavioural patterns of traders and other algos, and in some cases, even analysing news articles and social media posts.

Speed is crucial for the success of an HFT strategy, which is why they place their servers in the premises where the stock exchange’s servers are housed. This arrangement, known as co-location, allows HFT firms to access stock prices a split second ahead of the rest of the investing public.

However, execution speed is not a determining factor for the success of an algorithmic strategy, as it primarily depends on certain conditions being met, which do not change every second, like order book and liquidity.

Most algo firms use a mix of HFT and non-HFT strategies, experts said.

F&O booster

HFTs mainly operate in the futures and options (F&O) segment because the derivatives market is more liquid, allowing entry and exit at a faster rate with minimal impact on prices. Besides, the F&O market offers higher leverage than cash markets, meaning traders can take up a larger position with less capital.

The explosive growth in F&O volumes on the NSE after COVID turned out to be manna from heaven for HFTs, which were already becoming a major force in the stock market. The nominal average daily turnover value in the NSE’s F&O segment was Rs 14 lakh crore in FY20. That almost doubled the following year as a wave of newbie traders stampeded into the market, enthralled by the precipitous fall and equally dramatic rebound between March and April 2020.

Since then, F&O turnover has risen every year. For FY23 so far, the average daily turnover value is about Rs 130 lakh crore, almost 10 times higher than the pre-COVID level. In comparison, the average daily cash market turnover has just about doubled from pre-COVID levels. Even at its peak in October 2021, the cash market turnover was a shade below three times the pre-COVID levels.

There were many factors driving the F&O frenzy. Since the market was rising pretty much one way for almost 18 months, an overwhelming majority of amateur traders made easy money, first by trading in stocks, then in options contracts.

Smarter option

“These people quickly figured out that they could multiply their money faster through options trades since they had to put up less capital upfront by way of margins compared to what they had to fork out for cash market trades,” said an expert. “They would buy call options on the cheap and make good money on those. And those who sold put options thought they had hit a risk-free stream of income since the market was not falling much.”

Sensing an opportunity stemming from this ballooning of interest in F&Os, self-proclaimed ‘F&O experts’ arrived on the scene, claiming to have made super profits themselves and offering to share the secret sauce for a price. These gurus, or furus (fake gurus) as they mostly turned out to be, became role models for thousands of youngsters who eagerly signed up for exorbitantly priced training workshops, hoping to make millions by trading options.

And then there were software developers who went around hawking algo strategies to wealthy traders with the promise of market-beating returns.

“Majority of these so-called algo strategies were nothing but a set of standard rules for executing trades; they would work sometimes, but results were largely patchy,” the expert said. “And these low-level algos ended up becoming lunch for the far sophisticated algos that the HFTs had unleashed into the system.”

Since the HFT algos were primed to identify patterns, they could easily outsmart any other algo that left a trail. There are jokes in HFT circles about certain employees owing their annual bonuses to some of the basic algos deployed by HNIs, the expert said.

The crew

Check out the careers section of any HFT and you will hardly find openings for analysts specialising in a particular sector. The demand is mainly for IIT-trained hardware engineers, software developers and quantitative analysts.

Quants, as quantitative analysts are called, are specialists who apply mathematical and statistical methods to develop financial and risk management models.

“Quants and coders (software developers) are the two main pillars of any algo trading firm. The ratio of quants to coders will depend on the strategy of the firm,” said a person familiar with the workings of such firms. “Once the quant has developed a model by researching data and identifying patterns, the coder needs to create the software for running it. If the firm specialises in HFT, then there will be more coders than quants. If the firm is more into non-HFT algos, it will have more quants in the team than coders.”

The models and technology need to be refined constantly to stay ahead of competition, the person said.

“Think of it as changing the tyres of a Formula One car in a race,” the person said. “You are competing with rival algos as smart or even smarter than yours. If you can detect their vulnerabilities, they can spot yours.”

Unlike research analysts at traditional broking firms and fund managers at mutual funds or portfolio management services who make headlines for calling multibagger stocks, the stars at HFTs are largely unheard of, given the highly technical nature of their work and the secretive nature of algo trading.

The websites of most HFTs rarely give details of their key employees, other than a passing reference to the founders, if at all. But annual bonuses are said to be handsome, easily topping a couple of crores for the best performers.

Below the radar

And for all their success, the founders of algo trading firms have chosen to stay away from the limelight. You won’t find glowing profiles about them in the press, or any mention of their fancy acquisitions on page 3.

A controversy over the NSE’s co-location server facility could be one reason these investors like to keep it quiet, people in this field said. The highly publicised case involved some trading members exploiting loopholes in the NSE’s co-location rules and profiting by getting access to stock prices ahead of other members.

Former NSE MD and CEOs Ravi Narain and Chitra Ramkrishna are in jail on charges related to the case. Also behind bars is Sanjay Gupta, the promoter of OPG Securities, alleged to be one of the major beneficiaries of the violations.

“When you say algo trading, the first thing that comes to mind is the NSE co-location controversy,” said a source. “The general perception is that algo firms have an unfair advantage over the rest of the market. But then most people don’t understand what algo firms actually do.”

“Founders don’t need the publicity because the majority of them, if not all, are neither looking to add clients or attract capital,” said another person. “Secondly, unlike value investors or technical analysts, you can’t talk about your trading strategies. Also, you cannot deploy a whole lot of capital in algo trading even if you had it – it is not like buying huge blocks of stocks and then waiting for the price to appreciate.”

HFTs globally have been at the centre of fierce debates, with critics drawing attention to the systemic risks they pose. There have been instances of flash crashes globally as well as in India because of algos going haywire.

Besides, algo trading firms are accused of increasing volatility and gaining at the expense of ordinary investors and even long-term institutional investors such as mutual funds, insurance and pension funds, which are not into high-frequency trading.

On their part, algo trading firms argue that they improve market efficiency by providing liquidity which would otherwise not be there. One common HFT strategy is to provide two-way quotes (placing simultaneous buy and sell orders, and pocketing the difference), thereby acting as a market maker.

“They are a necessary evil,” said a high-volume trader. “Back in the days of open outcry, it was the jobber who would provide liquidity by temporarily taking on the risk. Today, algo trading firms play that role.”

Note: The story has been updated with numbers for QE Securities, part of the Quadeye group. Also, Tower Research’s annual revenues for FY21 is Rs 1780.7 crore and not Rs 1504 as mentioned in the earlier version of this story. The error is regretted

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.